Introduction

Investment grade corporate bond funds tend to be a better choice than high-yield bond funds in times of market turmoil. However, last year was a brutal year for both types of funds as the Federal Reserve aggressively hiked the rate. Will this trend continue towards the end of 2023 and into 2024? In this article, we will analyze iShares 5-10 Year Investment Grade Corporate Bond ETF (NASDAQ:IGIB) and provide our insights and recommendations.

Investment Thesis

IGIB invests in investment grade corporate bonds in the United States. The fund offers an attractive yield of 5.93% and has a quality bond portfolio with low default rates. However, an economic recession that may likely happen in early 2024 may trigger a selloff. Long-term income investors should treat this event as a good buying opportunity to accumulate more shares as the event will likely be temporary. Over the long run, we expect both capital appreciation and solid interest incomes.

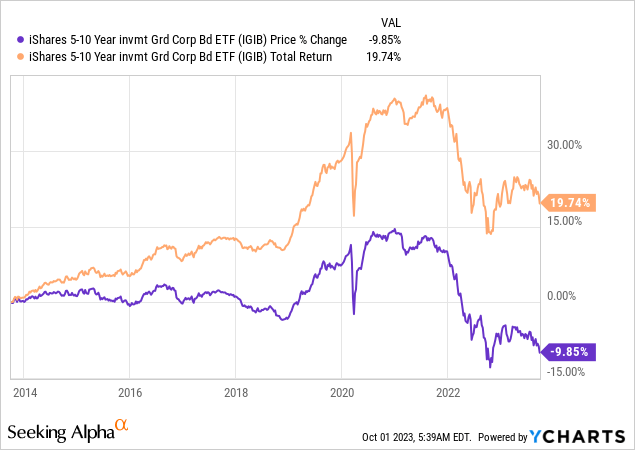

YCharts

Fund Analysis

IGIB has performed poorly since 2021

IGIB reached its historical peak during the pandemic thanks to the Federal Reserve’s quantitative easing monetary policy. However, skyrocketing inflation started in late 2021 has caused the Federal Reserve to quickly reverse its monetary policy from easing to tightening.

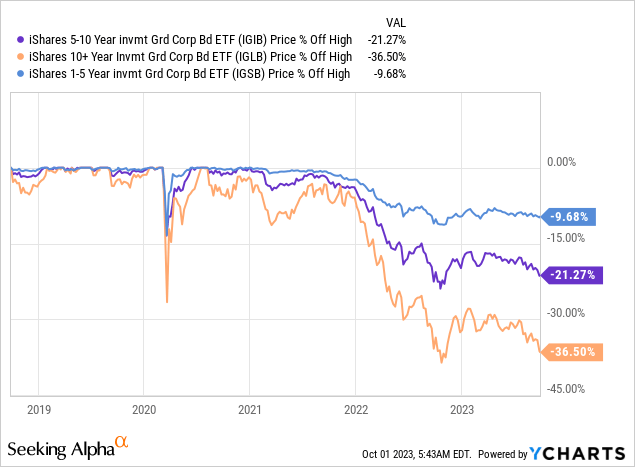

As a result, IGIB has declined by over 21% since its price peak reached in 2021. Its loss of 21.3% was not the worst, though. Its peer fund such as iShares 10+ Year Investment Grade Corporate Bond ETF (IGLB) suffered a much greater loss of 36.5%. The reason for this greater loss of IGLB is due to the longer duration of the bonds in its portfolio. In general, the longer the duration of the bond, the more sensitive its price is to the change of rate and vice versa. In contrast, shorter-term bond funds such as iShares 1-5 Year Investment Grade Corporate Bond ETF (IGSB) have only dropped by 9.7% due to its portfolio’s shorter duration characteristic.

YCharts

IGIB owns a portfolio of investment-grade corporate bonds

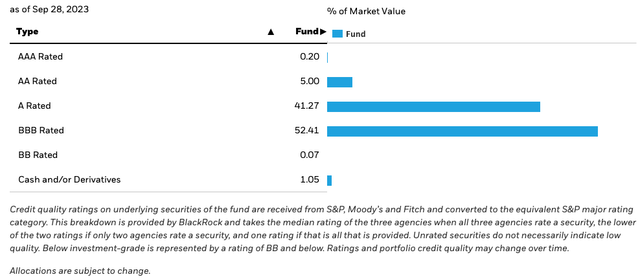

IGIB’s portfolio consists of nearly 100% investment grade corporate bonds. As can be seen from the chart below, BBB rated and A rated bonds represent about 52.4% and 41.3% of the portfolio respectively. These bonds have very low default rates. In fact, the default rate for 3-year and 10-year investment grade corporate bonds are only 0.41% and 1.81% respectively. With a 30-day SEC yield of 5.93%, this yield is way higher than the default rates. Therefore, default risk is quite minimal.

iShares

However, there is downside risk in an economic recession

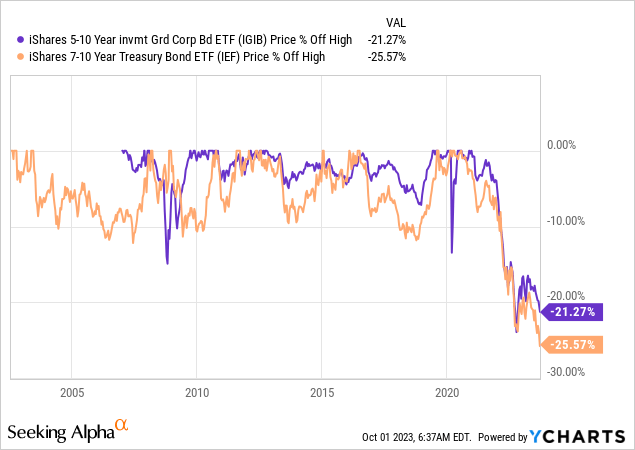

Although, IGIB has a high-quality portfolio of investment grade corporate bonds, its near-term risk cannot be ignored. We believe the Federal Reserve’s policy of keeping the rate elevated or higher, and for longer to combat persistent inflation, may eventually cause the U.S. economy to fall into a recession. The reason that it has yet to happen is because monetary policy typically takes 6~12 months to propagate through the entire economy. Therefore, we may eventually start to feel this impact towards the end of the year or in the first half of 2024. If a recession shows up, investment grade corporate bonds may fall even further as investors seek safe haven in treasuries instead. As can be seen from the chart below, IGIB’s fund price experienced negative spikes amid the initial outbreak of the global pandemic in 2020 and in the Great Recession in 2008/2009. In contrast, its treasury fund peer iShares 7-10 Year Treasury Bond ETF (IEF) did not experience any decline during these two periods. The reason is because investors often perceive U.S. treasuries as risk-free assets and tend to rotate money out of riskier assets such as corporate bonds into treasuries.

YCharts

Another possible explanation that IGIB tends to experience a negative spike in a recession is because over 52% of IGIB’s portfolio is BBB-rated bonds. As we know, BBB-rated bond is the lowest-rating bonds in the investment grade category and is more vulnerable in an economic recession than A, AA, or AAA bonds. In an economic recession, credit rating agencies may downgrade some BBB-rated bonds to non-investment grade bonds. As the market anticipates these downgrades to happen, bond prices may react beforehand and cause a fall in IGIB’s fund price.

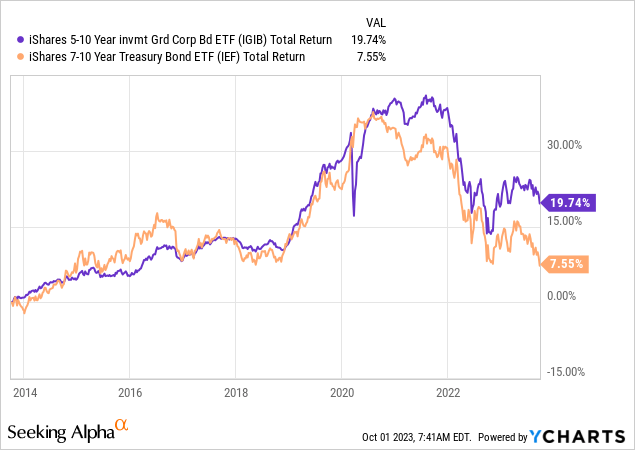

However, investors should treat this negative spike as a good buying opportunity

Despite the fact there tends to be a negative spike for corporate bonds during an economic downturn, long-term investors should embrace this volatility. As investment guru Warren Buffett often says, “Be greedy when others are fearful,” long-term investors should treat this rare negative spike as a good buying opportunity. In fact, IGIB actually outperformed its treasury peer IEF in the long run. As can be seen from the chart below, IGIB’s 10-year total return of 19.7% is obviously much better than the 7.6% return of IEF.

YCharts

Investor Takeaway

While we may be closer to the end of this rate hike cycle than the beginning of this year, a recession may not be too far away too. As we have discussed in our article, there may still be the possibility of a negative spike in IGIB’s fund price. However, investors should not fear and instead should treat this as a good buying opportunity. Since the Federal Reserve will usually turn its monetary policy from tightening to loosening in an economic recession, we see possible capital gains afterward. Therefore, investors will be able to earn both a solid interest income and some capital gains in the long run. Hence, we believe long-term income investors should own this fund.

Additional Disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Read the full article here