Introduction

Canadian commercial printing and marketing solutions company DATA Communications Management (DCM:CA) (OTCQX:DCMDF) is among the largest positions in my investment portfolio and I’ve been looking at increasing my exposure to this sector. This is how I stumbled upon US-based Quad/Graphics (QUAD) and the company looked compelling at first sight – forward P/E of just 9.3x, over $200 million of forecast EBITDA for 2023, and a year-end debt leverage ratio of about 2x (see slide 15 here). However, upon digging deeper, the picture became gloomy as operating margins are underwhelming and interest expenses soared by over 50% year on year in Q2 2023. In addition, the TTM net loss stands at $25.7 million. Overall, I think Quad is facing significant headwinds and my rating on the stock is neutral. Let’s review.

Overview of the business and financials

Quad was established in 1971 and is a commercial printing company that offers marketing strategy and management services. It describes itself as a “global marketing experience company”. Quad currently employs about 15,000 people across 14 countries and has over 2,900 clients across the retail, publishing, consumer packaged goods, financial services, healthcare, insurance, and direct-to-consumer sectors.

Quad

The business is split into two reportable segments, namely United States Print and Related Services, and International. The former includes the US printing operations of Quad as well as its global paper procurement, and marketing and other complementary services. The segment also includes the production of ink and accounts for over 80% of the company’s revenues. The International segment, in turn, includes Quad’s printing business in Europe and Latin America, and investments in printing operations in India.

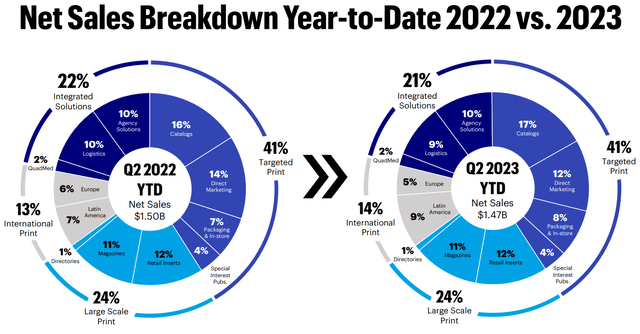

Looking at the breakdown of sales, I think that it’s a well-diversified company, as no business line accounts for over 20% of revenues. However, it’s worth noting that the print business is much larger than the integrated solutions business and I consider this to be negative as the latter usually have much higher margins.

Quad

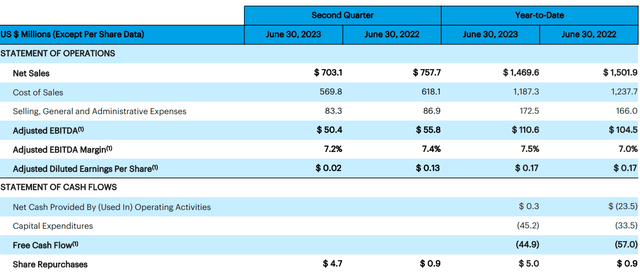

Turning our attention to the latest available financial results, we can see that the adjusted EBITDA margin was just 7.2% in Q2 2023, which is over a third lower than the level achieved by DATA Communications Management during the same period. In addition, Quad’s net sales decreased by 7.2% year-on-year mainly due to lower paper sales and logistics revenues. The company is thus losing economies of scale and selling, general and administrative expenses as a percentage of sales increased to 11.8% from 11.5% a year earlier.

Quad

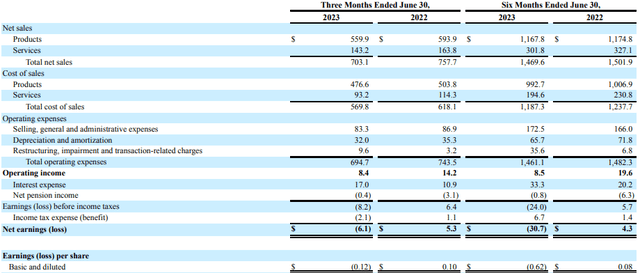

The net sales growth issues were concentrated in the United States Print and Related Services segment where product sales shrank by 8.4% due to lower print volumes while services revenues slumped by 12.3% as a result of a $16.8 million decline in logistics sales and a $2.8 million fall in marketing services and medical services.

Quad

In my view, the International sector is actually performing quite well as product sales improved by 7.1% on the back of a $17 million increase in print product volume and pricing. Services revenue slumped by 20% due to lower logistics sales but this was equal to just $1 million in absolute terms.

Quad

Looking at the income statement, I’m concerned by the rapidly rising interest expenses as they put Quad in the red in Q2 2023 after rising to $17 million from just $10.9 million a year earlier. It seems that rising interest rates are becoming a serious issue for the company as its blended interest rate stood at 6.7% in June 2023 (see slide 14 here) compared to just 3.8% in June 2022 (see slide 14 here).

Quad

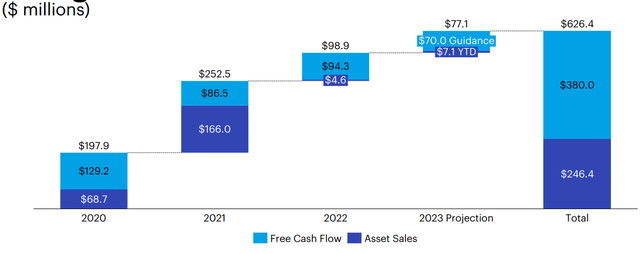

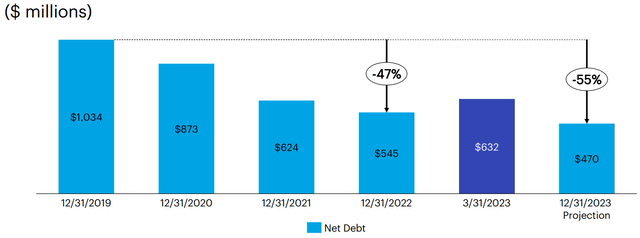

To be fair, Quad has been making serious progress on reducing its debt. According to the company’s presentation for the Q1 2023 financial results (see slides 13 and 15 here), its aim is to generate about $620 million through free cash flow and asset sales between 2020 and 2023 and thus reduce its net debt to $470 million by the end of this year.

Quad Quad

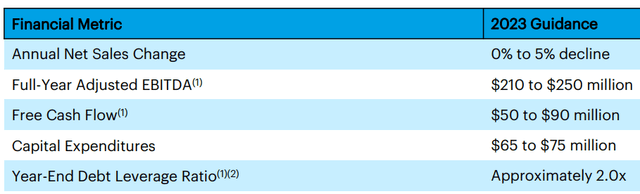

Yet, this goal seems difficult to achieve now considering the net debt decreased little in Q2 2023 and stood at $604.1 million at the end of June. Even if the net debt declines to $470 million, I think that Quad is in trouble as its interest expenses in Q2 2023 were more than two times higher than its operating income. On a positive note, the company has reaffirmed its guidance for the full year for the second quarter in a row and it expects to finish the year with adjusted EBITDA of between $210 million and $250 million and free cash flow of $50 million to $90 million. Considering the TTM adjusted EBITDA stands at $258.3 million, this guidance seems achievable.

Quad

Looking at the valuation, Quad has an enterprise value of $863.2 million as of the time of writing and the company is trading at an EV/adjusted EBITDA ratio of 3.75x based on the midpoint of the 2023 guidance. While this might seem low, I think that it’s a reasonable level for a company struggling with growth and keeping net income in positive territory due to low margins and rising interest rates. In my view, Quad should be trading at about 4x EV/EBITDA and thus the margin of safety here is low.

Investor takeaway

Quad has been selling assets and reducing its debt over the past few years in a bid to achieve sustainable profitability. Yet, the company has been struggling with organic growth and the remaining business has an EBITDA margin of just over 7%, which makes further debt decreases challenging. In addition, Quad’s net income is in the red due to spiking interest expenses and I don’t expect it to get back in the black anytime soon. Overall, I think that Quad’s balance sheet is in a much better position today compared to 2019 but the company doesn’t look cheap at 3.75x EV/EBITDA. In my view, risk-averse investors should avoid this stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here