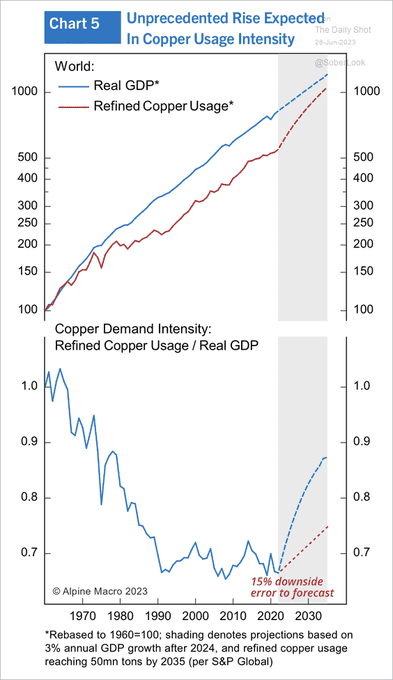

Dr. Copper prescribes rising demand in the coming years. According to S&P Global, as global real GDP grows through 2040, copper usage is seen as comparably climbing. Amid this unprecedented demand side jump, miners appear well positioned for long-term upside. Just recently, copper prices hit their best level since May as LME inventories dipped.

In the coming years, though, earnings on Rio Tinto (NYSE:RIO) are expected to be highly volatile, leading to a dividend yield that may fluctuate greatly. I have a hold rating on RIO due to shares being near fair value in my view while I assert its chart leaves something to be desired from the bullish perspective. I believe we need to see definitive signs that rising copper demand is playing out.

Bullish Long-Term Potential With Copper Plays

Sober Look

According to Bank of America Global Research, RIO is the world’s second-largest mining company, with operations in Australia, Africa, the Americas, Europe, and Central/SE Asia. Rio Tinto is the world’s largest producer of aluminum, the second largest producer of iron ore, and a top 5 producer of alumina, uranium, mined copper, export thermal & coking coal, and diamonds.

The London-based Diversified $107 billion market cap Metals and Mining industry company within the Materials sector trades at a low 8.3 trailing 12-month GAAP price-to-earnings ratio and pays a high 7.8% dividend yield, according to The Wall Street Journal.

RIO’s operations are somewhat diversified given its niche and features a strong return on common equity and dividend distributions to stockholders. Still, there is no getting around that the cash flow king is highly dependent on unstable areas like Brazil and China for supply needs and end-demand growth, respectively. Back in April, the firm reported record first-quarter iron ore shipments within a mixed report.

The management team left guidance unchanged but did reduce its copper production forecast due to operational issues at Escondida. Lately, growth risks out of China have hampered the stock price, so that is a key risk to consider in the coming quarters. On the positive side, however, it was reported that West Australia iron ore shipments registered the highest figure since mid-2020. Another risk for the bulls to consider is a worsening Real Estate sector outlook – that could pressure demand for copper and other industrial metals.

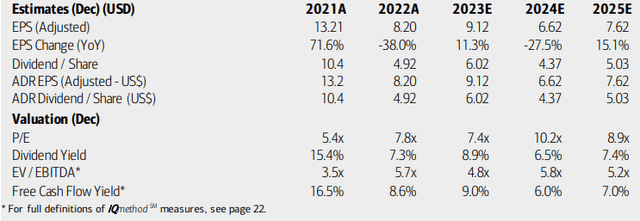

On valuation, analysts at BofA see earnings rising modestly this year after dropping sharply in 2022. Per-share profits for RIO are among the most volatile you will see. EPS to the ADR shares are then expected to drop hard in the out year before recovering back above $7 by 2025.

Amid the highly volatile profitability situation, the company’s dividend is flexible with EPS, so it will likewise swing around greatly. Still, the stock is seen as trading with a high-single-digit P/E over the coming quarters while its EV/EBITDA ratio is currently just a fraction of the S&P 500’s average multiple. Moreover, Rio Tinto boasts a high free cash flow yield.

RIO: Earnings, Dividend, Valuation Forecasts

BofA Global Research

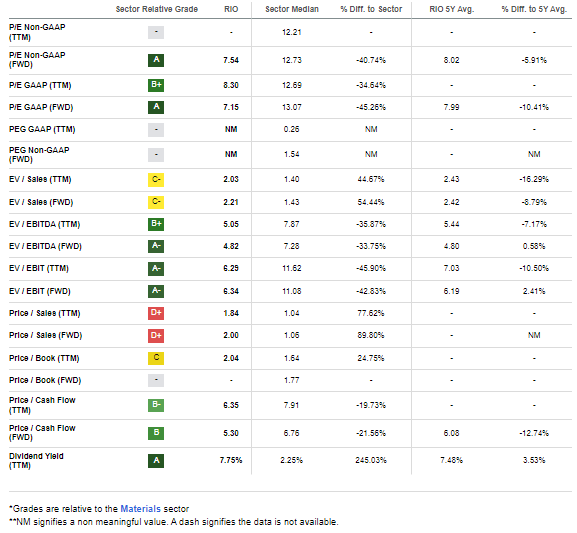

Shares trade at 7.15 times forward operating earnings estimates, which is a 10% discount to its long-term earnings ratio. It trades at a comparable discount on a price-to-cash flow basis. If we assume normalized EPS of $7 and apply a 10 P/E, then the stock should be near $70. While it is indeed a cheap stock compared to the broad market and its sector, I see it as merely a hold on valuation.

Rio Tinto: Cheap On A P/E Basis, But Volatile Earnings Story

Seeking Alpha

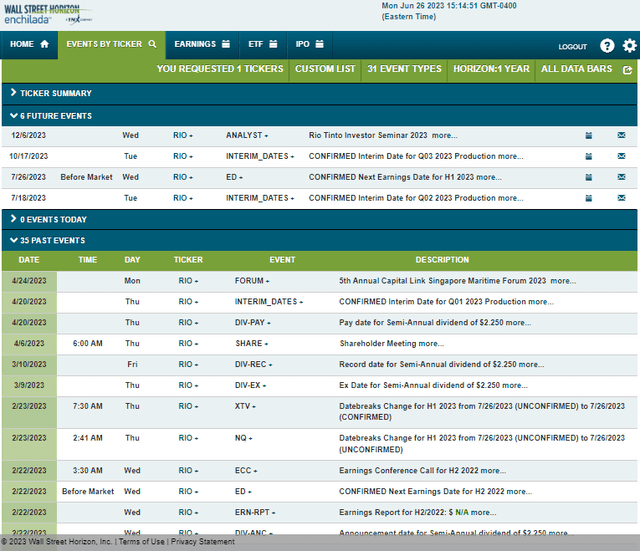

Looking ahead, corporate event data provided by Wall Street Horizon shows a confirmed first-half 2023 earnings date of Wednesday, July 26 BMO. Before that, the miner reports Q2 2023 production figures on Tuesday, July 18, which could also stir up volatility.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

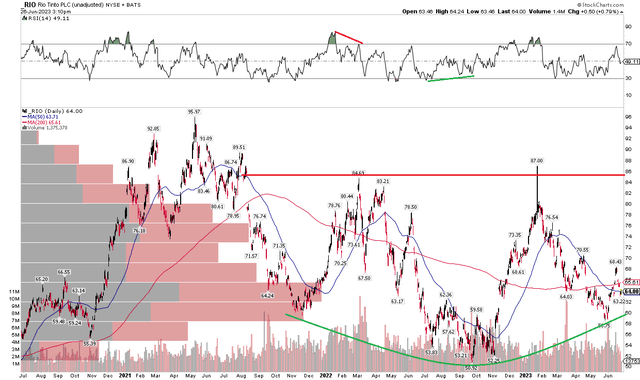

Just as RIO’s earnings picture is up and down, the chart is likewise messy. Notice in the graph below that shares are fractionally positive in the last 3 years, and it has been a full-blown ‘chopfest’ for the past 24 months. I see modest support in the $58 to $60 range while resistance is apparent between $85 and $87. There are, though, inklings of a bearish to bullish reversal pattern taking shape based on the late 2021 low, September 2022 bottom, and the successful retest of support about a month ago just below $59.

With a flat to slightly rising 200-day moving average, the bulls may be putting together a comeback here. I would like to see the stock rally above $71 initially, then challenge the aforementioned resistance zone. With ample volume by price in the $60 to $66 range, shares may simply churn here for a bit longer, but long with a stop under the September low can still work. In the meantime, investors can capture RIO’s lofty yield.

RIO: Some Bullish Signals, But Generally Trendless Price Action

Stockcharts.com

The Bottom Line

I have a hold on Rio Tinto. Earnings volatility is high while the technical trend is neutral. With shares not far from fair value, but with a high yield, there are mixed risks for long-term investors today.

Read the full article here