Dear readers/followers,

I was assigned Siemens Energy (OTCPK:SMEGF) as a spinoff back when the company was moved from Siemens (OTCPK:SIEGY), which was a core holding for me at the time. Siemens Energy, while I rode “the wave” for quite a while and made a pretty penny from the stock, ultimately turned to crap, at least for the short term, not long after I went neutral on the stock and sold my entire position.

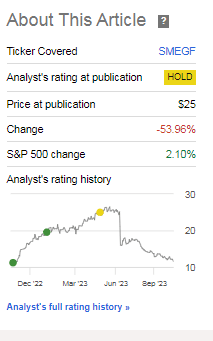

You can see my recommendations and my trajectory of articles here in this picture.

Today I am giving you a new stance for the company – or at least providing you with an article update for the business.

Seeking Alpha Siemens Energy (Seeking Alpha)

Siemens Energy is, as you can see, in a bit of a slump. This slump is, as I view it, justified here – the company has seen quality issues in its manufacturing. When I last published on this company, I had seen triple digit RoR. So I sold.

The company has always been a higher-risk investment, despite the “Siemens” brand to its operations. In this article, I’ll highlight the last set of results that we saw since August of 2023.

The company is continuing to see challenges – I don’t see a good visibility for an improvement, which means that even though things are cheap here, they’re not cheap enough.

Let’s see what we have here.

Siemens Energy – 3Q23 results were not good

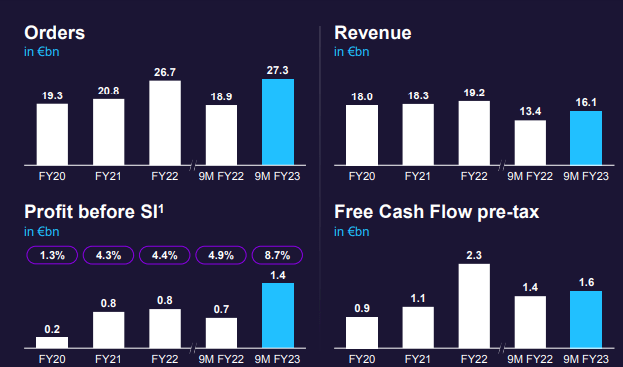

So, 3Q23 was actually a bit of a pick and mix. The company’s gas and power businesses, the former such businesses, are working well. Sales are good, and the orders are up 52.4%, now at €14.9B. The positives also include an order book that now is filled at €109B, which is close to a book to bill ratio of almost 2x.

But the order/top-line trends are only half of the story. The other half is moving down to the bottom line, which shows us a significant negative. For the 3Q23 quarter, the company is now at negative €2B for the quarter for profit, and a negative 27.3% profit margin. The company is barely FCF-positive, at €27M, which is at least up from the YoY period.

But the problem lies in what was expected to be the company’s main business – and which is now part of the problem – and not small setbacks either. Quality issues and production problem, increasing product cost, off-shore ramp up challenges – all of these things make the company’s renewables segment, Siemens Gamesa, very difficult here.

The company adjusted its guidance as of the 3Q23, now expecting a net loss for the full year, exceeding the last years negative results/losses by up to a triple-digit € amount.

The company fully expects 2023E FCF to be negative as well, up to a negative low-triple digit million € amount.

The company tries to clarify here that underlying numbers, especially top-line numbers, actually look fairly good. Cash flow performance is decent – but as you can see, all of these numbers are on a 9M basis, not the 3Q23, where numbers look quite a bit worse – also, we’re talking about Profit before SI.

Siemens Energy IR (Siemens Energy IR)

The primary impact here is for the onshore business, and let’s get into that for a bit to understand the background. Without these issues, I have a good feeling that the company would be substantially higher than we’re currently seeing.

So, the company has technical issues with both the so-called 4.x and 5.x platforms, specifically turbine vibrations during monitoring. The reasons for this has been identified as the blades and the bearings for the blades. This has resulted in disqualification of certain suppliers. The company has clarified that only a certain part of the current onshore fleet is affected, and due to the company’s multiple sourcing strategy, not all of the company’s turbines are affected either. Siemens Energy has been analyzing the faulty components – and all of this has been proactively, none of the analysis has been initiated due to turbine failures, but due to the company’s finding the faults. All of the company’s turbines are being monitored 24/7 remotely. As of this latest problem, additional inspection strategies have been implemented.

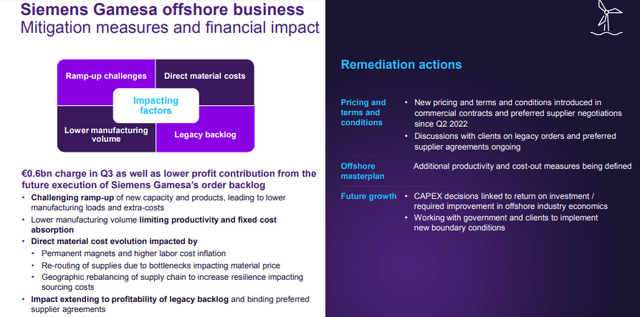

Obviously, these problems have impacted profit – and the company has recorded a €1.6B charge in 3Q, as well as an overall lower profit contribution from the backlog, given that we now need to account for increased repairs. This is before we even start discussing the costs for remediation in the supply chain, in manufacturing, increased controls in manufacturing and optimization, and higher focus on product and design.

Overall, it’s a complex situation, and it’s likely to impact the company for a long time to come. These trends have also resulted in start-up challenges in several locations, such as Hull, Cuxhaven, Le Havre and Aalborg. There’s another €0.6B in impact from these startup challenges.

Siemens Energy IR (Siemens Energy IR)

The obvious effect here from this impact is a longer path to profitability. Just how long?

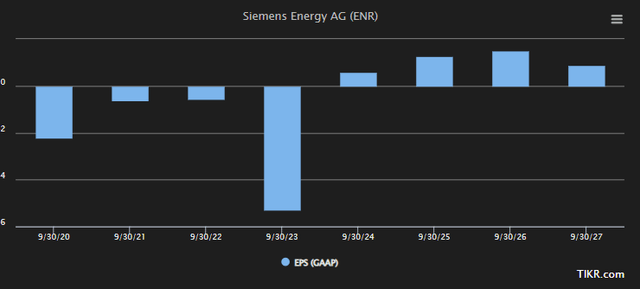

Current estimates are for 2023, and for 2024E to go into GAAP profitability, which should be growing over the next few years.

Siemens Energy GAAP EPS (TIKR:com)

Current estimates are for the company to even start paying a dividend during the next fiscal. The main hindrance to this profitability, and the reason why it’s delayed in the first place is the former Gamesa segment. But once these charges are over, it should be looking better. Far from as smooth sailing as the company wants to, in materials, make it out to be, but certainly better than we’re looking here. The company’s backlog includes massive service amounts and order levels, over €50B of the company’s backlog is actually service orders for existing units and assets, with increasing backlog levels across every part of the company’s business.

Despite what can only be described as a catastrophic year due to Gamesa, company liquidity is decent, and Energy remains at a BBB-rating, meaning it’s still considered investment-grade. if we take away the impacts, the profits for the company are actually doubled. If Gamesa worked, things would look very good.

So while I am very happy I sold my shares in the company at triple-digit profit, and why I have not gone back in yet, I believe there will come a time when Siemens Energy can be bought, and when it’s worth investing significant capital in the business.

Since the company got spun off, things have not looked good. The company has, as of this time, not managed to generate positive adjusted EPS levels. It’s at a market cap of less than €10B despite over €100B worth of back orders. The company has no yield, and any upside is based on eventual profitability, but given the historical trends, it’s difficult to estimate exactly when this will happen. More trouble might come along.

The question becomes, what do we pay for a currently-impaired company with a low forecastability that has failed to meet estimates 100% of the time currently, even if that time is less than 3 years?

The answer I would give you there, is “Not much” – but let’s look at valuation and where I would put things here.

Siemens Energy – Tricky at this valuation

I want to remind you of what I said in the beginning of my last article before the crash. I could not, as I see it, been more clear.

Combining the fact that the company is seeing to raise cash through equity, with a triple-digit RoR in a short time begs the question if the company’s current journey has come to an end and if it’s time to consider rotating profit.

I would say yes, it’s time.

I’ve been working with a long-term price target of €20/share. One of the biggest questions for this article was if I was going to change, because at a 2023-2024E EPS, the company would be valued at over 32x P/E at a €20/share given that the 2024E EPS is around €0.6/share at a current estimate.

At some point, this company is going profitable – that means that we have the opportunity to get in on the “ground floor”, but the obvious problem is we do not know how long we need to wait for this profitability to appear, or if anything else comes to disturb the trajectory.

What seems clear to me is that at some point, this order book is going to translate into positive earnings – as it has not for the last few years that the company has been listed.

An upside for Siemens energy is easily in the triple digits – provided that this upside eventually materializes and the share price can get some tailwind from actual GAAP profit.

However, here is how I see things.

The eventual negative or downside to waiting for the first positive signs of this reversal are far less, in this specific market environment, than going in too early into the stock when there are so many better opportunities and the upside is so unclear.

Siemens energy without a doubt has the potential to be a great business once it turns things around. It’s also clear that it’s in the process of currently doing so – and hasn’t lost customer confidence either. So an upside to €20/share isn’t unlikely – at some point.

However, not solely due to valuation, but due to current trends and current macro, I see the right choice here as being to wait for signs of improvement. This is a rare stance for me, but I do expect more pain in the next fiscal quarter before things eventually turn around.

Once we do get these signs, I may be one of the first here to change my thesis, but for now, the company is not attractive enough for me to “go in”.

Thesis

My thesis for Siemens Energy is as follows:

- The company is one of the more interesting plays in all of Europe on a mix of legacy Gas/power as well as a massive Renewable operation it seeks to pull from the public markets. The company is a transformation play, with a “due date” of 2023-2025 at the earliest, but now is the time to invest.

- I’m sticking to my “HOLD”, and I’m not adding shares of Siemens Energy here. My PT remains at €20/share, but I want to see what the company does in terms of recovery and other things going forward before I initiate a new position in the stock.

- For those reasons, I’m going more conservative here, and I believe investors should consider doing the same.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized)

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

It’s neither cheap, given current challenges nor with an attractive upside – I say “HOLD”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here