In my initial write-up on Veeva Systems (NYSE:VEEV) back in late January, I called VEEV stock one of the most attractive SaaS stocks out there. With the company reporting results earlier this week, let’s check in on how it’s been doing.

Q1 Results

For the quarter ended April, VEEV saw revenue increase 4% to $526.3 million. Subscription revenue moved 3% higher to $414.5 million. Service revenue rose 9% to $111.8 million. Analysts were looking for revenue of $517.3 million.

The company saw a $51 million revenue impact from the standardization of termination for convenience rights. This accounting change impacts multi-year ramping contracts. Excluding the TFC impact and currency, revenue rose 16% and subscription revenue jumped 17%.

Commercial Solutions subscription revenue rose 5% to $239.4 million, while service revenue for the segment rose 4% to $44.9 million. Management said it added 11 new SMB customers in the quarter for its core CRM product.

The company noted that it is adding an AI application called CRM Bot for its Vault CRM product. The product will be a separate license, but it does not have pricing for it yet, as it focuses on getting the product right.

R&D Solutions revenue edged up to $175.2 million, essentially flat versus a year ago. Service revenue for the segment jumped 13% to $66.9 million.

The company said it added its second enterprise agreement for its Vault Safety product in the quarter. It also added 26 new customers for its Vault Quality solution.

Adjusted EPS came in at 91 cents, easily surpassing the analyst consensus of 80 cents.

Normalized billings were up 11% year over year to $554 million. This came in ahead of company guidance due to more new business having annual terms than expected.

The company generated $444 million in adjusted operating cash flow, which excludes a tax benefit of $62 million. It ended the quarter with more than $3.6 billion in cash and short-term investments and zero debt.

Overall, when you strip out the TFC adjustment, VEEV reported a solid quarter. R&D Solutions, while seeing its GAAP revenue flat, continues to be the growth driver, as evidenced by its strong service revenue growth and customer wins. CRM Solutions, while more mature, also continues to grow. The resiliency of VEEV’s customers was evident in the quarterly results.

Adjusted EPS nicely beat the consensus, which in part is likely due to higher interest rates. VEEV carries a lot of cash and short-term investments, which is helping bolster its bottom line and add some additional cash flow as well.

Outlook

Looking ahead, VEEV forecast fiscal Q2 revenue to come in between $580-582 million. That includes a $17 million TFC standardization impact headwind and a $5 million currency headwind. The analyst consensus was for Q2 revenue of $580.1 million.

Adjusted operating income is projected to be between $199-201 million, while adjusted EPS is projected to be between $1.12-1.13. The analyst consensus was for Q2 EPS of $1.06.

It is looking for normalized billions to be about $529 million for the quarter.

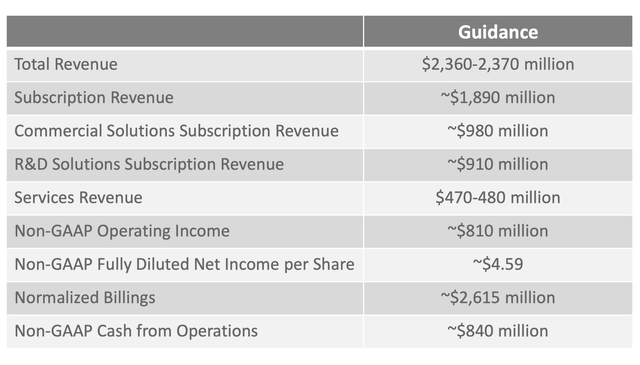

VEEV 2023 Guidance (Company Presentation )

For the full year, VEEV is guiding for revenue of between $2.36-2.37 billion, an increase of $10 million from its previous guidance. The forecast includes a $95 million impact from TFC standardization and $15 million in currency headwinds.

Subscription revenue is projected to be between about $1.89 billion, up $10 million from its prior forecast. Commercial Solution revenue is expected to come in around $980 million, while R&D Solutions revenue is forecast to be approximately $910 million.

VEEV is projecting adjusted operating income to be $810 million, with adjusted EPS of around $4.59. The company previously guided for full-year EPS of $4.22 and the consensus was for EPS of $4.32.

It is looking for normalized billings to be about $2.615 billion for the year, up 15%. Over 40% of its billings are expected to occur in Q4.

The company expects adjusted operating cash flow of $840 million. That’s a $30 million increase from its earlier guidance. The higher forecast is partially helped by an expected increase in interest income.

VEEV also reiterated its fiscal 2025 guidance calling for revenue of at least $2.8 billion and at least $1.0 billion in adjusted operating income.

Discussing the macro environment on its Q1 call, CEO Peter Gassner said:

“In general, the industry operates on pretty long cycles, especially our very established and large customers. So the ups and downs of the macro environment don’t really affect them too much. We do see a little bit more effect in what we call our emerging biotech. These are small customers, generally don’t have an approved product. So we see — when funding gets tight, we see a little bit of pressure there. But nothing that really has changed in the last 90 days at a macro level. So I guess that’s why we’re not so susceptible to those small ups and downs and business just continues to move forward.”

The company noted that about 4% of its total revenue comes from emerging biotechs that have no approved products.

VEEV nicely increased it guidance for the year, which is what investors like to see from a growth company. While the $10 million boost to revenue is pretty small, given the current macro environment and lower expectations, that was enough to help nicely lift the stock following its report. Expectations are always one of the biggest factors around earnings reports, so having lowered investor expectations is always nice.

The bottom line and cash flow forecasts were lifted even more, which reflects VEEV’s strong cash position and the impact of higher interest rates on that strong cash position. At some point you’d like to see VEEV use that cash in a productive way, such as buying back shares, acquisitions, or even paying a dividend. However, with where interest rates are currently, cash is not a bad thing to have at this point.

Valuation

VEEV currently trades at under 10x fiscal year 2024 (ending in January) revenue of $2.37 billion. (EV/S), while its EBITDA multiple is 28x based on the consensus of $824.3 million.

For fiscal-year 2025, it trades at 8.2x revenue estimates of $2.82 billion and 22x the adjusted EBITDA consensus of $1.05 billion.

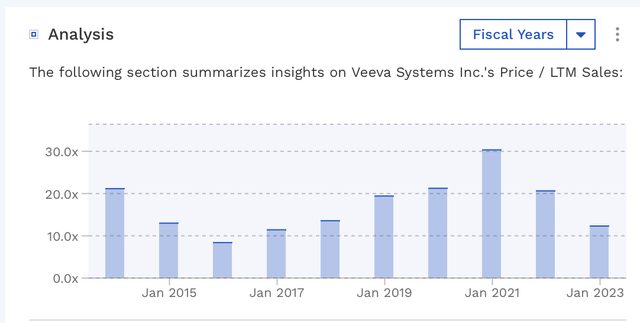

VEEV has historically traded at a high P/S ratio, with a P/S ratio of over 19x for four of the past five years. You’d have to go back to 2016 to see a ratio under 10x.

VEEV Historical Valuation (FinBox)

Conclusion

VEEV has continued to demonstrate the characteristics that led me to place a “Buy” rating on the stock in my initial write-up. It is the dominant player in the life sciences niche with its CRM and drug development SaaS offerings. Its solutions are extremely sticky, and its customers by and large are pretty unaffected by the macro environment.

While the stock is not in the bargain bin, it’s not out of line for a strong grower serving a largely recession-proof industry. Meanwhile, I like the nice win for its Quality Suite product during the quarter, and think this product suite can eventually get the company into some adjacent industries once its deal with Salesforce.com (CRM) winds down.

While not quite as attractively priced as before earnings, I continue to rate VEEV stock a “Buy.”

Read the full article here