Investment Thesis

My price target was triggered a couple of days ago, which is prompting me to look at T. Rowe Price (NASDAQ:TROW) again to see how the company has developed since February of this year and if it is a good time to start a position or if will we see further declines.

Assets Under Management

The last time I covered the company, it was coming off one of the worst years it had in recent times. FY22 was very bad for many companies in different sectors and asset management was one that got hit pretty badly. Assets under management or AUM fell $413B from the end of FY21 and stood at around $1.27B at the end of FY22. That was a massive hit for the company. As I mentioned in my previous article, the drop coincided with the overall negative broad market sentiment that brought down all the major indices.

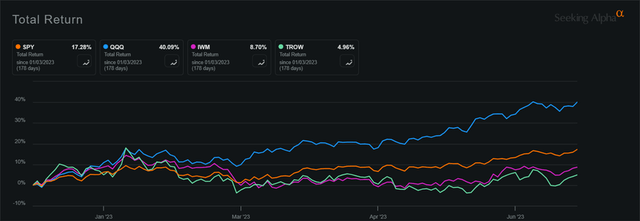

So, what has changed in the last 8 months? AUM has been increasing from those lows seen at the end of FY22 and now three months ended June ’23 stood at an average of $1.36B, which is around a 7% increase. In my opinion, this is a little underwhelming considering that the major indices have been performing spectacularly since the turn of the year, with SPY and QQQ rising 17% and 40%, respectively in the 6 months ending June 30th.

Total Return comparison (Seeking Alpha)

Outlook

Unfortunately, I wish I could be a little more upbeat about the economy, however, I believe that the macroeconomic headwinds are going to persist much longer than I anticipated. Inflation seems to be persistent and very sticky, which may force the FED to increase interest rates further. With the payroll numbers coming out hotter-than-expected for September, this is not a positive sign that the FED will stay put with its interest raises. The unemployment rate also ticked up a little bit in the report, but I don’t think it is going to be meaningful enough for J. Powell and we will see another interest rate hike in the remainder of the two sessions of the year. I expect a lot more volatility in the remainder of the year and at least the first quarter of ’24.

People are getting frightened yet again as they did in FY22, and preliminary results show a net outflow of $7.8B as of August 31st. I believe there will be further net outflows for the remainder of the year, and the company’s CEO is not very positive on that also:

“If I look at all of the leading indicators that I’m seeing right now, it suggests to me that we’re experiencing the worst of the pressure on flows, which is another way of saying I wouldn’t expect the run rate in the back half of the year to be greater than what we saw in the first half of the year. And as we work our way through ’24, we think we’ll see, as I say, noticeably less in the way of net outflows. But again, some things have to happen in terms of the industry backdrop, in terms of our investment performance, which we’re deeply focused on, and I’m encouraged by, and again, about execution against all of our strategic initiatives.“

In the short term, which is the next 3-6 months, I would expect a lot of volatility in net outflows and inflows, which may bring further share price deterioration, however, as we exit the macroeconomic headwinds sometime in 2nd half of ’24, I would expect net inflows to return, and the company’s position would improve.

Briefly on Financials

As of Q2 ’23, the company had $2.25B in cash and equivalents and still zero debt on books. The company continues to have plenty of liquidity for whatever it desires to do with it, whether to pursue more acquisitions in the future or reward shareholders via share buybacks or dividend increases. The company is in a great position because it doesn’t have to worry about annual interest expenses on debt, which frees up a lot of capital for these sorts of initiatives that I mentioned.

TROW’s current ratio continues to be very strong, which is a good thing and a bad thing in my opinion. According to Seeking Alpha, the current ratio stood at around 1.7 as of June 30 ’23, which is right at that range that I consider to be efficient. 1.5-2.0 current ratio in my opinion strikes a good balance between the ability to pay off short-term obligations and still have plenty of liquidity for whatever may come in the future. It also means the company has enough liquidity to further the company’s growth.

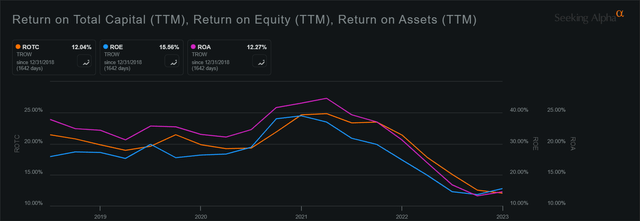

In terms of efficiency and profitability, TROW’s ROE and ROA have been fantastic over the years, and only FY22 made them slightly worse than its historical average. This tells us that the management is utilizing the company’s assets and shareholder capital efficiently.

The company’s Return on total capital has also been well above the minimum of 10% that I look for in an investment, which tells us the management is good at finding projects that have great returns. This also tells us that the company may have a decent moat and competitive advantage. We can also see the bottom set in at the end of FY22, so that is a positive if we continue to see the uptrend in the future.

Efficiency and profitability (Seeking Alpha)

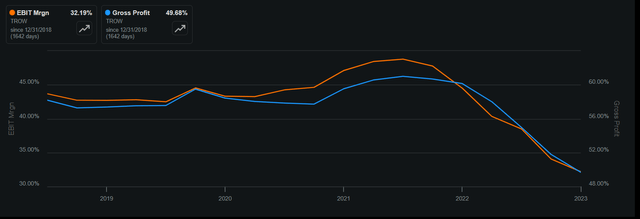

Margins (Seeking Alpha)

Overall, I see a strong company that will continue to weather the uncertainty rather easily given its liquid position. Slight worry about margins, however, as I mentioned this is a short-term problem and I wouldn’t worry too much.

Valuation

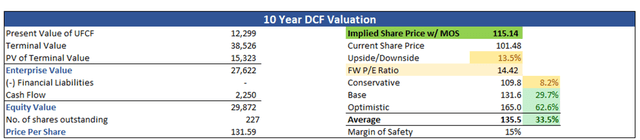

My parameters have changed since February slightly, so I’ll give a brief rundown of it here. I’m keeping my revenue assumptions on the conservative end for that extra margin of safety. For the base case, revenue will see a growth of around 3.5% CAGR over the next decade, which is about half of what the company managed to achieve in the last decade. For the optimistic case, I went with 5.5% CAGR, while for the conservative case, I went with 1.5% CAGR through FY32.

In terms of EPS, I modeled $7 a share for FY23 and $7.3 for FY24, and after that, the company will see around 7% CAGR in EPS until FY32 for the base case, 9% CAGR for the optimistic case, and 4% for the conservative case.

On top of these estimates, I will add a 15% margin of safety for extra cushion. The company’s balance sheet is very liquid and strong, so I believe 15% is sufficient. With that said, TROW’s intrinsic value is $115 a share, which means the company is trading at around a 13% discount to its fair price. This also shows how my assumptions updated over time, and now that the company reached my previous PT of $100, I believe the company is a buy at these levels.

Intrinsic Valuation (Author)

Risks

After such a rally that the indices saw during ’23, I would be very cautious of people who got in at the right time and are looking to cash out whenever there’s going to be some threat to their short-term gains. Outflows may accelerate if the macroeconomic situation gets worse. This may bring TROW’s share price further down, however, I think that it would be a great opportunity to add on such weakness if you are a long-term oriented investor.

The company’s fund may underperform the broad index, which may be a lost opportunity if you invested in TROW and not an ETF like SPY or QQQ, which have been outperforming TROW by quite a bit as I mentioned earlier.

Many economists and other professionals predict that there will still be further interest rate hikes, which will bring in further short-term volatility. Furthermore, the interest rates may stay higher for longer and that may lead to the company’s share price to continue its underperformance.

Closing Comments

I will be opening a position very soon, seeing that it hit my PT just a few days ago, however, the company is due to report results in less than 3 weeks, so I think I will start a small position in a couple of days and see what the management is saying about the remainder of the year and what kind of tone the management will have for the next year, if they will provide such an outlook. If I like what I hear, I will try to develop a decent-sized position. Plus, the dividend yield is very enticing at these prices.

The volatility may present an even better entry point, which I will take as an opportunity to add more shares if the results prove to be positive. I also believe there will be many opportunities over the next few months to start a long-term position because I don’t see macroeconomic sentiment changing for the better any time soon.

I believe that the risk/reward is very enticing here for the long-term investor, coupled with a decent dividend yield, there is no reason to panic during these tumultuous times when the macroeconomic path is uncertain. In the end, it will pass and 5 years from now, I see TROW going much higher. Even with my conservative estimates, the company seems like a value play to me that will pay off great in the future.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Value Idea investment competition, which runs through October 25. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Read the full article here