Bridgford Foods Corporation (NASDAQ:BRID) has recently seen a pullback in shares over the past year due to stagnant guidance. I believe that Bridgford is a buy due to the firm’s solid balance sheet amid macro headwinds, distribution expansion resulting in greater long-term FCF, and undervaluation assuming my DCF figures.

Business Overview

Bridgford Foods Corporation, along with its affiliated companies, is engaged in the production, promotion, and distribution of frozen, refrigerated, and snack food items within the United States. The company’s two main divisions are snack food products and frozen food products. Biscuits, various bread and roll dough goods, dry sausage, and beef jerky products make up the majority of its product line. The company offers both retail clients and the food service industry a wide variety of about 130 frozen food items. Distributors, cooperatives, and wholesalers all distribute these goods. Additionally, Bridgford Foods provides about 160 snack food products, which are distributed to supermarkets, mass merchandisers, convenience stores, and other similar businesses through customer-owned distribution centers and a direct store delivery network.

Financials

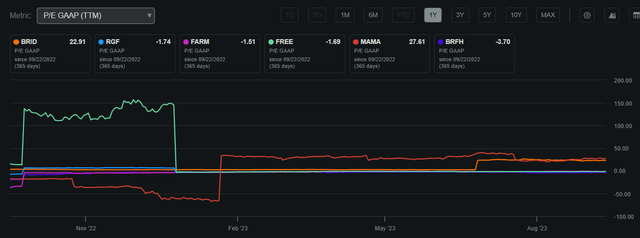

Bridgford is currently valued at around $101.3 million in the market, with a Return on Invested Capital of 3%. The stock is presently priced at $11.16 per share, slightly below its 200-day moving average of $12.26. It’s noteworthy that the company’s P/E GAAP ratio is at 22.91. This figure is lower than comparable peers indicating a relative undervaluation for the firm.

Bridgford P/E GAAP Compared to Peers (Seeking Alpha)

Although Bridgford does not pay a dividend, the firm has decreased its debt significantly and is committed to investments in its core business to return greater shareholder value in the future. The firm has also maintained its outstanding shares, which demonstrates its commitment to preserving value as well.

Annual Shares Outstanding (TradingView) Share Performance (Seeking Alpha)

Earnings

Bridgford recently reported disappointing earnings in Q3 2023 with net income falling from $41.3 million to $684,000 and sales falling from $59.52 million to $54.2 million. This demonstrates that Bridgford is experiencing difficulty during these macro headwinds to have steady cash flows. But, although earnings were weak, the firm’s ability to leverage through its solid balance sheet as mentioned later in this article along with its distribution expansion will allow the firm to leverage while also stabilizing cash flows in the long term.

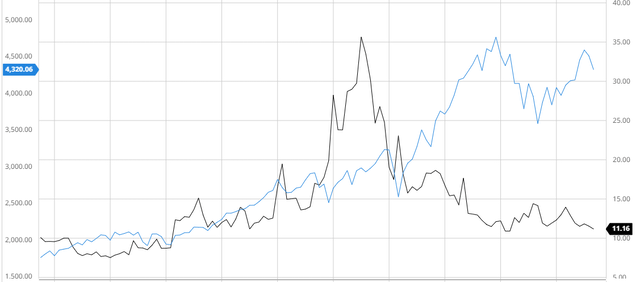

Performance Compared to the Broader Market

Over the past 10 years, Bridgford has underperformed in the S&P 500 due to a recent decline in earnings and revenues. I believe that the firm must restructure its strategy to stimulate growth and recover from recent negative price action in the long run.

Bridgford Compared to the S&P 500 10Y (Created by author using Bar Charts)

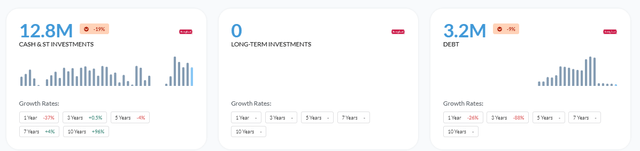

Balance Sheet

Bridgford also maintains a robust financial position with a substantial reduction in debt and enhanced interest coverage at 7.83. This resilient, low-debt balance sheet provides the company with flexibility for potential leveraging, particularly during periods of challenging macroeconomic conditions that may strain cash flows. Demonstrating a Current Ratio of 3.46 and an Altman-Z-Score of 4.14, Bridgford’s ongoing operations are stable and promising for the near to medium term.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

Valuation

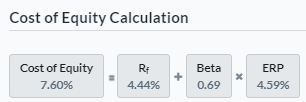

In order to calculate an accurate fair value for Bridgford, I first had to find the firm’s Cost of Equity by using the risk-free rate from the 10-year treasury yield. Based on this rate, I was able to find a Cost of Equity of 7.6%.

Cost of Equity (Created by author using Alpha Spread)

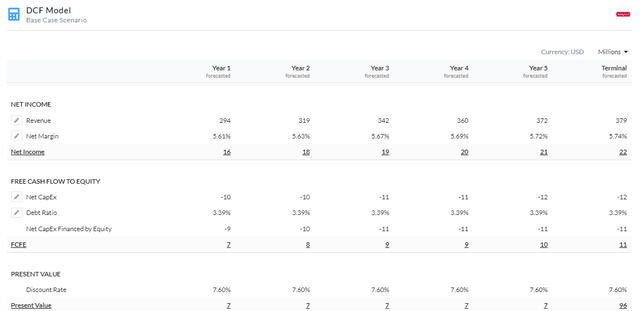

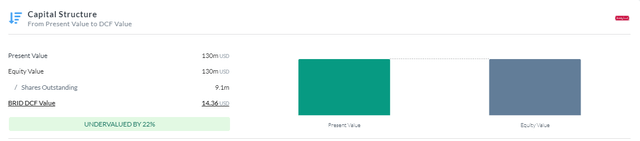

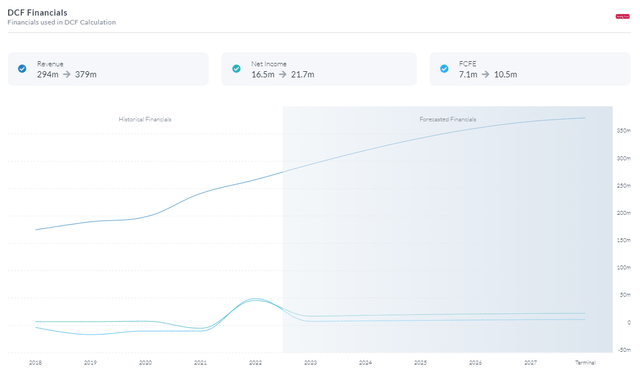

Assuming the previously calculated Cost of Equity, I created a 5-year Equity Model DCF using FCFE. I decided to use the discount rate of 7.6% because the firm is adequately leveraged for macroeconomic headwinds and will be able to take on debt if cash flows become a concern. I also estimated revenues and margins to grow with company guidance estimates as shown below. This resulted in a fair value of $14.36 presenting a potential upside of 22%.

5-Year Equity Model DCF Using FCFE (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

Distribution Network Expansion Resulting in Compounding Growth

As a key component of its corporate strategy, Bridgford Foods is dedicated to expanding its distribution network. By maximizing how its items are delivered to retail locations and end users, the corporation hopes to ensure that consumers can easily access its products.

Their efforts to form strategic alliances with significant retail chains and distributors served as one illustration of how they were enhancing their distribution network. Bridgford Foods was able to increase the visibility of its products in stores and get greater shelf space by working with influential players in the retail sector. This strategy improved both the accessibility of their products and brand recognition.

Bridgford Foods has looked into expanding its distribution options by adopting e-commerce. The business attempted to increase its presence in numerous online marketplaces after realizing the growing trend of online shopping. By making this change, they were able to reach customers who valued the ease of acquiring their goods online, thereby expanding their customer base.

Through such strategies, Bridgford Foods Corporation aimed to make its products more easily accessible to a wider audience, ensuring that consumers could find their offerings in their preferred retail outlets or through online platforms. This will not only improve sales but also expand margins due to the underlying costs being cut on an e-commerce platform along with greater wholesale pricing power once store items become more popular in large chain stores. This will result in improved cash flows along with greater FCF leading to the further expansion of its core business to outpace competitors.

Risks

Operational Risks: Natural disasters, supply-chain disruptions, labor issues, and any other operational challenges that affect production and distribution.

Market Volatility and Fluctuating Commodity Prices: Price fluctuations for ingredients like wheat, beef, and other raw commodities as a result of market dynamics, climatic circumstances, or geopolitical events, which have an impact on manufacturing costs and total profitability.

Regulatory and Compliance Risks: Regulations governing food safety and quality must be followed; failure to do so could lead to product recalls, legal action, reputational harm, and monetary losses.

Conclusion

To summarize, I believe Bridgford is a buy due to the firm’s solid balance sheet amid macro headwinds, distribution expansion resulting in greater long-term FCF, and undervaluation assuming my DCF figures.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here