A Hold Rating for Stelco Holdings Inc.

Lower selling prices and higher input costs due to inflationary pressures are expected to continue to weigh negatively on Stelco Holdings Inc’s (STLC.TO) (OTCPK:STZHF) sales and profitability in the coming period.

Chasing instead of meeting a demand for steel products, as evidenced by the business dynamics, does not help either. Actually, the conditions of the demand are on track to deteriorate further as the economy slides into recession in anticipation of more rate hikes by the US Federal Reserve to stem ongoing core inflation.

The company will try to protect the solidity of the balance sheet as much as possible by acting flexibly in a challenging environment. Solid financial health is a core value that the company strives for and relies on to pay its dividend. Looking ahead, the dividend does not appear to be in jeopardy, it is also fair to say.

So, armed with patience, as they receive dividends, Stelco shareholders may also be able to increase their exposure to the stock ahead of the benefits that could potentially come from the steel industry when this recovers better conditions.

How Stelco Holdings Is Performing

By increasing shipments of value-added flat steel, Stelco Holdings sought to mitigate the anticipated damaging impact on the company’s profitability of lower selling prices and inflationary pressures on raw material sourcing.

The increase in shipping volume was notable as it rose 17% year-on-year to 695,000 net tons of steel products in the first quarter of 2023, and time has to be rolled back to the second quarter of 2022 to see a similar increase.

At that time, the company managed to ship 677,000 net tons of steel products, an increase of 14%, not year over year, but sequentially.

Commenting on the financial results for the first quarter of 2023, Alan Kestenbaum, Chairman and CEO of Stelco, said the company was managed flexibly yet thoughtfully throughout the quarter. This must have meant intensive use of stocks. However, according to Q1 2023 financial results, a significant reduction in inventories, down 24% from the end of 2022 to $599 million, did not lead to complete success. Significantly lower sales prices (down 35.7% year-on-year to $960 per net ton of steel product sold in the first quarter of 2023) and inflationary pressure on the material costs for the manufacture of the steel products sold proved to be much stronger opponents than initially assumed.

Despite higher shipments, first-quarter 2023 revenue declined 24.2% year-on-year to $687 million, which combined with a 27.5% year-on-year increase in the cost of goods sold to $644 million, resulted in a sharp decline in the adjusted EBITDA. The item was $65 million in the first quarter of 2023, down 83.8% from $402 million in the first quarter of 2022.

Essentially, Stelco Holdings Inc experienced the same challenges in the first quarter of 2023 as it did in the fourth quarter of 2022, which resulted in revenue and profitability also falling drastically.

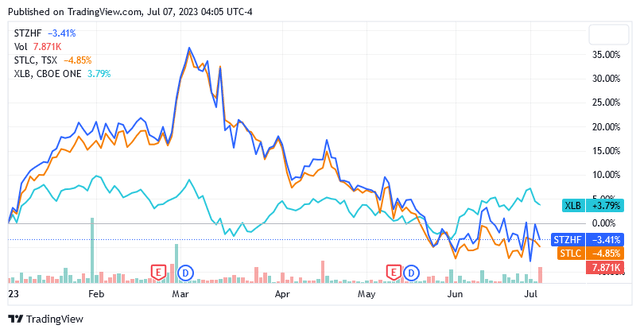

These two disappointing quarters in a row have caused the share price to fall 5.16% year-to-date, plus a sharp fall of more than 35% from the peak of March 3, actually helped by headwinds from the regional banking crisis in the U.S, this must also be noted.

Source: Seeking Alpha

Further Headwinds for the Profitability of Stelco

It should also be taken into account that in the quarter that Stelco Holdings reported its largest shipment increase prior to Q1 2023, which was the 14% sequential increase in Q2 2022 as mentioned earlier, inventories instead rose 12.5% to $568 million.

The comparison of the Q2 2022 vs. Q1 2022 trend with the Q1 2023 vs. Q1 2022 trend may indicate that demand conditions were significantly better in the quarters leading up to Q1 2023 and that their deterioration is now forcing the company to chase demand rather than meet it, with the latter strategy historically justifying higher inventories.

Then weaker demand played a very important role in lower profitability and indeed there are concerns about insufficient demand for steel products, as reported by Trading Economics.

The prospects for the demand for steel products are not promising. First, let’s say that Asia and Oceania currently top the ranking compiled by Statista.com economists as the world’s largest consumers of finished steel products.

China and India are almost certainly the countries that contribute the most to the demand for steel products from the Asia-Oceania region, as they are developing countries where industrialization and urbanization are the driving factors.

As growth slows down despite the government’s stimulus measures and the central bank’s accommodative monetary policy, the situation in China, where there are now also concerns about the environmental sustainability of steel products production, is disarming rather than providing a boost to the global demand for steel products.

But the economic prospects in the US and Europe are not ideal for the demand for steel products either. The minutes of the mid-June meeting of the US Federal Reserve Board of policymakers show a consensus that the economic situation calls for further rate hikes. This is because a still very strong labor market supports consumption and creates favorable conditions for maintaining high core inflation, far from the central bank’s medium-term objective. US private business payrolls rose by 497,000 jobs in June, the sharpest rise since February 2022, beating forecasts of 228,000. US core PCE inflation, the US Federal Reserve’s main indicator of inflation in the US economy, was 4.6% in May 2023, down slightly from April’s 4.7%, but still far away from the target of 2%.

So, the Fed is most likely to hike rates again at the July 26 meeting, with traders giving a 91.8 percent chance of a 25-basis point rate hike, and the European Central Bank and Bank of England are likely to follow suit.

Higher interest rates will raise concerns about economic growth. Statista even assumes that the chance of a recession is increasing. US retail sales, excluding gas and cars, a measure of consumption, are already showing signs of easing, which will no doubt put more downward pressure on demand for steel products.

According to the analysts of Trading Economics, falling prices can also be expected in the coming months. They forecast a downtrend of 4.2% from the current price within 12 months. As such, lower demand for steel products, lower prices, and inflationary pressures on the cost of goods sold will continue to weigh on Stelco Holdings Inc’s revenues and earnings. Therefore, this analysis does not see any opportunities for a recovery of the share price for the time being.

Additionally, Stelco’s stock prices could fall over the next few weeks as recession concerns prompt investors to heighten their risk perception of stocks, which are known to be a very risky investment product compared to bonds. Indeed, the rise in interest rates gives a greater incentive to invest in the second asset class than in publicly traded equities of companies.

The Valuation of Stelco Stock and the Implied Risk

Stelco Holdings Inc. (STLC.TO) (OTCPK:STZHF) will also be hit by headwinds from expected bearish sentiment in the US stock market and the impact on shares of the Canadian steel company will not be negligible.

As of this writing, the shares are trading at $31.48 apiece, giving it a market cap of $1.78 billion under the symbol (OTCPK:STZHF) and CA$42.38 apiece, giving it a market cap of CA$2.36 billion under the symbol (STLC.TO).

Source: Seeking Alpha

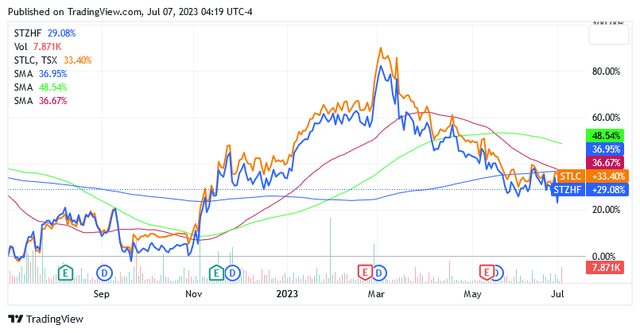

These share price levels are already well below the 100-day simple moving average line (by about 19.5% margin) and also below the 200-day and 50-day simple moving average line (by about 7-8% margin), suggesting that share price growth is lagging behind expectations.

With both stocks trading at a beta of 1.81x over 24 months (scroll down to the ‘Risk’ section of this page), the expected bearish sentiment resulting from a more aggressive stance from the Fed could be very negative for Stelco shares. On top of this, analysts at Trading Economics expect US stock futures (these securities provide a good indication of how the US stock market performs) to trend downward in the coming months. They expect the US Stock Market Index [US30], the benchmark for US stock futures, to fall from $33,850 at the time of writing to $33,475.15 by the end of Q3 2023 and then down further to the price of $30,825.77 expected around this time next year.

Thus, prices could fall over the next few weeks as recession concerns prompt investors to heighten their risk perception towards equities, which are known to be very risky as an investment compared to fixed-income securities such as bonds.

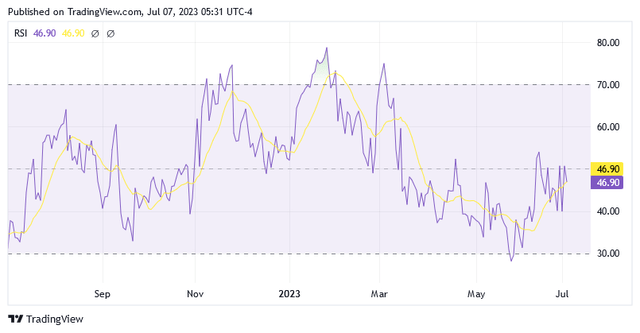

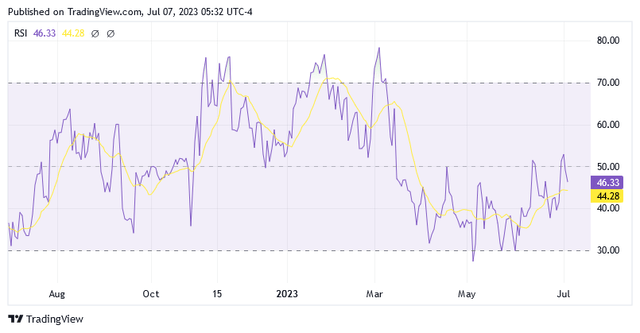

So lower stock prices are definitely possible, also according to the 14-day RSI [Relative Strength Indicators] charts below, which illustrate plenty of room for more downside effects to impact shares, so retail investors should stick to a Hold rating for now.

The chart below shows the RSI of the STZHF stock:

Source: Seeking Alpha

The chart below shows the RSI of the STLC.TO stock:

Source: Seeking Alpha

Shares of the stocks are not yet oversold despite falling sharply from the peak of March 3.

The formation of more attractive entry points could then be used to increase exposure to Stelco shares and then reap the benefits to the company’s sales and profitability when the demand for steel products recovers.

As long as the recession affects the growth prospects of the steel industry, there is a risk that the company will not live up to its core values, which could have a very negative impact on the market value of the position. These core values have been underpinned by Stelco for its shareholders by paying quarterly dividends and a special dividend.

But the presence of a solid financial position should significantly mitigate the risk and allow Stelco shareholders to patiently await the arrival of more interesting entry points to eventually increase their position.

To return free cash flow to shareholders, the company pays a quarterly dividend of $0.42 per share. The payout is up 60% over the trailing 12 months and 57.2% annually over the past three years.

The latest quarterly dividend was paid on May 23, resulting in an annualized dividend yield of 3.58% for STZHF stock and 3.92% for STLC.TO stock at the time of this writing.

The company also paid a special dividend of CA$ 3 per share on December 1, 2022.

The company is funding the dividend payment by having more than $1 billion in total liquidity available at the end of Q1 2023, of which 77% was cash and 22.8% was available on the revolving credit facility.

While the company has committed approximately $141 million in dividend payments over the past 12 months, including the special payment, this is well supported by available cash aside from operating cash flow, which was $512 million over the past 12 months, leading to $205 million after investment financing and debt payments.

The cash flow could come under some pressure in the next few quarters due to the above challenges.

As a result of the company’s indebtedness, the balance sheet incurred financing costs of $29 million in the first quarter of 2023, leading to $116 million on an annualized basis. This compares to operating income of $18 million for the first quarter of 2023, or $72 million on an annualized basis. On an annualized basis, both financial costs and operating income may better reflect recent economic challenges facing Stelco’s business, such as higher interest rates, lower steel prices and demand, and higher inflationary pressures on the cost of goods sold.

Comparing annual operating income to annual financial costs, one might conclude that there is currently a problem paying interest on the debt, but this analysis has also highlighted the amount of cash available on hand and that should help the shareholder to have some peace of mind.

In summary, an Altman Z-Score of 3.64 (scroll down to the ‘Risk’ section of this page) shows that the financial position of Stelco Holdings Inc. is quite robust and that the probability that the company will go bankrupt in the next few years is currently very low.

Conclusion

To cope with the negative impact of lower selling prices and higher costs due to inflation on sales and margins, Stelco Holdings has a tactical strategy of relying on an agile business model that will allow it to increase shipments and offset headwinds.

The near-term outlook looks not less challenging for Stelco Holdings Inc. due to the continued inflation and looming recession weighing on demand for steel products. Still, this analysis does not see a significant risk that the company could forego the core value of a solid balance sheet to support paying quarterly dividends as well as a special dividend once per year. Of course, continuing to deliver on this core value will be crucial for the stock.

Much will depend on how far the impact of the recession and inflation continues to affect the steel industry’s growth prospects. Stelco’s solid financial position should translate into acceptable risk and increase shareholder confidence pending captivating entry points to potentially increase exposure.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here