Introduction

It’s time to discover a stock I have never covered before. Organon & Co. (NYSE:OGN) is a woman’s health-focused healthcare spin-off that isn’t doing so well – at least when looking at its stock price.

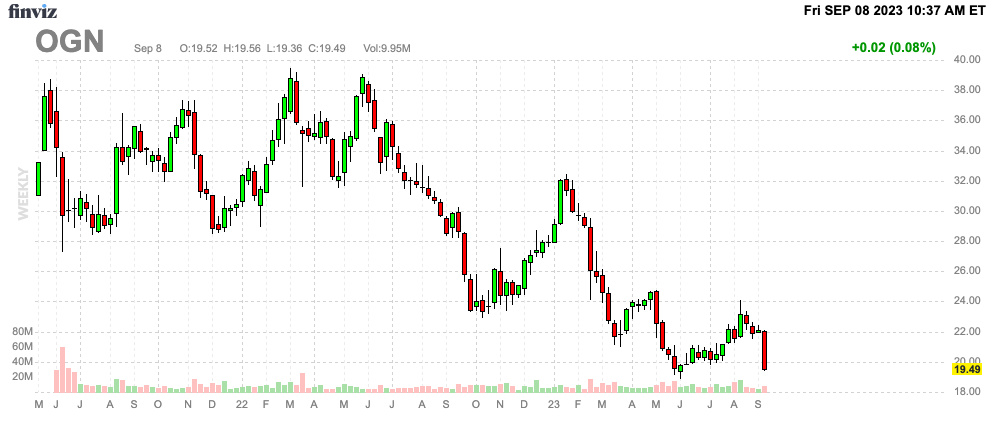

FINVIZ

OGN shares are down 30% year-to-date and more than 40% below their 52-week highs.

The good news is that its dividend yield is now 5.8%, which is the reason why I’m writing this article.

While OGN comes with a lot of spin-off debt and barely any growth over the next few years, its dividend is protected. At current valuations, OGN might be worth a shot for income-oriented investors looking for a potential deep-value play.

Now, let’s dive into the details!

What’s OGN?

Headquartered in Jersey City, New Jersey, Organon is a spin-off of Merck & Co. (MRK). In 2021, the company was spun off to become a standalone player dedicated to enhancing the well-being of women across their lifespans.

In this case, I’m paraphrasing the company’s 10-K a bit.

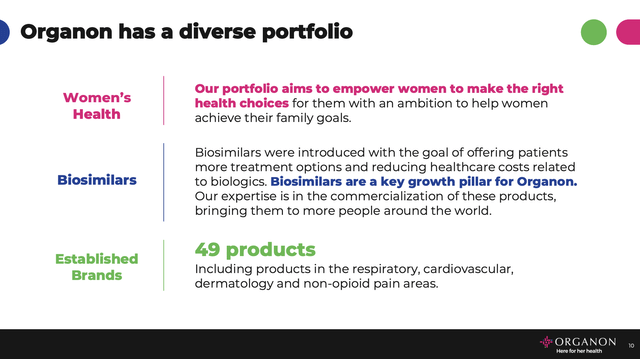

The company says that its mission revolves around creating innovative health solutions within Women’s Health, Biosimilars, and Established Brands.

With a diverse portfolio comprising over 60 products, Organon operates through various distribution channels, including wholesalers, hospitals, government agencies, and healthcare providers.

The company has six manufacturing facilities across different countries.

Organon & Co

- Organon’s Women’s Health division focuses on prescription products in contraception and fertility. Notable products include Nexplanon and NuvaRing for contraception, as well as Follistim AQ and Elonva for fertility. The company’s goal is to lead the women’s health sector by addressing unmet needs from adolescence to menopause.

- Organon’s Biosimilars business covers immunology and oncology treatments, with plans for expansion into areas like ophthalmology, diabetes, and neuroscience.

- Organon’s Established Brands include cardiovascular, respiratory, dermatology, and non-opioid pain management products. While some of these brands have faced generic competition for years, they continue to contribute significantly to the company’s profitability. Organon aims to revitalize these brands through strategic marketing to support future growth in key areas and regions.

In 2022, Organon recorded revenues of $6.2 billion, with approximately 77% generated outside the United States.

This is what the breakdown per segment looks like:

- Women’s Health: $1.7 billion

- Biosimilars: $481 million

- Established Brands: $3.9 billion

A big share of its sales are overseas.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

|

Europe and Canada |

1,741 | 27.6 % | 1,631 | 26.4 % |

|

United States |

1,383 | 21.9 % | 1,437 | 23.3 % |

|

Asia Pacific and Japan |

1,173 | 18.6 % | 1,143 | 18.5 % |

|

China |

933 | 14.8 % | 917 | 14.9 % |

|

Latin America, the Middle East, Russia, and Africa |

841 | 13.3 % | 895 | 14.5 % |

|

Global |

233 | 3.7 % | 151 | 2.4 % |

This brings me to its performance.

How Is OGN Doing?

The company isn’t doing poorly.

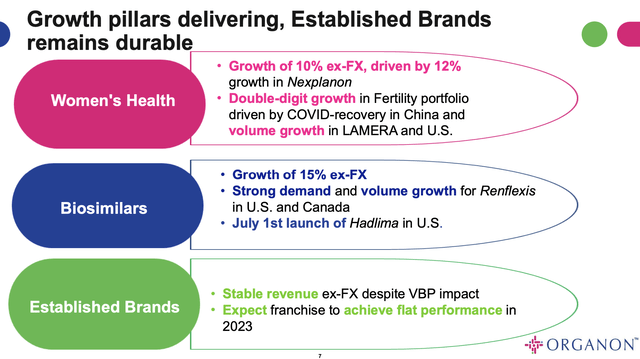

In the second quarter of 2023, the company reported total revenue of $1.6 billion, which marks a 4% increase at constant currency rates compared to the prior-year quarter.

The Women’s Health and Biosimilars franchises saw significant growth, while the Established Brands franchise remained stable. The adjusted EBITDA for the quarter was $530 million, with a 33% margin.

Organon & Co

Growth in the second quarter was influenced by several key factors, including the impact of the loss of exclusivity (LOE), the effects of value-based pricing (“VBP”) in China, price erosion, and strong volume increases.

Additionally, foreign exchange translation played a role in the company’s financial performance.

- OGN noted that the LOE impact was minimal, primarily related to generic competition for NuvaRing in the U.S.

- VBP in China had a $25 million impact in the quarter and a year-to-date impact of $50 million, aligning with expectations.

- Price erosion amounted to approximately $30 million, driven by biosimilars and competitive pricing in the U.S. fertility market.

Volume growth was strong, with about $115 million in the second quarter, largely attributed to growth pillars such as biosimilars, Nexplanon, fertility, Jada, and China Retail.

However, the supply-other segment represented lower-margin contract manufacturing agreements that have been declining since the spin-off.

Also, foreign exchange translation presented a headwind, with a 250 basis point impact in the second quarter, expected to continue moderating throughout 2023.

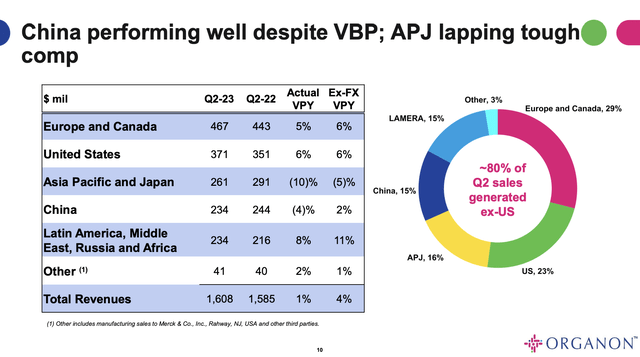

With regard to regional performances, the U.K. region experienced a 6% growth, driven by Atozet and biosimilars in Canada.

In contrast, the Asia Pacific Japan region declined by 5% in constant currency, primarily due to strong performance by competitors the previous year.

Organon & Co

China, despite VBP, managed 2% growth, attributed to COVID recovery in fertility and modest retail growth.

The LAMIRA region saw an 11% constant currency growth driven by Women’s Health and Established Brands.

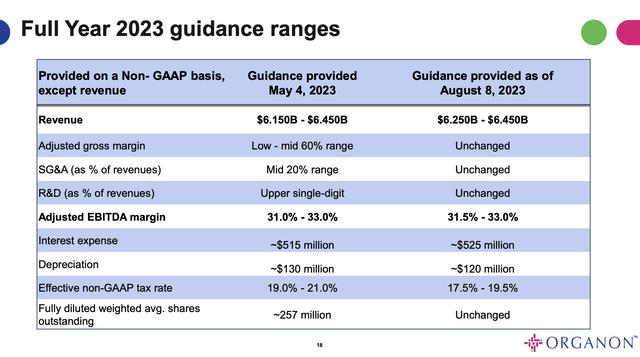

While the company did have some struggles in certain areas, it (positively) narrowed its full-year guidance.

The range for full-year 2023 revenue was changed from $6.15 to $6.45 billion to $6.25 to $6.45 billion.

Factors impacting this guidance included the aforementioned LOE, VBP, potential price erosion, and volume growth.

Organon & Co

So, what about the dividend?

The OGN Dividend & Balance Sheet

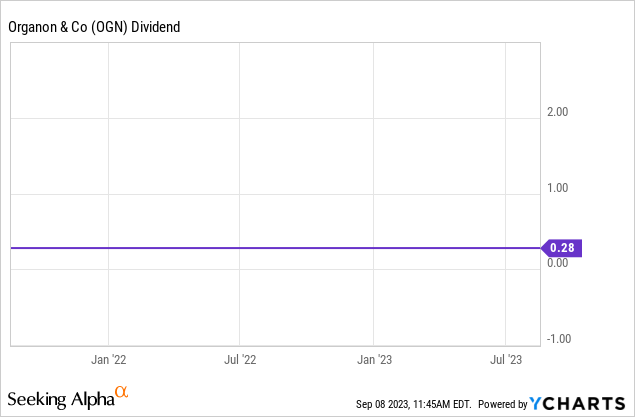

OGN currently pays $0.28 per share per quarter. This translates to a yield of 5.8%.

The company has not hiked its dividend since the spin-off, which explains why its dividend history is a straight horizontal line.

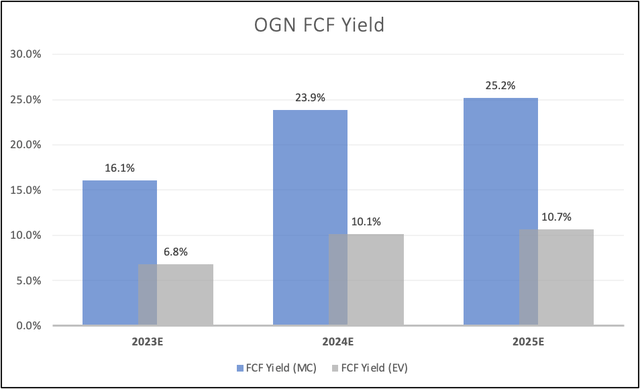

The dividend is protected by a boatload of free cash flow.

As seen in the table in the valuation part of this article, free cash flow is expected to increase to $1.3 billion in 2025, which would result in a 25% free cash flow yield. This may be the highest implied free cash low yield I’ve seen this year. It’s based on consensus analyst expectations.

The only issue is that the company has a lot of debt, which is why the FCF yield drops by 15 points when using the enterprise value instead of the market cap.

Leo Nelissen (Based on analyst expectations)

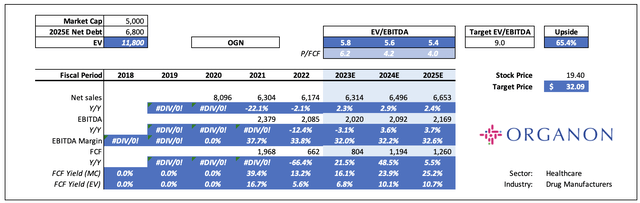

The company is expected to end this year with $7.6 billion in net debt, followed by a decline to $6.8 billion in 2024.

This is more than its $5 billion market cap.

However, because of its EBITDA, the company maintains a sub-4x leverage ratio, which is sustainable. Also, because of its high free cash flow, dividend cuts are not likely.

It has a BB credit rating, which is non-investment grade speculative debt. Also known as junk. However, this does not mean that a default is likely. It means rating agencies need to see improvements before the company becomes investment-grade, which starts at BBB-.

The good news is that as net debt is slowly being reduced, the company does have tremendous potential to hike its dividend aggressively in the future.

Valuation

OGN is very cheap. The stock is trading at just 5.8x 2023E EBITDA. It is trading at 6.2x free cash flow. In 2025, these numbers are expected to drop to 5.4x and 4.0x, respectively.

Leo Nelissen (Based on analyst expectations)

On the one hand, this is partially justified, as the company is not expected to grow its sales at a rate of more than 3% per year.

Annual EBITDA growth is not expected to cross 4%.

It also doesn’t help that debt is somewhat elevated in this environment of sticky inflation and high rates.

On top of that, Apple’s (AAPL) increasing issues with China cause investors to believe that we could be in for more geopolitical turmoil, pressuring companies with exposure in China. OGN has roughly 15% China exposure.

On the other hand, the company is growing consistently. Free cash flow will likely remain strong, allowing for steady debt reduction.

Eventually, the company is in a good spot to hike its already elevated dividend.

At some point, I believe that a 9x EBITDA multiple is warranted, which gives the company a fair value of roughly $32. That’s 65% above the current price.

The current consensus price target is $31.

I will give the stock a Buy rating. I won’t go with a Strong Buy rating despite the high fair value estimate. Due to the elevated debt load, patent risk, and slowly increasing geopolitical risks, I believe this stock should be handled with caution.

While it can turn into a total return monster in the next few years, I wouldn’t go overweight.

Takeaway

Organon may not be the flashiest stock on the market, but it offers a compelling opportunity for income-oriented investors. Despite its lackluster stock performance and substantial debt load, OGN boasts a solid 5.8% dividend yield, supported by a robust free cash flow projection.

With a diverse portfolio covering Women’s Health, Biosimilars, and Established Brands, OGN has a stable revenue base, even though rapid growth may not be on the horizon.

The company’s recent financials show resilience and an optimistic outlook, with potential for future dividend hikes as debt decreases.

Trading at low multiples and a fair value estimate well above its current price, OGN presents an attractive buying opportunity.

However, it’s essential to approach this stock with caution, considering its elevated debt and geopolitical risks.

Read the full article here