One year later, tech stocks aren’t dirt cheap anymore. Zscaler (NASDAQ:ZS), like many of its tech peers, has responded to the tough macro environment by delivering resilient revenue growth alongside expanding operating margins. ZS has benefited from an unusual “flight to safety” among its customers who have shown a preference for vendors with more complete platform offerings. While the stock has regained a healthy valuation, I suspect that Wall Street may reward tech companies like ZS with premium valuations moving forward due to their strong performance in the current environment. I expect cybersecurity tailwinds to continue powering above-market growth rates for this company – I reiterate my buy rating for long-term minded growth investors.

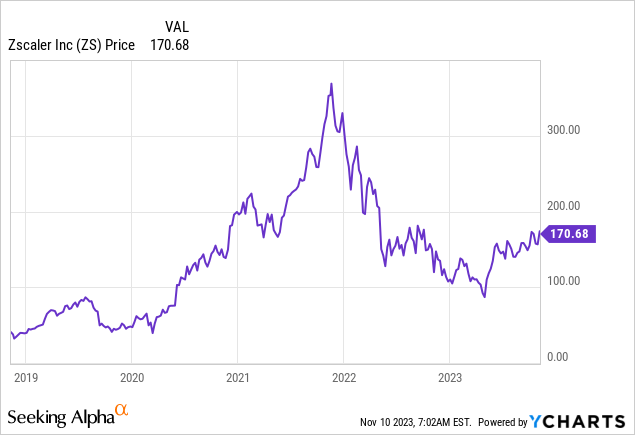

ZS Stock Price

It can be hard to believe, but it was as recently as May of this year in which Wall Street possessed substantial doubt in the stock of ZS, at one point sending the stock to the low $80s. The stock has since rebounded strongly off the lows as the company’s financial results have proved doubters wrong.

I last covered ZS in August where I acknowledged that even I, as a consistent bull, was not optimistic enough for the company’s prospects. Even as tough macro headwinds persist, I remain favorable on the stock at current valuations.

ZS Stock Key Metrics

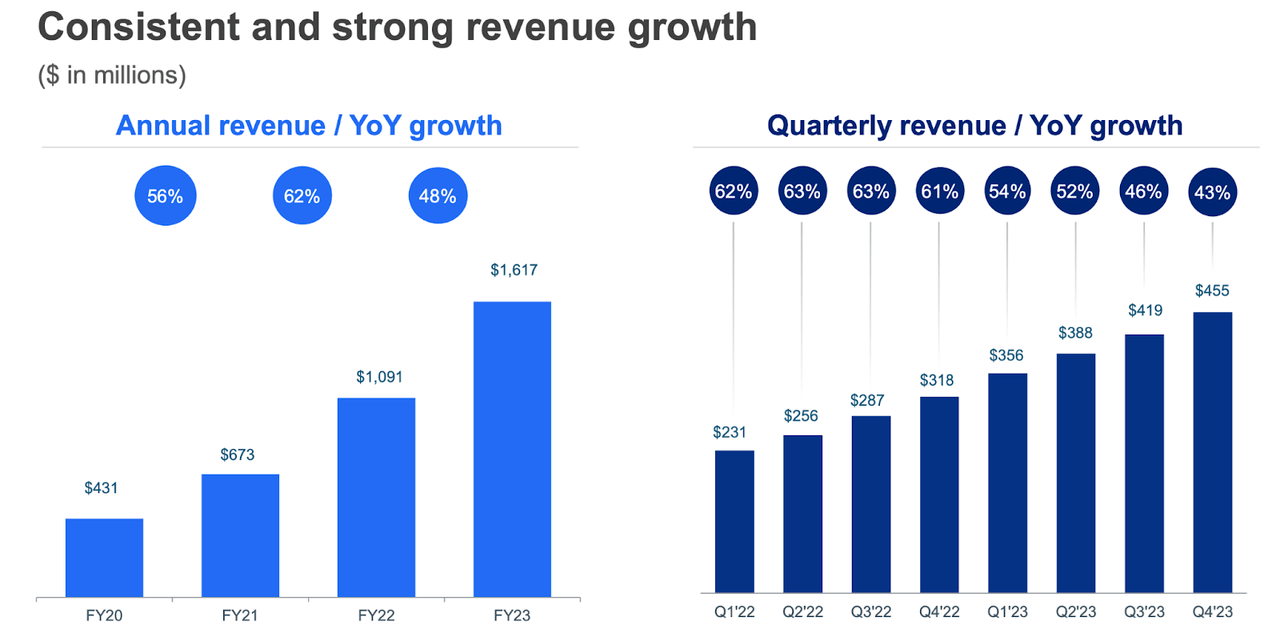

In its most recent quarter, ZS delivered 43% YoY revenue growth to $455 million, coming well ahead of guidance for $431 million. Hopefully it does not need to be stated that beating and raising guidance in this tough macro environment is no easy feat.

FY23 Q4 Presentation

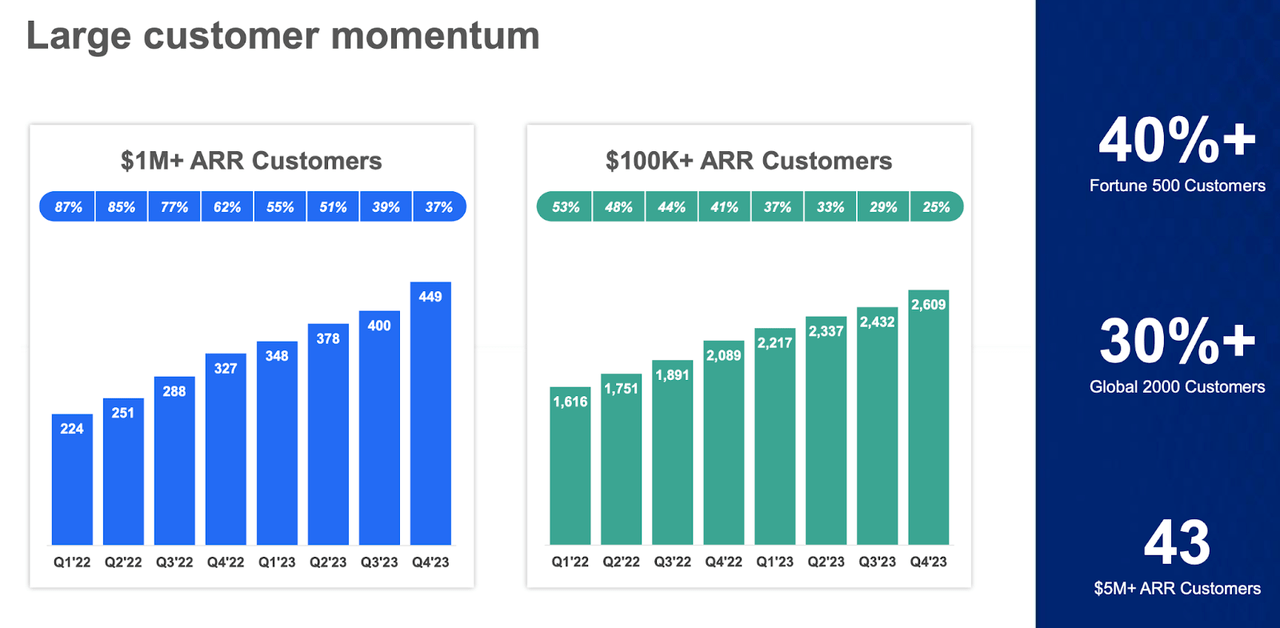

While smaller operators have seen customer growth slow down dramatically, ZS continues to add to its customer base, especially among larger customers.

FY23 Q4 Presentation

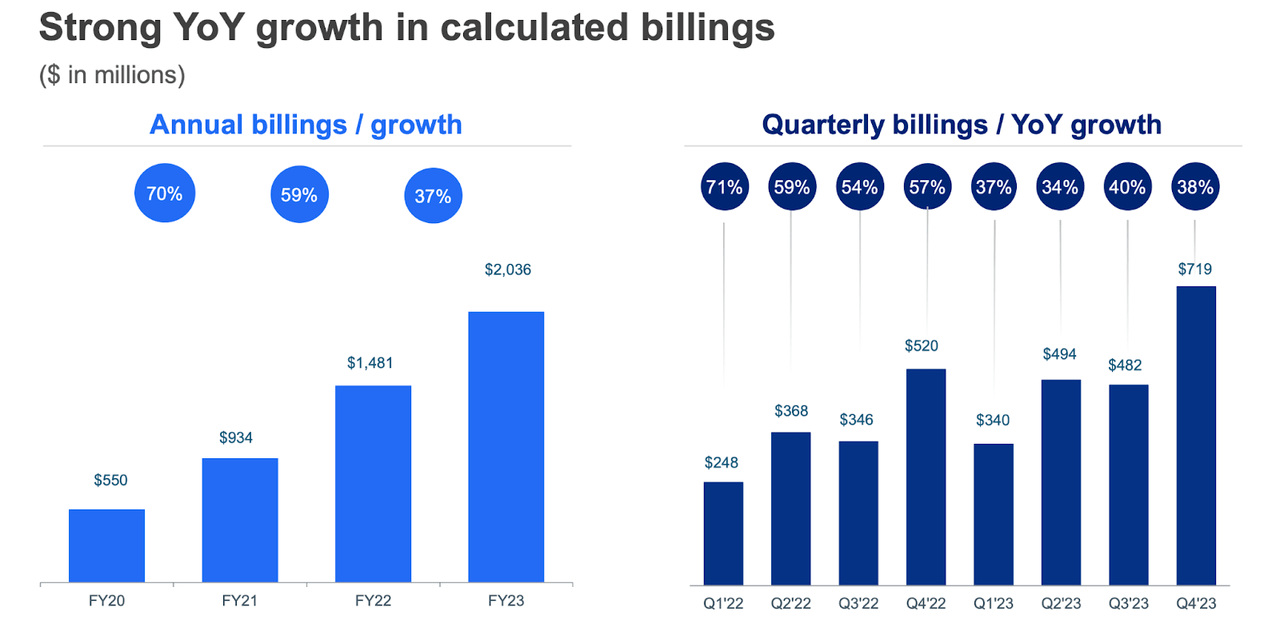

ZS coupled the strong revenue growth with 38% billings growth. Billings growth can often foreshadow future revenue growth, so that strong number has eased investor concerns about a dramatic slowdown around the corner.

FY23 Q4 Presentation

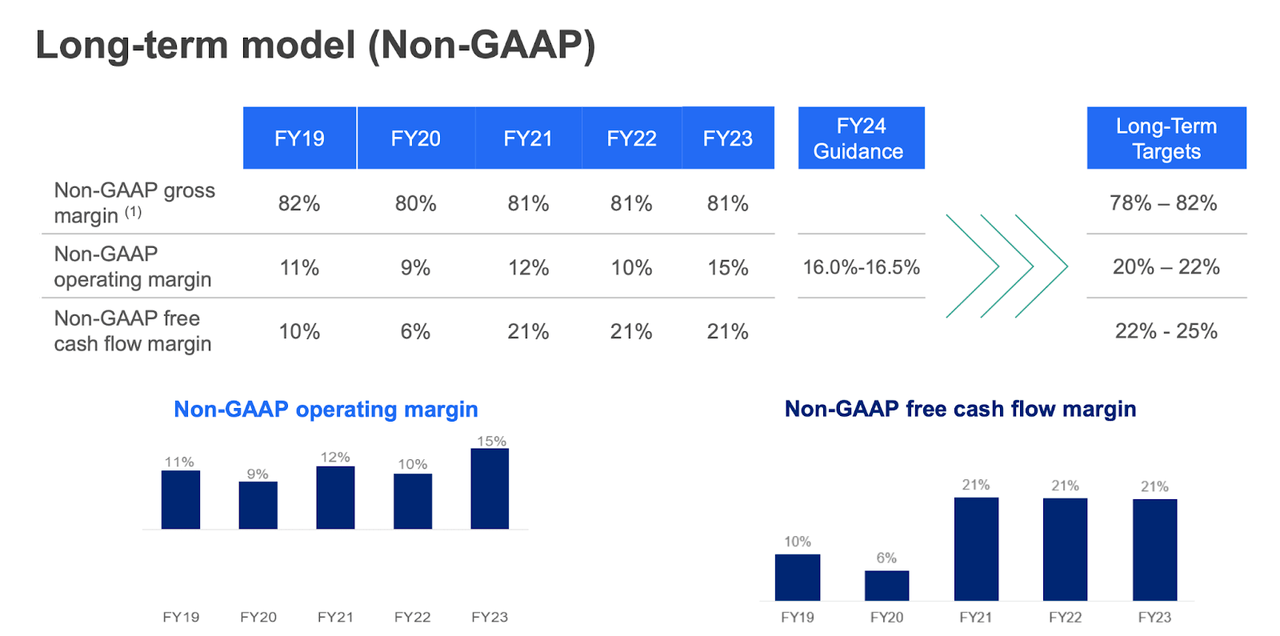

ZS ended the year with a 15% non-GAAP operating margin and 21% free cash flow. The company continues to work towards its long-term targets of over 20% in profit margins.

FY23 Q4 Presentation

ZS ended the quarter with $2.1 billion of cash versus $1.1 billion of convertible notes. Together with its positive cash flow generation, this represents a strong balance sheet.

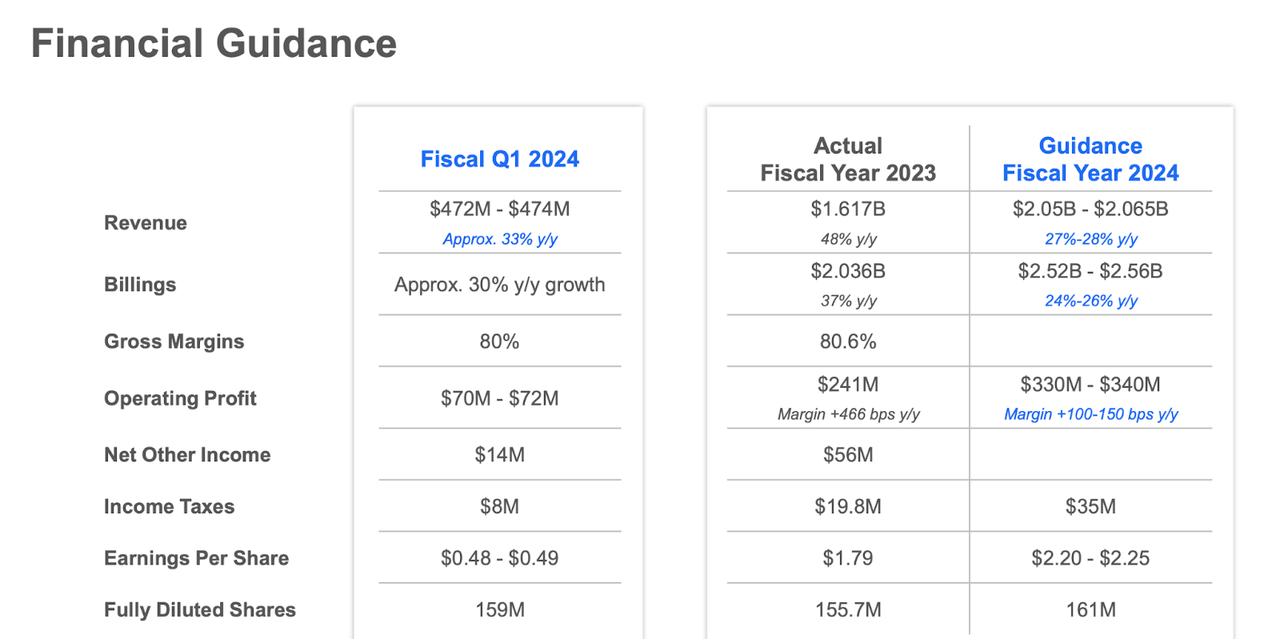

Looking ahead, management has guided for 33% YoY revenue growth in the upcoming quarter and 28% YoY revenue growth for the full year. Management expects to deliver over 100 bps in operating margin expansion as well.

FY23 Q4 Presentation

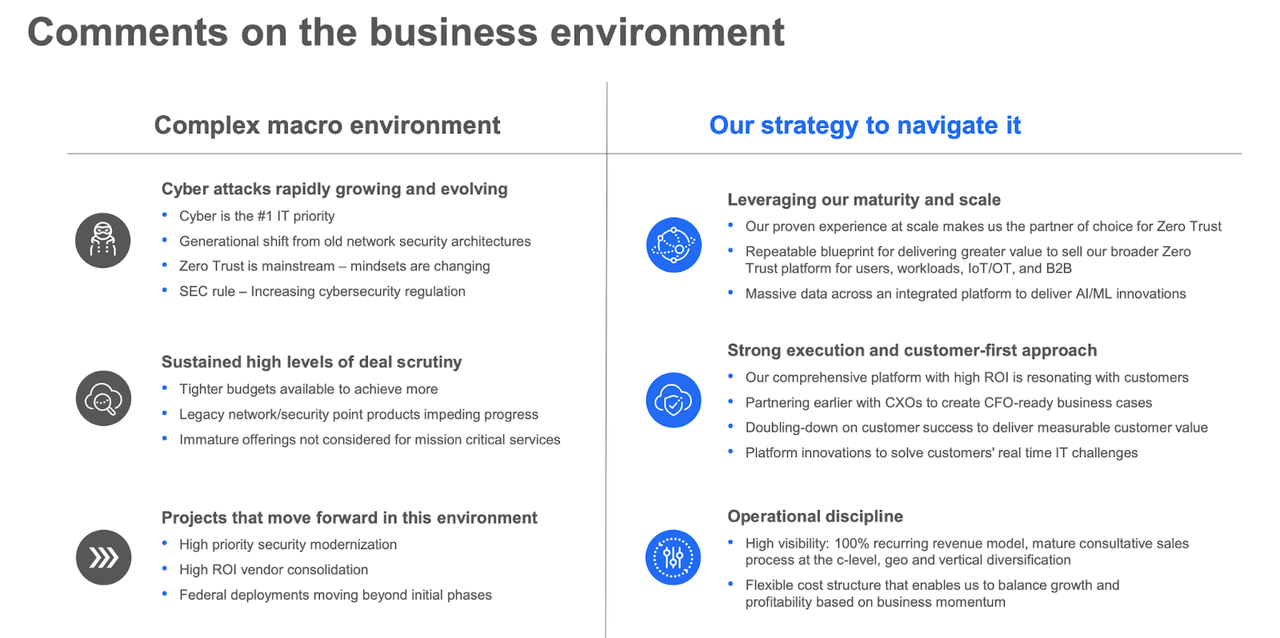

On the conference call, management noted that their guidance incorporates a similar macro environment as this past year. Management credited their strong results to their view that “good enough in cybersecurity is never good enough.” This tough macro environment has ironically proven to offer competitive tailwinds for the stronger platform companies like ZS as customers have shown a greater preference for more well-known names. Management described their positioning in a generative AI world as including their ability to allow customers to restrict how employees use generative AI, helping to protect against sensitive information being released into generative AI prompts. ZS stock briefly sold off in the quarter on news that Microsoft (MSFT) was entering the space. Management appeared unconcerned about the perceived threats, noting that they have strong positioning in the large enterprise market but noted that lower end operators may feel more impact.

Is ZS Stock A Buy, Sell, or Hold?

The tough macro environment – spurred by rising interest rates and recessionary fears, has impacted the secular engine through tighter IT budgets and resistance to begin new projects. ZS has somehow bucked that trend in large part due to being a well-known mature operator with a large product portfolio. Cybersecurity is also one of the few sectors which has not been meaningfully impacted in terms of importance as cyber attacks care little about prevailing interest rates.

FY23 Q4 Presentation

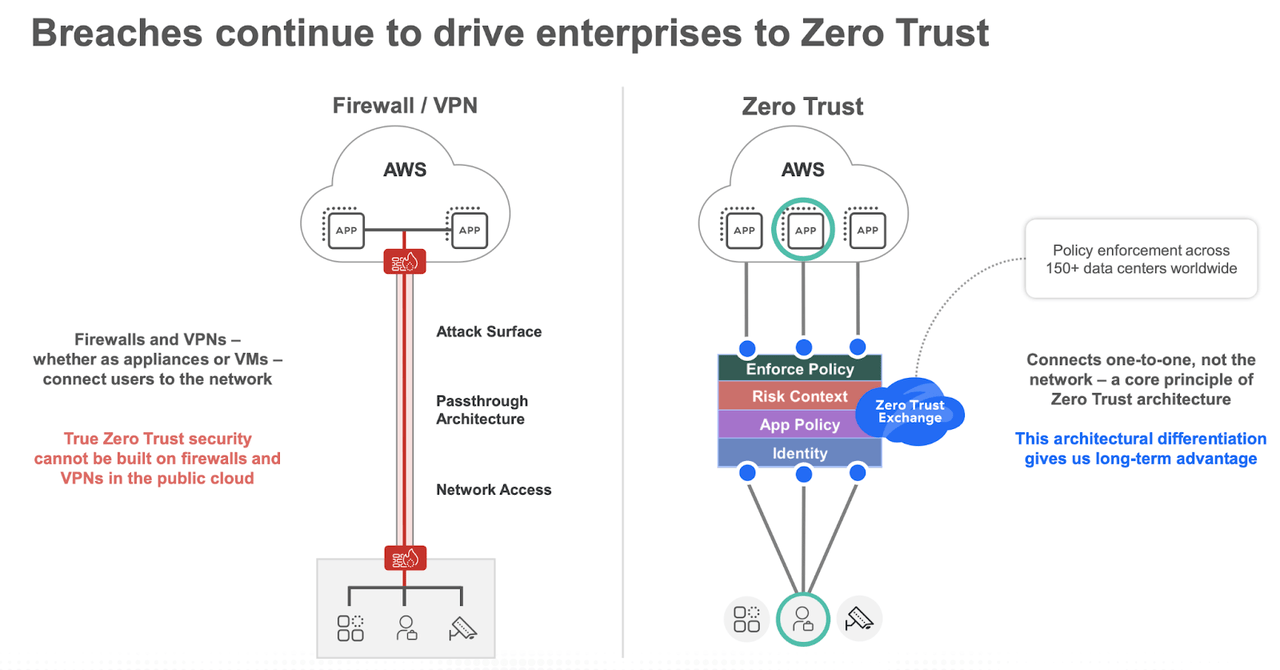

Within the cybersecurity sector, ZS is disrupting the legacy firewall protection providers. The problem with conventional firewall/VPN security is that it only protects access to a network. Once bad parties get access to the network, they have access to everything. With ZS’ zero trust architecture, they are able to secure access on a customizable basis at a per-app level.

FY23 Q4 Presentation

After the robust recovery, ZS is now trading at around 12x sales – a healthy but very reasonable valuation for a best-in-class operator with a strong balance sheet and secular tailwinds for as long as the eyes can see. With premium-valued stocks like this, understanding of the drivers of the growth story is very important. Cybersecurity has proven itself to be one of the elite sub-sectors within tech through its resilient results in this environment. Cybersecurity isn’t something that ebbs and flows with the economy – if anything, customers arguably should be more worried about cyberattacks during difficult times. With the rise of generative AI, the importance of generative AI has only increased, as cyber attackers now can utilize generative AI in their campaigns. I expect generative AI – alongside an improving macro – to help power top-line growth for top tier cybersecurity operators over the next decade, even while most tech peers are seeing rapidly decelerating growth rates.

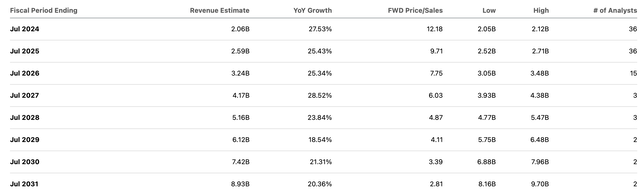

Consensus estimates call for solid revenue growth even beyond 2024. While decelerating growth rates is always a risk, Wall Street retains hopes that an improved macro environment can drive strong growth moving forward.

Seeking Alpha

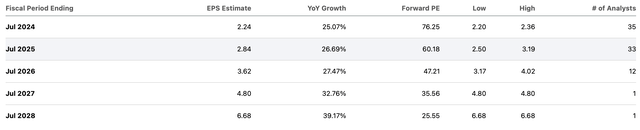

ZS is expected to generate strong operating leverage as well, with its net margin expanding to 19% by 2028.

Seeking Alpha

I continue to use my assumptions of 25% top-line growth, 30% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’). That leads to a valuation of around 11.3x sales, implying strong upside over the coming years from ongoing growth. I am of the view that high quality tech stocks deserve a 1.5x PEG ratio, or better, due to their recurring revenue business models as well as their strong financial performance during this tough macro environment.

What are the key risks? The most glaring risk is the potential for consensus estimates to prove too aggressive. Cybersecurity has admittedly been one of the more resilient subsectors in tech, seeing far less deceleration in top-line growth rates than peers. It is possible that it is just a matter of time before “gravity” catches up to cybersecurity names. It is also possible that the macro environment worsens such that top-line growth is pressured. ZS is trading at a valuation that is pricing in forward growth, as the stock does not trade with immediate upside potential from a multiple expansion perspective (at least based on my fair value estimate). If sentiment were to worsen, as it did during the 2022 crash in tech stocks, then ZS may see some volatility. I am not so concerned from a financial perspective due to the profitability (albeit on a non-GAAP basis) and the net cash balance sheet, but investors with weak stomachs should be forewarned. While MSFT does not appear to be a threat at least in the near term, it is always the elephant in the room and perceived competition may eventually impact valuations.

I reiterate my buy rating for the stock, even though the ongoing rally has removed any obvious multiple expansion potential. I view ZS as one of the higher quality growth stories in the market and one worth paying a premium for.

Read the full article here