Strategy overview

iShares iBonds 2024 Term High Yield and Income ETF (BATS:IBHD) is a high yield bond fund paying monthly distributions, with an expense ratio of 0.35%. It was launched on 5/7/2019 with the objective of investing in components of the Bloomberg 2024 Term High Yield and Income Index. The fund may also invest in ETFs, U.S. government securities and cash equivalents. It has 338 holdings, mostly corporate bonds below investment grade with a maturity date between 1/1/2024 and 12/15/2024, and an average yield to maturity of 7.78%. The Underlying Index is rebalanced on the last calendar day of each month until 6/30/2024. Then, as the bonds mature, it will transition to cash and cash equivalents. On or about 12/15/2024, the fund will terminate operations and be redeemed to shareholders, as its value will be almost entirely in cash.

Portfolio

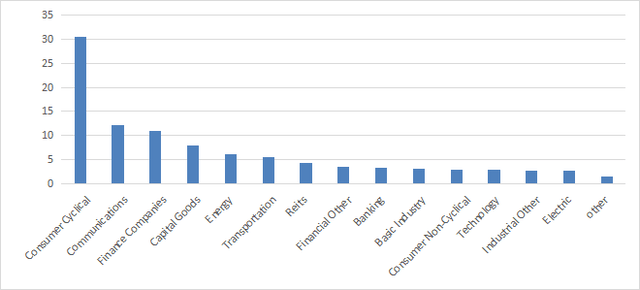

As reported on the next chart, the fund is overweight in issuers from the consumer cyclical sector (“consumer discretionary” in GICS denomination), with 30.4% of assets. Industrials are in second position: the sum of capital goods, transportation, basic industry (which may also include companies in the materials sector) and other industries is 19.2%. Communication services and financials are in a 11%-12% range. Other sectors are below 7%.

IBHD industry breakdown in % of assets (Chart: author; data: iShares)

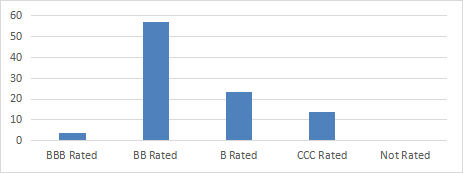

About 95% of the fund’s asset value is in bonds rated BB and below. IBHD is clearly positioned in the “junk bond” ETF category.

IBHD ratings in % of assets (Chart: author; data: iShares)

The next table lists the top 10 issuers, representing an aggregate weight of 29.8%. The heaviest ones weigh about 3%. As a consequence, the portfolio is well-diversified across a number of companies and the risk related to each of them is moderate.

|

Name |

Weight% |

|

FORD MOTOR CREDIT COMPANY LLC |

3.07 |

|

SERVICE PROPERTIES TRUST |

3.01 |

|

ICAHN ENTERPRISES LP |

3.01 |

|

LAS VEGAS SANDS CORP |

3.01 |

|

DELTA AIR LINES INC |

3 |

|

NAVIENT CORP |

2.98 |

|

INTESA SANPAOLO SPA |

2.98 |

|

TELECOM ITALIA SPA |

2.97 |

|

DISH DBS CORP |

2.92 |

|

GLOBAL AIRCRAFT LEASING CO LTD |

2.87 |

Who should hold IBHD?

This fund is clearly not a long term pick: it will be converted to cash next year. Moreover, it makes little sense to invest in a junk bond fund with a yield to maturity of 7.8%, when a much safer T-bill ETF like iShares 0-3 Month Treasury Bond ETF (SGOV) is at 5.4%, with a net expense ratio of only 0.07% and a very low volatility.

In fact, IBHD is not a standalone product. It is designed as a component for bond ladder strategies, along with its siblings with different years of maturity: IBHC (2023), IBHE (2025), IBHF (2026), IBHG (2027), IBHH (2028), IBHI (2029) IBHJ (2030). The fund issuer also has bond ladder ETFs in investment grade corporate bonds (IBDO to IBDY), municipal bonds (IBML to IBMR) and treasuries (IBTD to IBTO). You can see them all here, with their characteristics and a ladder designer tool to combine them.

A bond ladder strategy allots a capital to several “rungs”, usually in equal weight and corresponding to equidistant maturity intervals. When the closest rung is converted to cash, the proceeds may be reinvested in a farther rung, or elsewhere. Rungs may vary from quite short term (for professional bond portfolio managers) to several years. iShares iBonds series allows investors to create rungs with intervals of one year or more. In a bond ladder strategy, these ETFs are designed to be held until maturity. Doing so, investors don’t have to worry about price variations due to interest rates and market sentiment. However, keep in mind they hold junk bonds, so defaults may affect the NAV (net asset value).

A bond ladder strategy allows to:

- Manage cash flow based on planned distributions,

- Smooth out the effect of fluctuations in interest rates,

- Lock in higher yields when it is possible,

- Have periodically some cash available to reinvest or spend.

ETFs like IBHD make bond ladder strategies simple for everyone. It doesn’t mean they are for everyone, even less those in the high yield category. First, bonds usually represent only a part of an investor’s asset allocation. Second, to be worth the work, bond ladders need to be divided in several positions with at least a few thousand dollars in each. Third, a ladder in high yield bonds makes sense only after creating at least another ladder in safer bonds (treasuries, munis, corporate). ETFs of the IBHx series have their place in the strategy of a high-net-worth individual or a family office, not of an average investor.

Performance

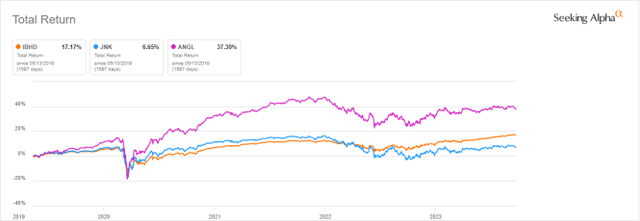

The next chart compares total return since inception of IBHD and two high-yield ETFs holding bonds of various maturity years:

- SPDR Bloomberg High Yield Bond ETF (JNK), a benchmark for this asset category;

- VanEck Fallen Angel High Yield Bond ETF (ANGL), picking bonds of issuers that have lost their investment grade rating.

IBHD is ahead of the benchmark, but significantly behind the fallen angel fund.

IBHD since inception vs. JNK, ANGL (SeekingAlpha)

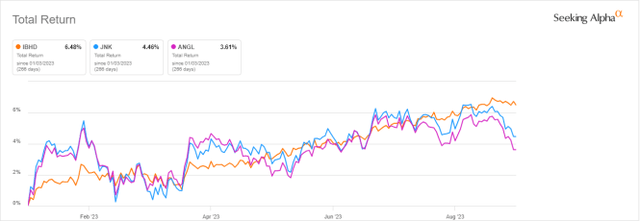

However, IBHD has been the best performer and the less volatile in 2023 to date (next chart). This is not a surprise: it will start converting to cash in about 9 months, and there is less uncertainty on NAV than for funds holding bonds of all maturity years.

IBHD vs. JNK, ANGL year-to-date (SeekingAlpha)

Takeaway

iShares iBonds 2024 Term High Yield and Income ETF has an attractive 7.8% yield, but it is not a long-term investment. It is an element of a bond ladder ETF series and will be converted to cash in December 2024. Bond ladder ETFs are designed to be held until redemption to limit risks of price gyration. However, IBHD low volatility in the recent months shows that the risk is already much lower than for broader junk bond ETFs. Bond ladders in high-yield bonds are more likely to interest high-net-worth individuals and family offices, not average investors. Keep also in mind these ETFs may be overweight in a sector: consumer discretionary in this case.

Read the full article here