Investment Thesis

Perion Network Ltd. (NASDAQ:PERI) continues to deliver strong prospects, and yet its share price has recently taken a small breather. However, I argue that this breather is par for the course, that stocks don’t move in straight lines. This is not because Perion has had any mishaps in execution.

Rather, compared with nearly all other adtech companies I follow – and I follow many – Perion continues to positively impress me.

Accordingly, I believe that over the next twelve months, we’ll look back to Perion at $32 per share and consider it a bargain entry point.

Rapid Recap,

In my previous analysis, I said,

The most exciting aspect is its valuation, with the stock priced at 8x this year’s EBITDA. Perion’s revenue growth rates are set to impress, with the likelihood of achieving 20% CAGR by the end of Q4 2023.

I argue that analysts’ revenue expectations for Perion are considered conservative, and are likely to be upward revised soon.

I continue to believe that Perion will exit Q4 2022 with a 20% CAGR and enter 2024 against an easier comparable base, with a less onerous macro environment.

Why Perion?

Perion is an Israel-based technology company that specializes in delivering advertising solutions. Its value proposition lies in providing businesses with effective tools to enhance their digital advertising strategies and optimize customer engagement across various online channels. Perion’s solutions encompass cross-channel optimization and creative design, enabling brands to connect with their target audiences in impactful ways.

Like many of its peers, with Perion the holy grail of advertising is to provide accurate measurable results. The better quality the accuracy of the adverts, the more large customers will be willing to pay for Perion’s platform.

And this leads me to discuss Perion’s biggest customer, Microsoft Advertising (MSFT), which includes Bing Ads. Perion has a partnership with Microsoft Advertising that involves providing technology and services to enhance the performance of Bing Ads. Perion’s role in this context includes tools for optimizing ad delivery, improving targeting capabilities, and enhancing the overall effectiveness of advertising campaigns on the Bing platform.

Perion is involved in the supply side of digital advertising. It provides advertising solutions and engagement platforms that help publishers and app developers optimize their ad inventory and monetize their digital properties effectively. This places Perion in the realm of supply side platforms (SSPs) within the digital advertising ecosystem.

Imagine the digital advertising world as a big marketplace. On one side, you have the sellers, who are websites, apps, and other digital places that have space for ads. These sellers want to make money by showing ads to their visitors. Now, on the other side, you have the buyers, who are companies that want to advertise their products or services.

In the middle, there are platforms called SSPs (Supply Side Platforms). These platforms help the sellers (websites and apps) manage and sell their ad space to the buyers (advertisers). It’s like a matchmaker that connects the right ads with the right places to show them. SSPs make sure that the sellers get the most money for their ad space, and the buyers get the best spots to show their ads to the right audience. So, being in the realm of SSPs means being part of this matchmaking process in the digital advertising world.

With this framework in mind, let’s discuss Perion’s outlook.

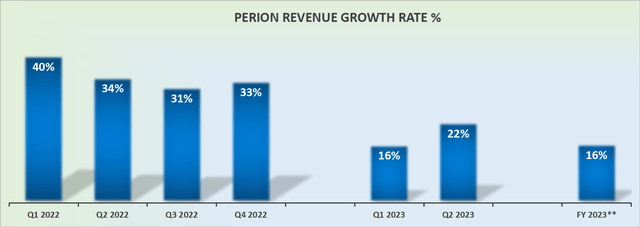

Perion’s 2024 Could See 20% CAGR

PERI revenue growth rates

In my previous analysis, I said:

Perion masterfully teases out to investors that its outlook for 2023 is likely to be upwards revised, given the strength of its H1 2023 performance.

We didn’t have concrete figures at the time, all we knew was that Perion’s 2023 outlook pointed to its revenues growing by 15% y/y in 2023.

However, Perion has since then upwards-revised its outlook so that 2023 is expected to grow by 16% y/y.

For those that have followed Perion closely, they’ll be very familiar that this company has a long history of being conservative only, to later on surprise investors.

In fact, that’s one of the main arguments bears have against Perion.

The Bear Case

Certain short reports have made the case that Perion is overvalued and proceed to make lengthy declarations to inflame the short argument. Here I highlight three:

- How [Perion] generates $1.50m and $0.30m of revenue and EBITDA per employee in the advertising technology industry, where the peer average is $0.53m and $0.07m, respectively.

- That insiders have repeatedly liquidated shares.

-

Why Perion raised $230 capital from shareholders when interest rates were close to 0%?

Admittedly, I have never understood the capital raise and discussed this aspect previously. Perhaps Perion wanted a certain M&A acquisition and it fell through? Difficult to know for certain one way or another. Nevertheless, this capital raise is clearly something odd. And shorts are not alone in that consideration.

Meanwhile, the other two noteworthy considerations can be easily explained away. Perion’s cost structure is for the most part outside the U.S. That would translate into a dramatically lower cost basis.

And as for the insider dilution since 2019, the fact of the matter is that in the past 4 years, Perion’s share price is up nearly 10x. That’s a very strong increase in a short period of time.

And talking of Perion’s performance, let’s move to the next section.

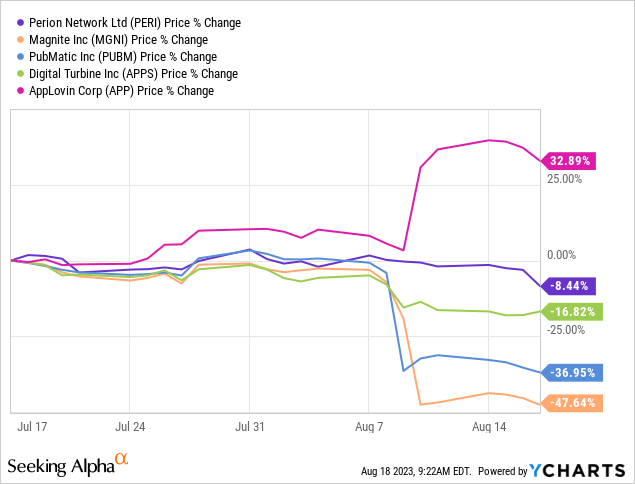

How Perion’s Performance Compares

Recently, we’ve seen Magnite (MGNI), PubMatic (PUBM), Digital Turbine (APPS), and AppLovin (APP) report their respective results. And we’ve seen countless adtech companies getting shot out of the sky.

All of these companies saw their adtech businesses shrink to varying degrees. The one that outperformed has been AppLovin. However, I have stated that AppLovin’s performance has been strong because of its Software segment. And that AppLovin’s Apps business is fairing just as badly as that of its peers, excluding Perion. Incidentally, AppLovin is a stock that I’m bullish on and recommend.

In conclusion, I believe that paying 8x this year’s EBITDA for Perion is a compelling valuation.

The Bottom Line

After closely analyzing Perion’s recent performance and market trends, I firmly believe that the recent pause in its share price is merely a natural fluctuation rather than a sign of mishaps.

In fact, compared to other adtech companies I follow, Perion continues to impress me positively.

The company’s strong valuation and anticipated revenue growth rates make it stand out in the digital advertising landscape.

With its history of conservative estimates followed by positive surprises, Perion’s potential for a 20% CAGR by 2024 seems entirely feasible.

Despite concerns raised by certain short sellers, I find that the company’s performance, cost structure, and insider actions provide a solid rebuttal to these arguments.

When compared to its industry peers, Perion Network Ltd.’s consistent growth sets it apart, making its current valuation at 8x this year’s EBITDA an appealing proposition.

Read the full article here