Consumer electronics maker Garmin (NYSE:GRMN) delivered a decent 1H 2023 despite tough comps and macro challenges. Auto OEM segment is a meaningful medium term growth driver on the back of an expanding intelligent vehicles market. Prospects appear baked into the stock.

Company Overview

Gamin designs, develops and manufactures wearable, portable, and fixed-mount Global Positioning System [GPS]-enabled products and other navigation and communication products for five primary markets: fitness, outdoor, aviation, marine, and auto.

Fitness: this segment offers products designed for use in health, wellness, and fitness activities. Products offered include sports watches, cycling products such as cameras and bike radars, activity tracking fitness bands, fitness and cycling accessories such as blood pressure monitors and cycling bike speed sensors, along with online web and app platforms that enable users to track their fitness, activities, and wellness data. This is Garmin’s second-biggest segment accounting for roughly a quarter of revenues.

Outdoor: this segment offers products for outdoor activities. Products offered include adventure watches, golf devices, dog tracking and training devices, and outdoor handheld devices with features ranging from basic navigation capabilities to more sophisticated features offering barometric altimeters and 3-axis compass. This is Garmin’s biggest business segment accounting for roughly a third of revenues. It is also Garmin’s most profitable business segment in terms of margins (with segment operating margins of over 30%) as well as earnings contribution (accounting for nearly half of total operating income).

Garmin Q2 2023 earnings release

Aviation: this segment offers a range of aircraft avionics solutions which are sold directly into aircraft original equipment manufacturer (OEM) applications as well as through Garmin’s worldwide dealer network for retrofit installations on existing aircraft. Products offered include integrated flight decks, flight displays, automatic flight control systems, audio control systems, engine indication systems, traffic awareness and avoidance solutions, transponder solutions, weather solutions, and wearables such as smartwatches for pilots. This segment also offers web and mobile app-based products to help pilots plan, file, and log flights. Business and commercial aviation customers are also offered other benefits such as runway analysis, load planning and other performance data.

Marine: this segment offers recreational marine electronics Products offered include chartplotters marine autopilot systems, marine radars, marine VHF communication radios, and wearables such as smartwatches for mariners.

Auto: this segment designs and develops products for the auto market. Products for consumer auto markets include personal navigation devices and dash cams, while products for OEM auto customers include infotainment units, integrated cameras, in-cabin monitoring and gaming solutions. This is Garmin’s smallest segment accounting for less than 10% of revenues.

Garmin Q2 2023 earnings release

1H2 2023: growth picks up, margins decline

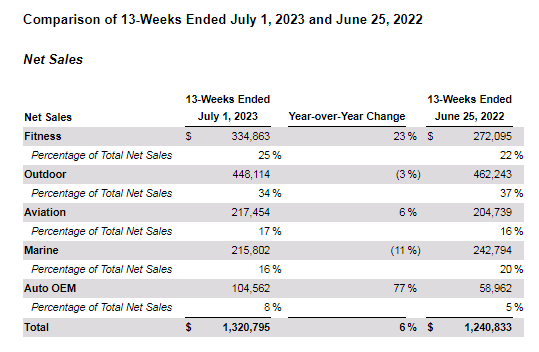

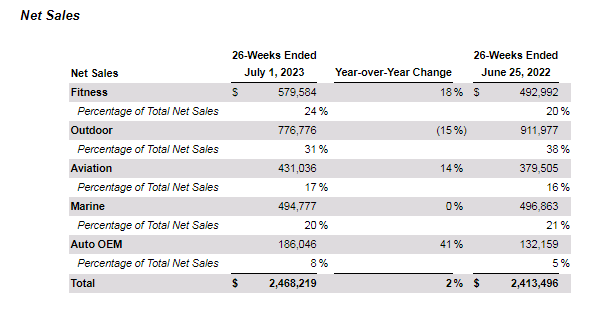

Q2 2023 sales rose 6%, the first quarter of positive growth after four quarters of consecutive declines (which were partly due to tough comps). For 1H 2023, revenues inched up 2.2% YoY to $2.46 billion. Fitness, Aviation and Auto OEM saw positive growth while Marine was flat (partly due to normalizing demand post-pandemic as well as sluggish market conditions due to economic uncertainties) and Outdoor declined (due to tough comps).

Garmin Q2 2023 earnings release

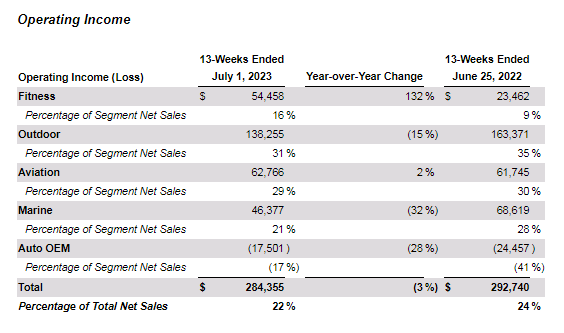

Margins however remained soft due to segment mix (bigger revenue contribution from Auto OEM and Fitness which carry lower margins than Outdoor which saw its revenue share drop) which offset tailwinds from moderating input costs; 1H2023 gross margins dropped to 57% from 58% the same period last year and operating margins were down to 20% from 22% the same period last year.

For FY2023, management expects revenues of around $5.05 billion. This translates into a growth rate of roughly 4% from last year’s $4.86 billion revenues. Gross margins are expected at 57.2% (compared with 57.7% last year), and operating margins are expected at 20% compared with 22% last year.

Near term tailwinds include moderating inflation (which could ease margin pressure) and possible rate cuts (which could provide a lift to overall consumer spend and therefore sales, particularly in their Marine business segment). Goldman Sachs expects possible rate cut in Q2 2024.

Strategic focus on increasing recurring revenue sources potentially promising, Auto OEM segment a meaningful medium-term growth driver

All of Garmin’s end markets could benefit from secular growth trends helped by a robust smartwatch market which is projected to grow in the high single digits over the coming years according to research reports. Smartwatches contribute to sales in all of Garmin’s segments except Auto OEM. Garmin does not break down smartwatch sales however their estimated 4% market share in a market estimated at $45 billion suggests their smartwatch business is collectively worth more than $1.5 billion or around a third of their total revenues of $4.8 billion last year.

Management noted in their Q2 2023 earnings call that they are strategically focusing on increasing recurring revenue sources. Results from this strategy remain to be seen, but if successful it could not only reduce revenue and earnings volatility but also increase switching costs. Garmin already has a number of subscription products including aviation databases, insurance plans, marine charts, cycling content library and maps subscriptions to name a few and they continue to launch new subscription products such as their new golf app subscription. Many of these products play well into Garmin’s strengths in GPS technology and serve very specific target markets such as athletes, pilots, and hikers and thereby help solidify their niche, high-end position in the increasingly competitive but fast-growing smartwatch industry.

Garmin’s Auto OEM segment is its smallest, but this segment could be a meaningful growth driver along with the rise of intelligent vehicles. The company has a longstanding history in the automotive devices market particularly as a navigation solutions provider, however their strategy going forward is more ambitious with a focus on unifying multiple automotive domains, touchscreens, and wireless devices on a single SoC (system on chip). Garmin recently introduced their latest in-cabin automotive solution early this year which features four infotainment touchscreens, wireless gaming controllers, a cabin monitoring system, and facial recognition to automatically load user preferences among other features. The company continues to strengthen their automotive offerings through R&D (Garmin’s R&D intensity has increased from 13% of revenues around a decade ago to around 17% the last fiscal year). Garmin has a history of making strategic acquisitions to expand their capabilities and with a robust balance sheet (barely any debt, current ratio of 2.8) the company has ample flexibility to make further acquisitions. Based only on business secured so far (as of early this year), management expects Auto OEM segment revenues to grow at a CAGR of 40% over the next few years.

Margins may come under pressure as Auto OEM segment ramps up

Garmin’s Auto OEM segment is currently its only loss making segment (11% segment loss in FY2022). While the company is aiming to have the segment turn profitable by 2024, it is not clear how profitable the segment would be. In any case, it may remain a drag on overall margins in the foreseeable future as the segment’s revenue share rises against more profitable segments like Outdoor (37% segment operating margin) and Aviation and Marine (over 20% segment operating margin).

Risks

Competitive risks

Garmin’s roughly 4% smartwatch market share dwarfs market leader Apple who commands a 30% market share by shipments and 60% share of revenues. Garmin is currently recognized as being ahead of Apple in some areas such as GPS accuracy and data analytics however Apple has been consistently improving over the years and looks well positioned to continue to do so. Apart from scale economies, Apple enjoys ecosystem advantages over Garmin and financial advantages from their considerably larger smartwatch business suggests Apple is in an increasingly stronger position to invest in smartwatch innovation to narrow any superiority in terms of technology and domain expertise Garmin currently enjoys, and thereby potentially offer a better value proposition to smartwatch customers in terms of price and features in the long run.

Execution risks

Garmin’s has long offered pricey devices with hefty features, subscription-free. Switching costs are currently limited so if their new subscription plans don’t sit well with consumers, the strategy may backfire if customers promptly switch to rivals like Apple.

Conclusion

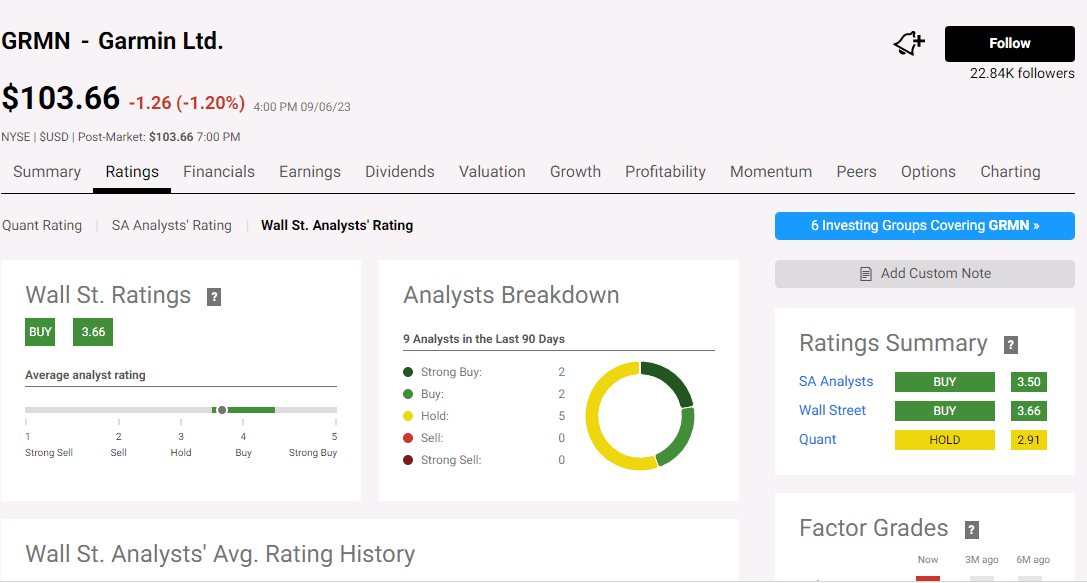

Garmin has a moderate buy analyst consensus rating.

Seeking Alpha

Garmin’s revenues have grown at a CAGR of around 6% over the past decade, and earnings have grown nearly 5%. Looking ahead, Auto OEM and smartwatches could support medium term growth assuming good execution. Margin pressures however could limit earnings cash flow growth as well as profitability metrics and competitive risks may further impact profitability.

Garmin’s stock has appreciated 13% over the past year and is trading at a forward P/E of 20. This is higher than the sector median (14.5) and roughly equal to their 5 year average (21). Prospects appear largely baked into the stock.

Read the full article here