The 10-year treasury yield is now trading above 4%, and has thus topped the ∼3.6% dividend benchmark that investors expect from investing in Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD). The key question now is: Why should investors take the equity/ volatility risk on stocks when the U.S. government is offering a higher-yielding, “risk-free” alternative? Or formulated differently, should investors dump dividend stocks and pile into treasuries instead?

The short answer is yes. And the reasoning is in the question: If a risk-free bond security is yielding a higher income than an income-focused equity portfolio (higher yield and lower risk), than arguably only fools would not rotate their asset allocation.

Admittedly, stocks could in theory deserve a growth premium over treasuries, even dividend stocks. However, with interest rates trending around ∼5%, it is highly doubtful that cyclical businesses – such as those at the core of SCHD’s investment strategy – deserve an implied growth premium.

Reflecting on the current market environment, I advise to sell dividend portfolios/ ETFs (such as SCHD), and buy treasuries instead (SCHO).

SCHD’s Asset Allocation Strategy …

The Schwab U.S. Dividend Equity ETF is, as the name suggests, a fund designed to give investors exposure to dividend-paying U.S. equities.

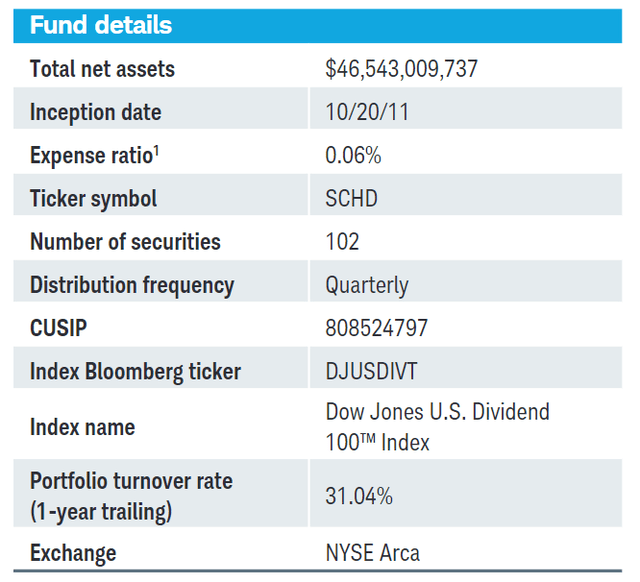

SCHD Fact Sheet

Specifically, the fund tracks “as closely as possible, before fees and expenses” the performance of the Dow Jones Dividend 100 Index (DJUSDIV); and, for the trailing twelve months, SCHD has distributed to investors ∼3.6% of NAV in form of dividends.

According to the fund’s fact sheet, the ETF currently holds 102 securities, with a one year trailing twelve months portfolio turnover ratio of ∼31%.

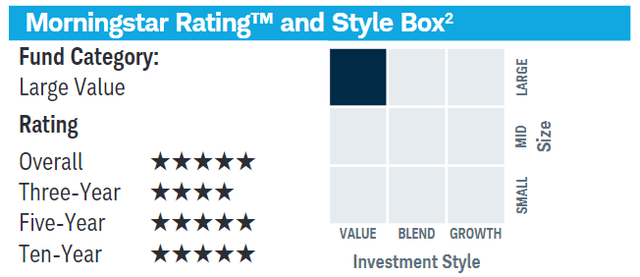

With a focus on dividends, SCHD invests primarily in mature businesses who have limited use for growth capital, and thus, distribute the major share of their earnings to investors. In that context, SCHD’s equity portfolio is strongly skewed towards large-cap stocks (consolidated industries) and value opportunities (statistically low accounting multiples, such as low P/E and P/B).

SCHD Fact Sheet

… Underperforms Treasuries On Yield

SCHD may be an attractive ETF for income-seeking investors. However, the problem that I am having with SCHD in the current market environment is that the yield on SCHD undeperforms the yield on U.S. treasuries on both the short- and long-dated part of the yield curve. For reference, the 2-year note is currently yielding ∼4.96%, and the 10-year note ∼4.95% respectively, versus a ∼3.6% income yield for SCHD. This is quite surprising, because treasuries, as a “risk-free” fixed income security, should trade at a discount to stocks, not at a premium — in order to compensate investors for taking equity/ volatility risk on their capital.

Another argument why treasuries may currently be better than dividend stocks is anchored on price risk: Investors should consider that the price skew is strongly favorable for treasuries (the value of treasuries will appreciate if the FED cuts rates, which is becoming a likely scenario), while quite unfavorable for cyclical stocks (going into a [likely] recession, there is an argument for lower earnings and lower equity prices).

Don’t Count On Growth

It can be argued that stocks, including slow-growing dividend stocks, may theoretically deserve a valuation premium compared to treasuries, because value accumulation for stocks is also a function of growth. Treasuries, on the other hand, are as “growth-free” as they are “risk-free”.

However, I would like to point out that SCHD’s fund holdings are quite cyclical, with little exposure to structural growth trends such as AI and automation. In that context, SCHD’s growth is – at least to a considerable degree – contingent upon supportive interest rates. But after a more than 500 basis points increase in the fed funds rate, I doubt that cyclical growth is still robust.

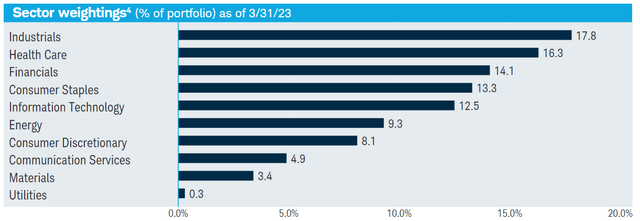

In fact, SCHD’s largest sector weight is Industrials with 17.8%, followed by another highly cyclical sector at the 3rd place, Financials, with 14.1%. Information Technology is only 12.5%, as compared to almost 30% for the S&P 500 (SPY)!

SCHD Fact Sheet

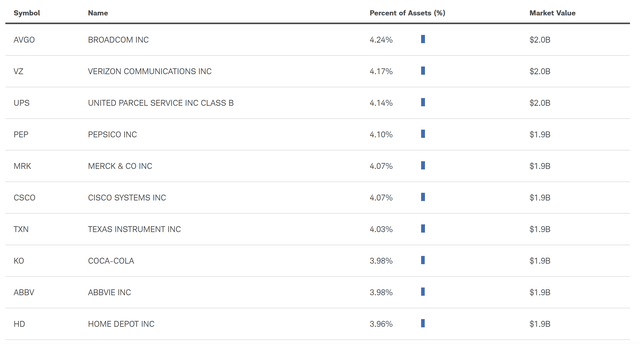

A more detailed look on SCHD’s top 10 single stocks confirms the allocation towards slow-growing, cyclically exposed, businesses.

SCHD Fact Sheet

In my opinion, it is extremely questionable whether cyclical businesses, which are the focus of SCHD’s investment strategy, merit an implicit growth premium as the FED aims to cool the economy. In times of an expanding economy, yes. But in the context of potentially facing a recession, which is negative growth, assigning SCHD a growth premium is quite a speculation. On the other hand, the Treasuries’ attribute of being “growth-free” may not necessarily be a downside, considering the macro circumstances.

Conclusion

The 10-year treasury yield is now trading above 4%, having topped the approximately 3.6% dividend benchmark that investors expect from investing in Schwab U.S. Dividend Equity ETF. Accordingly, I suggest that investors should consider moving their assets from dividend stocks to treasuries, given both higher yield and lower risk offered by the latter.

While stocks may deserve a growth premium when the economy is expanding, I argue that the premium should evaporate, if not turn negative, when approaching a recession. The argument is especially applicable for cyclical businesses, which make up the core portion of SCHD’s investment strategy.

With the FED trying to cool the economy, a Treasury investors’ gain is a SCHD investors’ loss. And accordingly, I advise to dump dividend portfolios/ ETFs, and pile into treasuries instead.

Read the full article here