We continue to closely follow the operational performance of a number of banking institutions, as they are the backbone of the state of small businesses and consumers in the United States. We are in a debt-fueled economy, and the access to loans is crucial to keep the economic engine of the nation humming. There has been great concern with the rise in interest rates causing loan demand to dry up, and even worse, concerns over customers being able to pay their debts. Another engine of America is our farmers, and their need for capital to purchase machinery, livestock, and churn out their crops.

Today, we turn to Farmers & Merchants Bancorp (OTCQX:FMCB). The stock has been relatively stable in this chaos, and the three-year chart is favorable. We rate the stock a hold in this environment, but note it is a dividend king. The company has raised its dividend for 58 consecutive years. However, the flipside to this is a stable stock. So, it is a great hold for dividend growth investing.

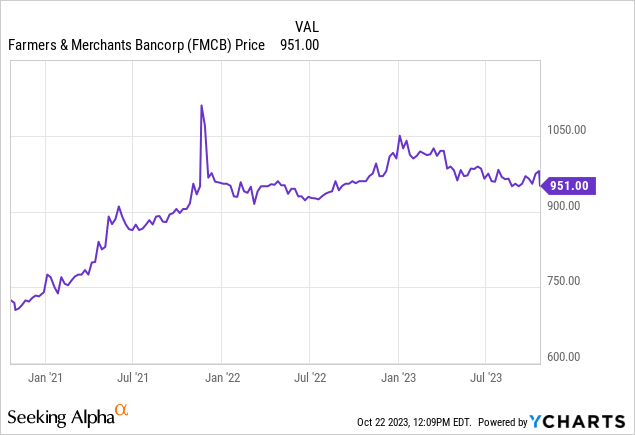

The bank just reported Q3 earnings, and in this column we examine the key metrics we follow for regional banks. First, take a look at the chart:

As you can see, the stock has held pretty steady in the $900-$1,000 range, with a few peaks above $1,000. This action comes with that growing dividend every year. This is, of course, a small regional bank, with 32 branches across the Central Valley and East Bay areas in California. It is a major bank lender to agriculture in the U.S. and has been recognized by the many rating firms as one of the safest banks operationally for several years in a row. Our review suggests that this company has had strong financial metrics for years, and in Q3 this was no exception. Now, the bank is not immune to this climate, but is very strong relative to the many other regional banks we have covered.

We think this weakened state for banks will be coming to an end in 2024. We believe this assuming the Fed’s rate hiking campaign will be coming to an end. Further, we see margin expansion as likely, as future loans are going to made at higher yields, while we see the cost of funds peaking. As such, we think the trough in margins for the industry will occur in the next quarter or two. The market has priced in earnings declines and pressure in net interest income for banks. But this bank has a strong track record of profitability and growth, and it is well-capitalized.

In Q3, Farmers National Banc Corp. saw strength. There have been concerns with deposit declines, or lack of loan growth. This was not the case with this quality bank. Growth in deposits were 2.38% and loans grew 1.88% compared to the second quarter 2023. Many other regionals we have covered have seen declines in one or the other, if not both.

Now, the main concern has been a narrowing of margins. While we have projected margins to trough for the sector in 2024, if not sooner, this bank is expanding margins. Yes, in a climate where banks are almost universally seeing margin decline, Farmers and Merchants expanded their margins. Net interest income for the quarter was $53.4 million, an increase of $3.0 million, or 5.9%, when compared with $50.5 million in the same quarter in 2022. Net interest margin increased to 4.20% compared with 3.95% in the third quarter of 2022. This is impressive year-over-year growth, driven by increased loan yields that outpaced the increase in costs of deposits.

On the earnings front, this bank is incredibly profitable. Net income was $22.0 million, or $29.23 per share. This EPS was up 16.0% from a year ago. That is stellar performance. And for the trailing 12 months, earnings were $114.13 per share. Folks, that means the stock trades less that 9X trailing EPS, and for all of 2023, we are projecting $120 in EPS, putting the stock at 8X FWD EPS. Very attractive.

What is most impressive is that the bank still has industry-leading asset quality. The return on average assets was 1.65% and return on average equity was 16.80% in the quarter. Where many other regionals are seeing declines from a year ago on these metrics, both were up compared with 1.45% and 16.64%, respective, from Q3 2022. The efficiency ratio even improved to a stella 42.89% compared with 46.86% a year ago. Very few regionals sport a sub 50% efficiency. However, the bank is not completely immune to pressure. While the credit quality remained incredibly strong with only $4.5 million of non-performing loans, the delinquency ratio of 0.19% did tick up from 0.02% last year.

That said, this was due to one borrower facing issues. As such, Farmers recorded a provision for credit losses of $3.0 million and an allowance for credit losses of $74.2 million, or 2.08% of total loans and leases as of which ticked up from 2.03% in Q2, the sequential quarter. This was one blemish in an otherwise strong quarter

Take home

The bank is in a tight range trading wise, and is a dividend growth king. Overall, Farmers & Merchants Bancorp is in very healthy shape and is an under-the-radar name. We would hold the stock until shares are closer to $900, when we would then pull the trigger. The margins expanded, earnings are growing, and asset quality remains incredibly strong.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here