Qorvo (NASDAQ:QRVO) is a semiconductor company with a focus on enhancing connectivity and power efficiency in various industries such as consumer electronics, IoT, automotive, network infrastructure, and aerospace/defense. Semiconductors being in a cyclical industry have to capitalize on the boom years to survive the lean years. What concerns me most about Qorvo is that its performance was not only quite fragile in a moderate year, but its future also looks quite uncertain. Below are the reasons I have less confidence in the stock for the near future:

1. Disproportionate exposure to a few customers and major exposure to the smartphone industry

2. Uncertain macro and weak demand that may again disproportionately affect Qorvo

3. Valuation that does not reflect the risks

Weak Key Metrics

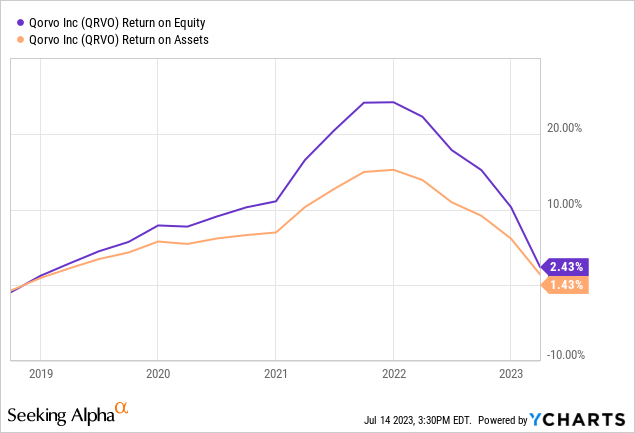

While it saw significant growth in 2020 and 2021, it’s top line and profitability started suffering in the latter half of 2022 and 2023. Its Earning per Share pretty much fell back to the level that was last seen in 2019 ( ≈ $1) Both its Return on Equity (ROE) and Return on Assets (ROA) have dropped down to low single-digit percentages which further indicates that its profitability and efficiency have suffered.

What is the reason for this?

Its two largest customers Apple and Samsung account for almost 50% of its business and this level of dependency indicates that any changes in Apple’s demand or business relationship could significantly impact the company’s financial performance. Exposure to smartphone phone sales is a key risk acknowledged by the company. In fact, Q4-2022 saw the biggest-ever drop in smartphone sales with 18% for the quarter and 11% for the entire year. High exposure to the smartphone industry is indeed a key risk for the company.

What does the future hold?

Concentration risk

As evidenced, Apple is known for dropping its suppliers and developing its own in-house capabilities when they decide the relationship does not work for them. They dropped Intel in favor of its own chips, dropping Broadcom and Qualcomm in favor of its own modem, Bluetooth and Wi-Fi is expected to occur as soon as 2025. While Qualcomm, Intel, and Broadcom are far bigger companies and could handle losing Apple as its key customer, such moves will have a material adverse effect on Qorvo’s business, financial condition, and results of operations.

Inventory and Valuation risk

This would tie to demand and the overall health of the economy. While a demand slowdown itself significantly brought down the company’s profitability, I would hate to think what a recession would do to this stock. This is where it gets tricky. There is no foolproof way to predict when an economic downturn would arrive which means that the company would end up overestimating the demand and end up having an inventory problem on its hands.

To ensure availability the company proactively purchases materials and manufactures products before receiving binding purchase orders. Qorvo has entered into agreements with its suppliers that ensure that its request for capacity is met through 2026. This was put in place in 2022 after the industry faced wide supply constraints. This is a double-edged sword. If the purchase commitments per the agreement are not met, it is quite likely that the company loses money to honor its commitments to the supplier.

This is precisely what happened to the company in fiscal 2023. Weakened demand for 5G handsets in China meant that they had to record impairment to the deposit and recognized additional inventory reserves.

Scenario-based valuation

The earnings multiple is quite bloated due to the company facing significant headwinds in recent quarters. To a degree, this has been reflected in its stock price, as we saw the stock fall almost 60% from its highs. Can the valuation come down even further? Early indicators suggest this might happen. Largan Apple’s largest camera lens supplier is not optimistic about 2023 citing a weak 2023 market. Many semiconductor companies expecting a sluggish second half of 2023, are already eyeing past this and looking into a recovery in the second quarter of 2024.

But there is a growing chorus that the recession may be pushed from 2023 to 2024. As the economy displayed greater durability than anticipated and the United States managed to steer clear of a recession thus far, the likelihood of a recession in 2023 has been diminishing. Consequently, bets and predictions have begun to extend into the future.

This is clearly at odds with what is expected for the smartphone market. If we saw an 11% decline in the smartphone market for Q2-2023 (with no recession) what could we expect for 2024? In such a situation, it’s better to account for valuation under a range of scenarios.

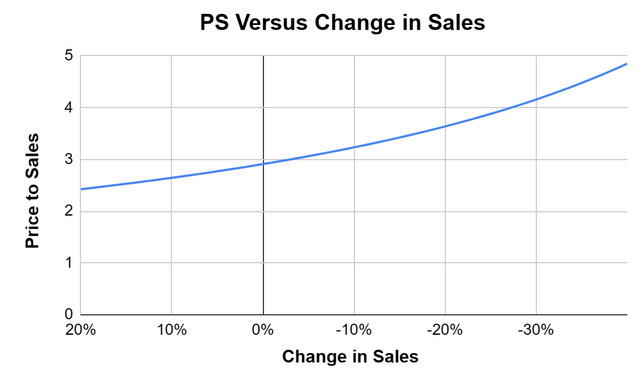

Author Calculated

The current Price to Sales ratio is 3x but a 30% hit to sales would result in a forward PS ratio greater than 4x. For context between the 2022 and 2023 fiscal years, we saw sales decline by around 23%. In a general sense, the semiconductor industry itself is overvalued, riding too much on the promise of AI, and may very well see a correction if the optimistic scenarios (no recession, strong demand) don’t materialize.

What would invalidate this thesis?

If the demand for smartphones starts to roar and Qorvo’s key customers continue to be committed to the company it is highly likely that the stock price will grind higher. There is also a possibility that the company successfully diversifies its business away from smartphones which means that it is less exposed to the cycles of just one industry. Its revenues and earnings could get resilient and shareholders would have much more to expect from this stock.

But for now, I would rate this stock as a Sell. The economic outlook combined with Qorvo’s commitment risks to its supplier and a valuation that may see a potential reset means that the continued risks of holding on to this stock far outweigh the benefits.

Read the full article here