Investment Thesis

Health and beauty and specifically skincare is a large and expanding global opportunity. The Beauty Health Company (NASDAQ:SKIN) offers a non-invasive facial product called ‘HydraFacial’ and is creating a strong network effect of beauticians, spas, clinics and retail outlets and connecting them with affluent and aspirational consumers and the celebrities and influencers whose lives they covet. The company offers a razor and blade model that is growing albeit in a non-linear fashion. There is plenty of optionality and the company is pursuing potential new opportunities that could offer growth for years to come.

Investment Opportunity

Skincare is a growing industry with an estimated 29% increase in skincare specialist jobs by 2030 expected. This has led me to investigate a number of cosmetic and health and beauty companies. The Beauty Health Company is an ambitious, recently public company that offers a 3-stage facial product called ‘HydraFacial’ that cleanses and exfoliates skin, extracts impurities and then finally hydrates it. Most review websites have lists of glowing reviews. and YouTube and TikTok have plenty of positive looking before and after videos.

The company has been evolving the machines that provide these facials to consumers via the company’s customer – spa and salon owners, for many years with 2022 seeing its 10th iteration – Syndeo, which offers smart data collection as well as the optionality of treatments that go beyond facials, which offers potential optionality in the future. Early signs are that spas and clinics are upgrading to these new devices (about a 1/3 of sales in the first half of 2022 were upgrades from existing machines). I foresee these devices being used for future treatments for burns, scars, caesarean and birthmarks, etc.

The Beauty Health Company has one of my favourite business models – the razor and blade, by which salons and spas can buy the ‘delivery system’, which currently costs around $25000; these systems are unique to the company and patent protected. The ‘blade’ part of the model lies in the consumable parts that are used for each treatment – these are the tips that actually make physical contact with the skin, the treatment solutions and what I believe is the potentially most lucrative part, the treatment ‘boosters’ that customise and personalise treatments. Currently, there are 3 boosters that the company has internally developed and 14 that have been created through different partnerships. For example, Jennifer Lopez’s own cosmetic company branded booster is now available to consumers. These glamorous celebrity tie-ins, partnerships and endorsements are vitally important in the competitive health and beauty space.

The company is also creating a small amount of revenue in its training programmes for beauticians who can learn how to integrate the product into their salons and spas. As of its most recent investor day, the company had trained over 35,000 (a) estheticians to use its system in its 13 experience centres as well as in 75+ beauty schools around the world. This specialist training reminds me of the network effect created by Intuitive Surgical via its DaVinci systems, where surgeons are trained and feel confident using their devices making potential switching costs for hospitals very difficult. Further, the company also offers advanced training and qualifications through its 3 tiered professional training, which it refers to as “Like an MBA for aesthetics”.

Furthermore, the company is doing a good job of keeping up with new developments in skin care and looking for new growth drivers. One example is an upcoming ‘exosome’ booster. Early evidence suggests that among their potential uses, exosomes can be used to rejuvenate skin, and it appears to be a potentially lucrative new marketing product. Google ‘exosome beauty’ and you’ll probably find some outrageously expensive creams and products that are on or coming to the market soon. The company is also looking to tap into the growing hair restoration market, currently around a $5 billion a year industry, through the topical use of its ‘Keravive’ product that can be administered by doctors and in medicinal spas and clinics.

In terms of increasing the exposure of its product, the company is working hard to bring high profile spas and beauty salons as well as large chains into its ecosystem. For example, it offers a product called ‘Perk’ as a quick in-store treatment in LVMH-owned (OTCPK:LVMHF) Sephora, a cosmetic chain with over 2600 stores around the world. Further, in April this year, the company launched a new exclusive facial for Dior Spas.

Investment Risks

The beauty industry is robust and ostensibly recession proof albeit women will often trade down clothes and trade up smaller luxuries as per the ‘lipstick effect’ during recessionary periods. However, with prices recommended by the company as being between $150 and $500 for a facial, HydraFacial treatments as well as the spa and salon visits within which they are likely administered are likely to be sacrificed or at least reduced during recessionary times. I can see this either being a short-term headwind or a factor that causes some fluctuating growth in the next couple of years as consumer spending varies.

The company is currently spending a lot on marketing, around 40% of its total revenue, albeit down 7.8% year on year. My hope for the company moving forward is that it benefits from a combination of word of mouth, social media campaigns and its investment in celebrity and influencer partnerships and can slowly reduce its reliance on such heavy marketing spend. There is plenty of competition for the health and beauty consumer dollar, but the company does have something I believe to be quite an innovative niche. Similarly, I find it a little disconcerting that the company is only spending 1.4% of its current operating expenses on research and development of new products, despite the high levels of science and progress that the company implies in its reports.

Management company’s 5-part ‘master plan’ is to: expand its presence into more spas and clinics as well as retail stores, develop its relationships with beauticians, build out brand awareness, spread internationally and make acquisitions. It is a very ambitious plan and there is certainly execution risk as to whether management has the ability to develop products, increase sales, build relationships with its providers, offer training and expand internationally effectively and simultaneously. Time will tell in future earnings reports as to whether they can successfully spin so many plates.

Finally, currently, around 25% of the company’s shares are short (down from around 35% a month ago) despite the stock already falling around 60% from all-time highs, which indicates that the market still has doubts over the company.

Investment Chances of Beating the Market

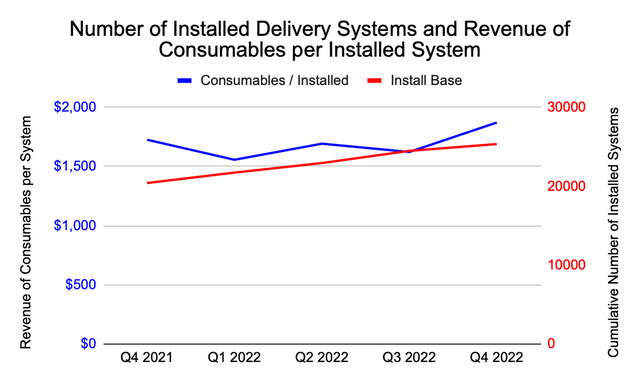

Part of my thesis is that this is a razor and blade model, and digging into the numbers, I like what I see. Firstly, take a look at the red number. That is the cumulative number of installed delivery systems in spas, clinics and retail outlets internationally. It is increasing steadily. The blue line is the total consumables revenue from the company’s income statements divided by the installed number of delivery systems. The line is a little less directly up and to the right; however, it is trending upwards, which means that each system is seeing an increase in the amount of revenue being generated. Assuming this continues, the company will grow nicely into the future.

Number of Installed Delivery Systems and Revenue of Consumables per Installed System (Compiled by Author from Information from Company’s Earnings Presentations)

Looking forward, management is aiming for the company to double its revenue by full year 2025, targeting $600-$700 million per year with an adjusted EBITDA margin of between 25%-30%. These are quite ambitious targets that come in at around 25% CAGR for sales over the 3 years. However, this is a growth story and with the flywheel of recruiting clinics, upselling existing customers to newer machines, selling more and more consumables and connecting consumers with celebrities and influencers, I can see strong growth over the next few years assuming the macro level economic issues do not bring about a heavy global recession.

Taking management’s guidelines out to 2025 and then tapering sales growth down to a conservative mid-single digit year-on-year percentage over the next decade, I get a revenue of around $1.5 billion per year by 2033. Here are my assumptions:

|

Revenue |

Growth % |

|

|

2021 |

$260 |

– |

|

2022 |

$366 |

40.69% |

|

2023 |

$443 |

21% |

|

2024 |

$536 |

21% |

|

2025 |

$648 |

21% |

|

2026 |

$765 |

18% |

|

2027 |

$879 |

15% |

|

2028 |

$985 |

12% |

|

2029 |

$1,083 |

10% |

|

2030 |

$1,181 |

9% |

|

2031 |

$1,275 |

8% |

|

2032 |

$1,365 |

7% |

|

2033 |

$1,447 |

6% |

With management’s future adjusted EBITDA margin between 25%-30%, I’ve gone with the lower figure and applied a tax rate of 25%. This gives us a 2033 EBITDA of $361 million per year and, assuming no debt interest and not factoring in depreciation and amortisation, a net income of $271 million.

For a quick and dirty 2033 valuation, let’s go with market averages with a PE of 15 and a price to sales of 3. This gives us the following numbers:

|

PE of 15 x 2033 EBITDA with 25% tax rate, assuming no debt and no adjustments for depreciation and amortisation |

$4,068.39 |

|

Price to sales ratio of 3 x 2033 revenue |

$4,339.62 |

|

Averaged of the two market cap |

$4,204.01 |

|

Current Market Cap (at time of writing) |

$1,392.10 |

|

Annual Return assuming no stock dilution or buybacks |

11.69% |

I believe that if the company is able to achieve a 11-12% return over the next decade, it will likely beat the market.

Investment Summary

The Beauty Health company has a popular product. Its razor and blade model is working well to both sell delivery systems (as well as upgrade existing ones) and increase the consumable parts that are required to offer the HydraFacials. There is plenty of optionality, with treatments in retail cosmetic stores as well as moving beyond the face to addressing cosmetic and low-level medical skin needs.

If management can continue to balance international growth, developing its offerings to practitioners, marketing the product both directly to consumers and to its business customers and finding an appropriate level of sales and marketing spend, we could have a great opportunity at a reasonable price. If the company executes its plan, I believe it will deliver a market-beating return over the next decade, which is my default time for considering an investment. I rate it a cautious buy.

Read the full article here