Co-authored by Treading Softly.

The current generation of workers presents an interesting conundrum for employers. This generation is among the least likely to move for work – they would rather make a worse career choice to remain close to family and friends than be forced to move. This flies strongly in the face of previous generations, which saw the majority move to new cities or towns for work.

This generation is also considered to be among the least “loyal” to their employer, with the average timeframe working for the same company falling into three years. They feel that annual raises are not properly valuing their contributions, and changing jobs often provide double-digit compensation increases. While we could discuss and opine on how employers could do more to reward long-term employees, we can accept that long gone are the days you’d get a job and work there for your entire lifetime.

People love to keep their options open and enjoy being able to be flexible or transient in many aspects of their lives. So it should come as little surprise that in the market, average holding periods for investments have dropped from decades to mere months or weeks.

So, deciding to be an income investor and eventually a professional income investor can feel binding or restricting. How can you be an income investor and potentially swear off vast non-income-providing swaths of the market?

As a professional income investor, there are certain types of companies that naturally fit my goals better than others. You’re going to find a lot of real estate investment trusts (“REITs”), business development companies (“BDCs”), and fixed-income investments that have high dividends, but when you get into a lot of sectors, you’re lucky if they pay a 3% yield.

As a result, my portfolio does not have a particularly strong correlation to the S&P 500 (SP500). There are days when the S&P is down and my portfolio is up, and there are days when my portfolio is down while the S&P goes up. I want the diversification that many non-dividend paying companies provide, but I am not going to buy stock in a company that is unable or unwilling to pay me.

Fortunately, there is a solution: Closed-End Funds. CEFs manage portfolios and are required to pay out the majority of their income and capital gains to shareholders. As a result, CEFs tend to have the high yields I demand, while the holdings within the portfolio can be anything under the sun.

Today, I want to look at two top-notch CEFs that I can use to leverage outstanding and generous income from the market.

Let’s dive in!

Pick #1: USA – Yield 10.8%

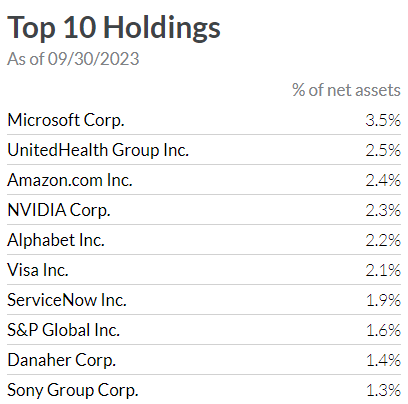

Liberty All-Star Equity Fund (USA) is a CEF that has five distinct managers. Three of them use “Value” oriented investment strategies and the other two use “Growth” oriented investment strategies. This creates diversification among holdings and investment strategies. The fund primarily invests in “large caps,” an area where you aren’t likely to find many high yields. As a result, the top 10 holdings of USA have zero overlap with my picks. Source.

Liberty All-Star

We all recognize the names. Great, well-established companies that have had significant returns for shareholders for years. Yet not one of these companies pays a dividend worth getting out of bed for.

USA converts this portfolio into a variable income stream. Its policy is to pay out 2.5% of NAV each quarter. As a result, when NAV is high and there are a lot of capital gains to realize, the dividend is higher. When the market is down and there aren’t so many capital gains, the dividend is lower. This helps ensure that the fund is neither underpaying nor overpaying shareholders.

USA is a great option for income investors to diversify and gain exposure to many of the big names that aren’t going to fit into a dividend strategy. We can get exposure to the broader market while also enjoying a high income. Diversification + Income = Happiness.

Pick #2: RNP – Yield 10.3%

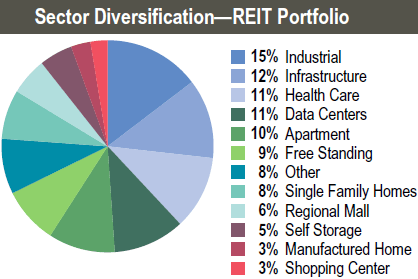

Cohen & Steers REIT & Preferred Income Fund (RNP) is a CEF that has two distinct strategies, both designed to provide a high level of income. First, RNP has a diversified REIT portfolio: Source.

RNP Fact Sheet

While “industrial” is its largest sector, it is closely followed by infrastructure, health care, data centers, and apartments. RNP’s picks in these sectors are what most who follow REITs would classify as “best in class” or at least contenders to be in the best-in-class conversation. Their top 10 include names like Prologis (PLD), American Tower (AMT), Welltower (WELL), and Realty Income (O), among others.

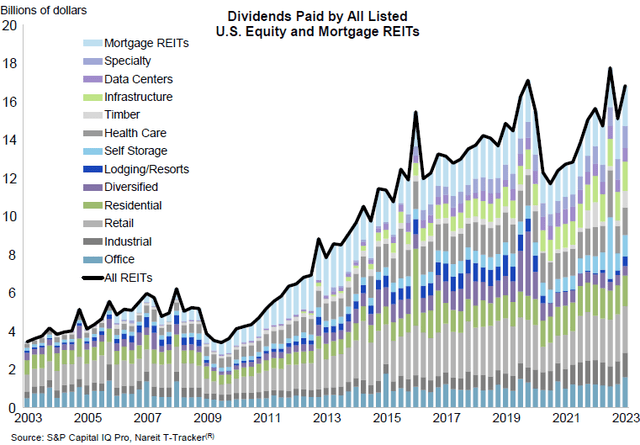

The REIT sector is an interest rate-sensitive sector, frequently selling off when interest rates rise. Yet, it is also a sector that has seen dividend growth over time. Like the Great Financial Crisis, COVID had a negative impact on REIT dividends. However, as a group, REIT dividends have recovered to pre-COVID levels and are continuing to climb. Source.

REITWatch Sept report

It is a sector that has proven its ability to provide high cash flow and to recover when those cash flows are disrupted by black swans.

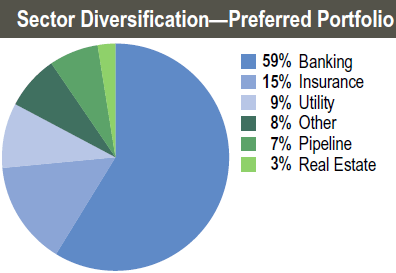

The other half of RNP’s portfolio is invested in preferred equity. While many REITs have preferred shares, RNP chooses to focus on other sectors for the preferred portfolio to maximize its diversification. Real Estate only makes up 3% of its preferred portfolio.

RNP Fact Sheet

Instead, RNP focuses on banking and insurance, two sectors that frequently utilize preferred equity. Preferred equity provides a stable and predictable income while being less volatile than common equities.

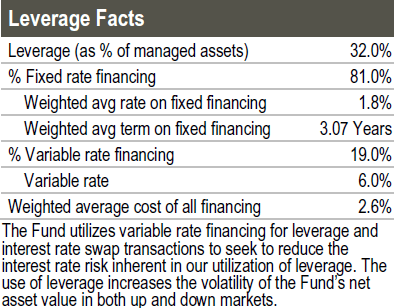

Both of these sectors are likely to see a strong recovery as interest rates stop rising and would benefit if interest rates started declining. Both of which are a question of “when,” not “if.” While RNP waits, they were quick enough to load up on interest rate swaps, effectively fixing 81% of their debt at a 1.8% interest rate.

RNP Fact Sheet

This provides RNP with ample time to wait, without having to be overly worried about the rising costs of financing for their borrowings. We are happy to buy up RNP while it is trading at an 8% discount to book value, building our income and looking forward to price upside when interest rates stop rising.

Conclusion

With USA and RNP, we can enjoy outstanding income from a vast array of holdings that otherwise may not be worth holding in an income portfolio. These portfolio managers leverage their experience and skills to provide you and me with outstanding and recurring income.

I see CEFs as a tool to help rapidly boost my portfolio’s income-generative ability. Any tool has its purpose and time to shine; often, the best times to buy a tool are not when it’s attractive to everyone – thus, demand is low and the price is likewise lower. You don’t want to have the need to buy a hammer when you’re looking to drive a nail; you want to have the hammer already.

When it comes to your retirement, your portfolio is your toolbox. It needs to be filled with tools to complete different tasks and provide you with a means to solve life’s problems head-on. Your expenses are going to be relentless and unending. You need a solution that is equally relentless and unending – I have that solution in my portfolio by following my unique Income Method and generating an abundance of income that overwhelms my expenses and provides excess income to spend as I please and enjoy the luxuries of life.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here