Solid Business Model

We do not believe the economy and stock market are stable enough for retail value investors to take unwarranted risks. Predictions persist for a mild recession in 2023, or a deeper worldwide recession next year.

We like solid, stable companies in basic and essential industries; that is why we are bullish about Methode Electronics, Inc. (NYSE:MEI), as the share price recently dipped. Methode is a global developer and seller of custom-engineered solutions for User-Interface, LED lighting, sensors, chassis, and powertrain distribution applications.

The price plopped from nearly $50 per share to ~$37, so we are upgrading our assessment from the Hold rating assigned in our previous article for Seeking Alpha to judge it as a Buy at this time. The share price has not been this low since last October. At the time of our September 2020 article, the share price was $28. It slipped to $24, then climbed over the next eight months to nearly $50. It wandered around below $50 then slipped 9% the second week of June ’23.

Managing The Numbers

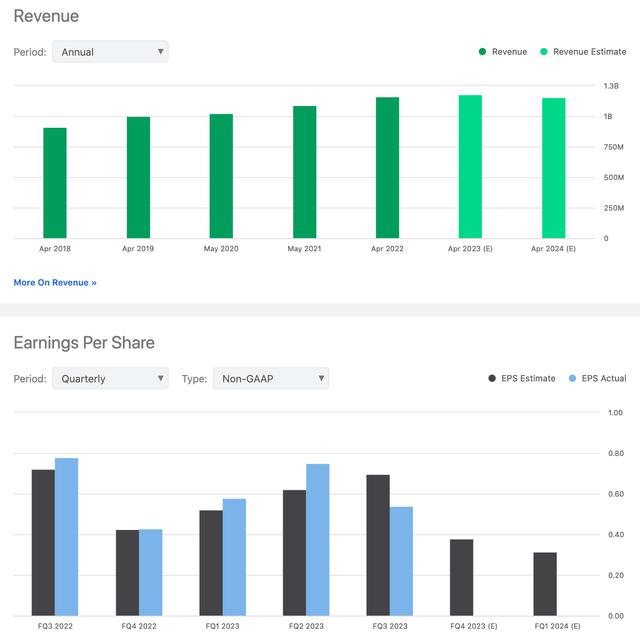

Revenue and Earnings (seekingalpha.com/symbol/MEI)

The company’s explanation is confirming of the investment community’s reservations about consistent macroeconomic growth and government spending in FY ’23. EPS expectations are for:

… revenue of about $1.183B for FY 2023, compared to an earlier anticipated range of $1.155B to $1.18B. The consensus revenue estimate is $1.17B. MEI slashed its GAAP EPS expectations for FY 2023 to a range of $2.10 to $2.14 from a prior range of $2.50 to $2.60. The consensus EPS estimate is $2.51… Additionally, for fiscal 2024, MEI said it anticipated EPS of $1.55 to $1.75 on revenue of $1.15B to $1.20B. The consensus estimates are $2.58 and $1.19B, respectively.

Methode’s CEO, Donald Duda, went on to predict lower sales and earnings in FY ’24 due to program roll-offs as well as market headwinds in commercial vehicles, data centers, and e-bikes, but FY ’25 is expected to enjoy significant increases in organic sales and earnings. We forecast the Q4 ’23 EPS, scheduled to be announced on June 22, 2023, will be perhaps two or three cents higher than the $0.43 for last year’s Q4. Methode beat EPS forecasts in 8 of the last 9 quarterly reports.

Coming off 6 consecutive years of record sales, the prognostication has not apparently phased investors. Between January ’23 and May, insiders executed 15 buying stock trades and 7 sales of stock. Hedge funds slightly increased their holdings in the last quarter. Moreover, Methode Electronics was owned by 8 to 10 funds between Q2 ’21 through Q4 ’22. By the end of Q1 ’23, 13 funds held positions.

The stock currently holds a 1.38 Beta rating, but short interest remains relatively low (~3.7%); we do not foresee any reasons for the price to drop significantly. In March, the company declared a $0.14 share quarterly dividend, in line with previous ones. Seeking Alpha’s Quant ratings assign As and Bs to the dividend for its safety, growth, yield, and consistency. Not much for retail value investors to worry about here. In fact, we consider the company’s overall health pretty well-founded.

Analysis (infrontanalytics.com/fe-en/US5915202007/Methode-Electronics-Inc-/beta)

Good For The Long-Term

Methode Electronics’ capital structure is solid. We believe the company enjoys a strong balance sheet. Its market cap is $1.37B. It carries $231.1M in debt that is underpinned by $164.7M in cash. That’s down over $215M the year before. The enterprise value stands after the last quarter’s report at $1.44B.

Management’s plan has been in part to grow the company through M&A. They bought 14 companies over the years in the electrical equipment (36%) and automotive (22%) industries. In May, management announced the acquisition of Nordic Lights Group Corp, a premium maker of equipment sold to mining, construction, forestry, agriculture, and material handling. More acquisitions, at a time when revenue and earnings are threatened for 18 months, seems like swashbuckling in our view. Over a longer term, with the 2025 EPS expected to top $2.75 compared to $2.14 in 2023, and free cash flow of $4.22 per share that currently stands around 82% of its EBIT, investors can be at ease unless the 2024 business environment turns sour.

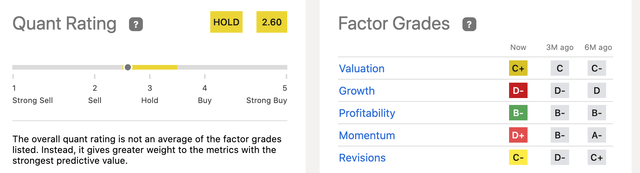

Quant & Factor Grades (seekingalpha.com/symbol/MEI/ratings/quant-ratings)

Seeking Alpha Factor Grades for Methode Electronics are mixed. The metrics for valuation are all As and Bs except for the dividend yield (C+). The Quant Rating suggests investors be cautious, though it leans to the bullish side of the scale. The average target price is probably going to hover around $39 per share, factoring in the anticipated PE of 17 and EPS of $2.25 for 2023. It can potentially return to the mid-$40s if the June ’23 announcement is better than expected and business is better than the dour (-22%) predictions for earnings growth.

Takeaway

Methode Electronics, Inc operates in four segments: automotive, industrial, interface, and medical. The automotive industry is negatively affected by higher interest rates and persnickety supply chain issues that in turn stifle growth for the segment’s suppliers. U.S. industrial production is haphazard at the present time, -0.2% M/M for May ’23. Interface and medical are going to have modest growth over the next few years.

In our bullish opinion, the dip in share price makes it attractive for investors in basic essential industries. We believe Methode will weather the economic headwinds and the stock will stabilize; the share price can potentially climb higher on almost any good news that affects the company, making it a worthwhile opportunity for retail value investors confident in the American economy.

Read the full article here