In this article on Moncler S.p.A. (OTCPK:MONRF), I provide a brief update on the company. In my previous articles, I had pointed out that despite the impressive growth figures, the company was approaching its price target in a way that made it less attractive. As anticipated in the article, the previous target price was €63.00 (equivalent to $68.20 for MONFR), and after reaching this target, the stock began to decline.

Previous Article Moncler (Seeking Alpha)

The key factor that had a negative impact was the concern about a potential macroeconomic slowdown, which could lead to a decrease in sales for luxury brands, including Moncler.

In this article, I delve into some noteworthy figures related to Moncler and the luxury goods sector. This analysis aims to provide insights into the company’s performance and includes an update to my DCF model based on the latest developments.

Mid-year results were excellent, but a slowdown in spending will need to be considered

The H1FY23 results from the end of July were exceptional, with a revenue of €1,136.6 million, marking a 22% growth compared to 2022. The Net Result was €145.4 million, slightly lower than the €211.3 million in H1FY22, primarily due to an extraordinary tax benefit (€92.3 million). Excluding this exceptional event, the group demonstrated its capability to navigate through supply chain slowdowns and inflationary pressures without significant impact. Furthermore, the company sustained double-digit growth, reaffirming its position as a robust and steadily growing group.

As stated by the CEO of the group, Remo Ruffini:

“For the first time in our history, Group revenues exceeded the 1 billion euro mark in the first half of the year. I am proud of this significant milestone, a testament to the great teamwork, innovative thinking, and customer-centric approach that defines our Group.”

(Source: Moncler Results H1FY23)

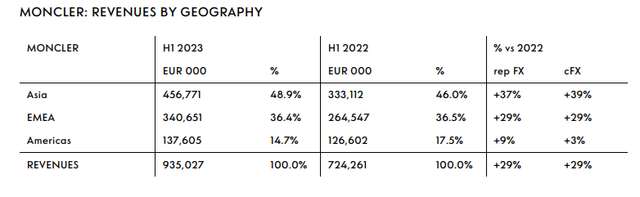

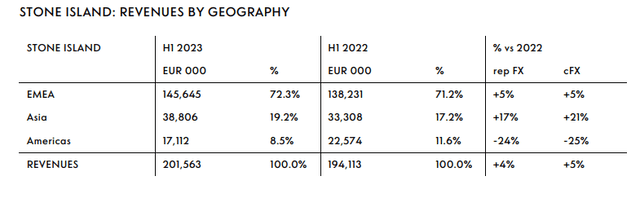

Analyzing the markets and individual brands, I observed several trends which I also highlighted in my previous articles. Notably, the impressive growth in Asia for the Moncler brand stands out. This 39% growth was as I anticipated in my initial article on Moncler, driven by the end of lockdowns in China and a subsequent surge in consumer spending. Similarly, the Stone Island brand also experienced growth, albeit at a slightly lower rate of +21%.

Moncler Brand Growth (Moncler H1FY23)

However, the most significant impact is seen in the Moncler brand’s performance in Asia. While Stone Island primarily sells in EMEA (accounting for 72.3% of Revenue), Asia stands out as the largest market for Moncler, comprising 48.9%, followed by EMEA and the Americas with 36.4% and 14.7% respectively.

Stone Island Brand Growth (Moncler H1FY23)

These figures not only allow for an in-depth analysis of Moncler’s outstanding 2023 results but also enable a more precise assessment of the individual markets it operates in. This insight is crucial for understanding the potential, and indeed probable, impact of an economic slowdown and reduced demand.

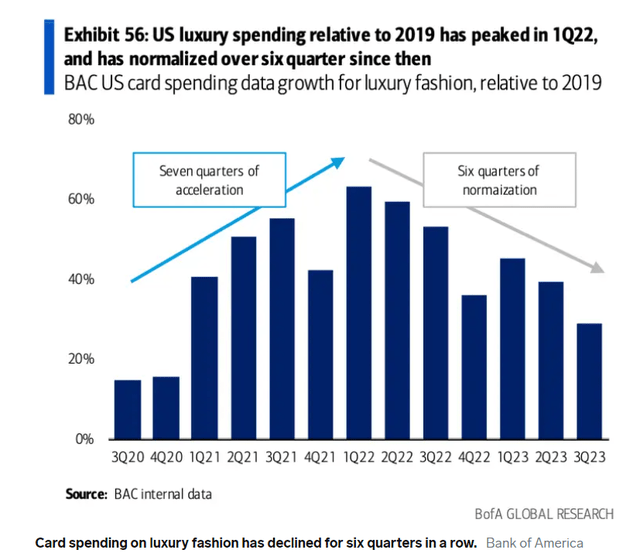

According to analysts, the fashion sector is expected to be affected by the less-than-stellar performance of the US and European economies. Additionally, recent data on Chinese growth does not appear very encouraging.

Nonetheless, from my perspective, while a slowdown in retail sales is foreseeable in the EMEA and Americas regions, I do not anticipate the Asian segment being as severely impacted.

Luxury Spending (Market Insider)

Indeed, estimates suggest that, in contrast to Europe and America, sales in China are projected to remain largely unaffected despite the risk of an economic slowdown, as the market seems to be more resilient. Therefore, considering that sales in China constitute the majority of revenue for the Asia segment, a quick calculation reveals that more than a third of the group’s total revenue is not subject to any negative changes.

Lastly, it’s important to note that Moncler targets high-income clients, which positions the company to be more profitable and resilient even in a worst-case scenario of a fashion sector hit hard by reduced spending.

The new valuation

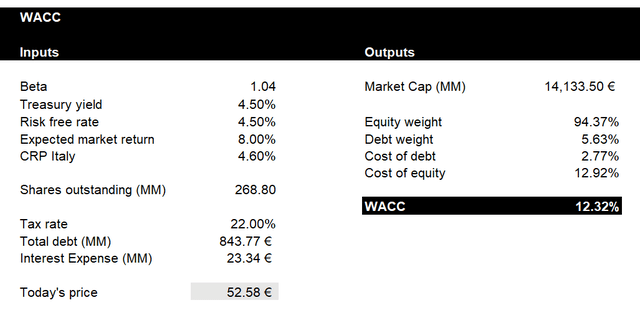

Regarding the valuation, as mentioned earlier, I have updated my DCF model. I adjusted the WACC downward to 12.32% due to the increase in interest rates.

Moncler WACC (Personal Excel Model)

Regarding other data, as explained previously, I considered a base case, which is approximately 5% lower than my previous estimates, assuming a moderate reduction in demand in the EMEA and Americas segments. I also made more modest reductions in estimates for the Asia segment, as I do not anticipate significant slowdowns in China.

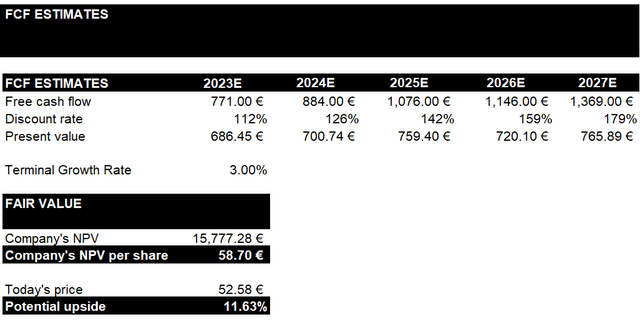

Upon reviewing my previous DCF, there has been no notable change in FCF variation. However, what affects the company’s NPV (Net Present Value) the most is primarily the interest rates and slightly lower growth over the next two years.

FCF Final Table (Personal Excel Model)

Consequently, the fair value stands at €58.70 (MONFR $63.60), indicating a potential upside of 11% from the current price.

Bottom line

In summary, analysts anticipate a slowdown in spending within the fashion sector due to economic uncertainties in Europe, America, and Asia. Nonetheless, I maintain the belief that Moncler possesses resilience, as demonstrated in 2022 and the first half of 2023. Given its status as a high-end brand, I expect that Moncler’s clientele will continue to spend despite the mentioned challenges. Furthermore, even with concerns of reduced growth in China, I anticipate the segment to weather this with relative stability, as it has consistently exceeded expectations in previous quarters.

However, it’s worth noting that the company’s price target is in very close proximity to its fair value. Over recent months, the price has reached my previous target and then retraced. Therefore, due to this negative momentum and the proximity of the price to the target, I maintain my rating at Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here