Introduction

I covered Taiwan Semiconductor (NYSE:TSM) back in October 2022 under the headline of “Taiwan Semiconductor: I’m Buying And Here Is Why”. At the time, the stock was trading at its lowest valuation since 2016 and appeared to be a sensible opportunity from both a P/S, P/E and EV/EBITDA perspective. Since then, the stock has appreciated 55.5% and provided a total return of almost 58% including dividends.

I shall be the first to say, that once a stock has appreciated by such an amount, I immediately grow skeptical concerning its prospects. I expected the stock to rebound at some point and I was lucky to identify what turned out to be the bottom, but I didn’t anticipate we could be here less than a year after. I also had the luxury of already being exposed to Texas Instruments (TXN) and Broadcom (AVGO) at the time, meaning I had the added patience of already being exposed to the sector meanwhile the stock kept dropping, to the point where it eventually traded 55% off its recent high. Then I pounced. Sometimes you’re lucky.

However, not everything is perfect as I never managed to build a full position within my portfolio, as other interesting deals were out there at the time. I advocated the principle of dollar cost averaging at that time, but never prioritized building my position fully. It’s now time for me to revisit this company, to identify if I find it prudent to extend my position.

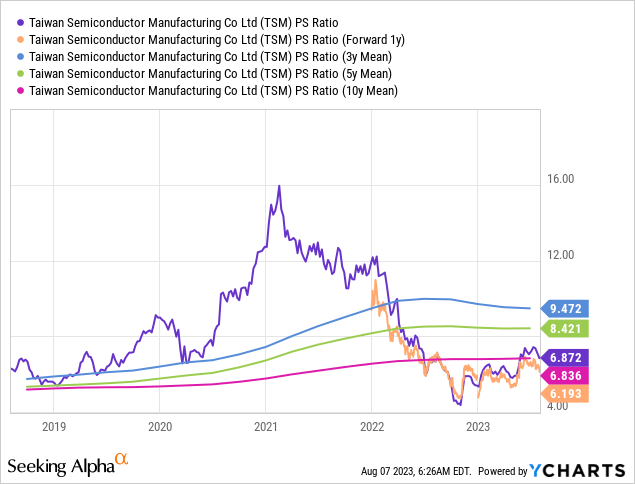

Observing the same valuation metrics as back in October, and it’s clear a lot has happened. We’re nowhere near the hay days of the Covid-19 multiple expansion (dare I say bubble?). However, we are looking at a forward 1Y P/S ratio of 6.2. That’s quite a bit. For this to be justified, I’d expect revenue growth of 10% plus in order for the company to grow into its valuation.

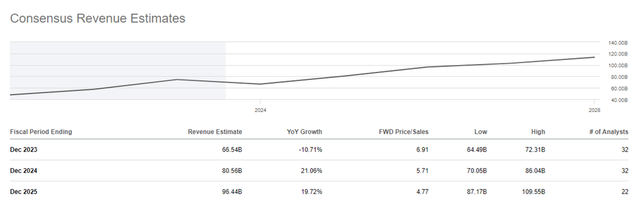

Consensus Revenue Estimates (Seeking Alpha)

If we observe the forward expectations, then it would suggest that the company can actually grow into the current valuation. I picked up the company at a forward P/S ratio of roughly 4, and if the consensus estimates hold true, the current valuation would decompress to a somewhat similar level within just a couple of years, as the expected revenue expansion would allow the company to grow into its valuation.

The expected EPS developed is more thinly covered, but consensus estimates suggest a growth trajectory slightly better than that for the revenue.

The Outlook Remains Strong

Glancing at the valuation of Taiwan Semiconductor today, my first requirement would be that the marketplace offers sufficient opportunity for the company to grow into its valuation. As I’m writing this, Taiwan Semiconductor is Asia’s largest market cap company, by a margin. You know what they say. The bigger they are, the harder they fall. In other words, there is never much room for error when you’re a juggernaut.

The situation rests on two things, first that the market keeps expanding and secondly that the company has sufficient prowess to carve its piece of that market. I covered these aspects in greater detail the first time I analyzed Taiwan Semiconductor and its outlook, but here I’ll provide a brief rundown of my perspective.

Last I covered this company, I concluded the following.

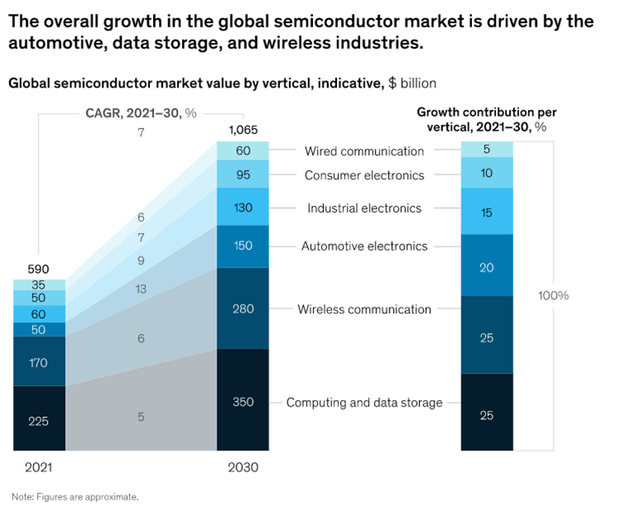

“From an industry perspective, what attracts is the fact that the industry is enjoying robust growth in both the short- and long-term. Supply and labor shortages as well as inflation is also causing pain within this industry, as with everything else, but the demand outlook remains strong seen over a multiyear horizon. According to this industry report, the sector is expected to grow 10% during 2022 in order to exceed $600 billion as a whole, while McKinsey expects the sector to have grown beyond $1 trillion by 2030. Forecasting growth on an industry level more than half a decade into the future inevitably means the estimate will be off the mark, but whether the industry value reaches a combined $950 billion or $1.1 trillion by 2030, doesn’t take away from the fact that this is an industry offering products in demand.”

Semiconductor Sector Outlook 2030 (McKinsey “The semiconductor decade: A trillion-dollar industry”) (McKinsey)

In other words, the need for semiconductors isn’t going anywhere, but that’s hardly news.

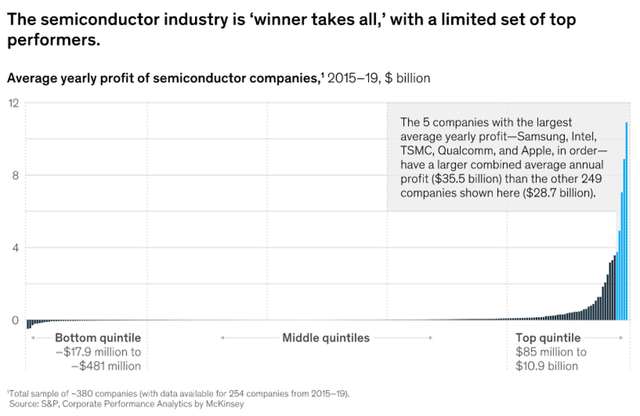

One of the most interesting aspects of this industry, is its cutthroat nature. It’s a winner takes all sort of dynamic that’s at work. The industry used to be cluttered by market participants, but Moore’s law dictating the ever-smaller nodes, has caused most of the legacy players to eventually tap out as technology pushed them beyond their abilities. Only Intel (INTC) and Taiwan Semiconductor remain of the companies who also made semiconductors if we go back just a few decades. Semiconductor manufacturing is a game of milestones. If you want to be able to produce the 5nm node, you must first be able to produce the 7nm node and similarly, if you want to be able to produce the 3nm node, you must first manage the 5nm.

Semiconductor Industry Earnings Distribution (McKinsey “It pays to be a technology leader in the semiconductor industry”) (McKinsey)

This has caused companies to lose their ability to compete, showing just how important process knowledge and technological competence is in this business. Effectively, we have three players left who push for the technological leadership. That’s Taiwan Semiconductor, Intel and Samsung Electronics (OTCPK:SSNLF) and it’s no secret that Intel has been struggling in recent years.

This dynamic has also resulted in what’s referred to as the fabless model, where companies rely upon companies with foundries (the actual manufacturer as opposed to the fabless model where the company only handles the design). This creates a concentration around those who have the foundries, such as Taiwan Semiconductor, who is servicing many of the larger fabless companies, such as Broadcom, Nvidia (NVDA) and Advanced Micro Devices (AMD).

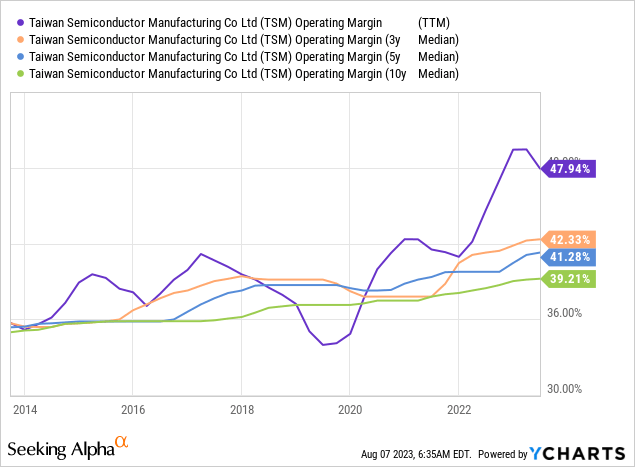

As can be imagined, this is good business for those that succeed in this marketplace. This is also evident in the operating margin for Taiwan Semiconductor and how it has developed throughout the past decade. It pays to be at the forefront of technology. The operating margin has however been inflated in the last couple of years during the concerns related to supply and demand imbalances during the Covid-19 years.

There is no evergreen scenario in any business, not even this one. Taiwan Semiconductor has had a tendency to beat on both top- and bottom-line throughout the past years, but revenue has been slowing in the wake of the Covid-19 splurge. We are in a different macro setting where companies bring down inventories and experience softening demand for their products. Take Apple (AAPL) who reported Q3 results on the 3rd of August as an example. You’ll find a lot of high-end chips within their iPhones, MacBooks and so on, but the company experienced dwindling demand. This has a direct impact on a company like Taiwan Semiconductor.

Earnings History (Seeking Alpha)

There will be volatility associated to any business and this is no different. One of the reasons why this stock traded at such a depressed valuation – relatively – back in October, was amongst other things due to the changing macro setting. The market anticipated a recession nearing, which naturally created downwards pressure on stocks in general and for cyclical companies in particular. Consumers will be holding back on getting that new phone, TV, headset, car or other consumer good that isn’t exactly a requirement once you start seeing coworkers getting laid off.

Back then, consensus estimates for revenue FY2024 stood at $90.8 billion compared to same consensus expectations today coming in at $80.4 billion, not least because of the recently downwards adjusted revenue guidance for FY2023 by management.

We still haven’t seen that recessions, but from history we know that once interest rates start getting to a certain level and improving employment start affecting wage inflation, then we are nearing a scenario where something has to give way in the global economy. If the consensus estimates for FY2024 become reality, it will represent a 21% expansion in revenue and become the highest revenue in company history.

This is merely short-term fluctuations, but those short-term fluctuations form the baseline for the future. I’d stay more focused on the long-term outlook, as I intend on holding positions for years, but it’s always important to stay aware of those fluctuations when dealing with cyclical goods and services.

A Pristine Balance Sheet Keeps This Company Out Of Harm’s Way

As the company released its Q2-2023 earnings on July 20th, it was with a significant contraction in form of YoY revenue declining 13.7%. EPS also declined from $1.55 last year, to $1.14 this year. On top of a poor YoY performance, management also communicated the need to reduce the FY2023 revenue outlook to an expected 10% YoY decline compared to a prior consensus expectation of low- to mid-single digit decline. Just to round it off, operationally, the company also had to communicate a delay associated to their new Arizona plant which is now expected to become operational by 2025 as opposed to 2024. The operational decline also showed itself when management communicated a declining operating margin on a forward basis, though it’s still expected to be in the high 30’s, which is very satisfactory in a time where it’s more difficult to run the business than normally. Not a lot of good news in that earnings communication. I’ve already mentioned that I believe the long-term outlook is much more interesting than any volatility in the short-term performance, but one thing is important.

Being a cyclical company, cash flows can come under pressure if demand halts. We’ve seen it time and time again with companies such as Nike (NKE) and Stanley Black & Decker (SWK) who couldn’t foresee a growing inventory and softening demand. Suddenly, the management team needs to liquidate that inventory both from a cash flow perspective but also before that inventory loses relevance. This isn’t immediately comparable as we are discussing vastly different goods and bargaining power setups, but the idea goes across. Remember how I mentioned that downstream customers are very dependent on Taiwan Semiconductor, which plays in the companies’ advantage.

Getting to the point here, and that point is, that any cyclical company needs a strong and cash rich balance sheet to weather potential downturns. Otherwise, those short-term fluctuations I referred to, can turn into lasting headaches for the company, where management is pushed into a corner and forced to make expensive decisions on behalf of the company and therefore compromising its ability to make value-adding decisions.

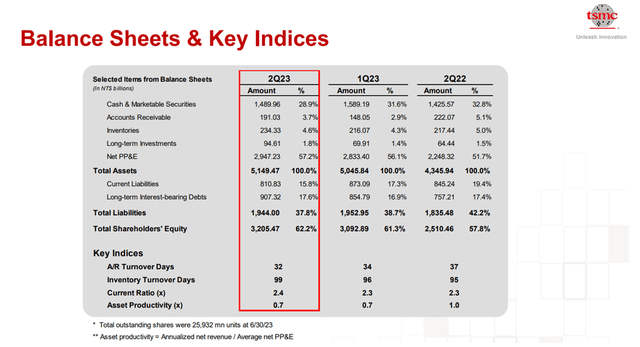

The following balance sheet numbers will be denominated in NT dollars, where the company itself assumes an exchange rate of $1 to 30.8 NT dollars.

Q2-2023 Balance Sheet Taiwan Semiconductor (Taiwan Semiconductor Investor)

The balance sheet looked marginally better a year ago, but it’s still very strong. This company has a lot of cash on hand, in fact five times the size of the inventory. In addition, the cash balance also exceeds interest bearing debt. This overview doesn’t allow my final observation, but if you head into Seeking Alpha’s financials section for the company, you’ll be able to see that there is close to no goodwill on the balance sheet. Goodwill is the bane of healthy balance sheets for companies who could come under stress. If your business is counter cyclical, then I’m not paying too much attention to goodwill, but if you are cyclical, then I certainly am paying attention. In times of distress, goodwill tends to fade into thin air. As such, goodwill becomes the illustration of a management team potentially making value destroying moves on behalf of company shareholders. A very recent example is that of Teladoc (TDOC) who acquired Livongo Health for $13.9 billion in July 2020, only to take an impairment charge of $13.7 billion in February 2022, less than two years after the acquisition, in other words, all those billions vanished. Point being, I like my investments to have strong balance sheets and Taiwan Semiconductor has got a very strong balance sheet.

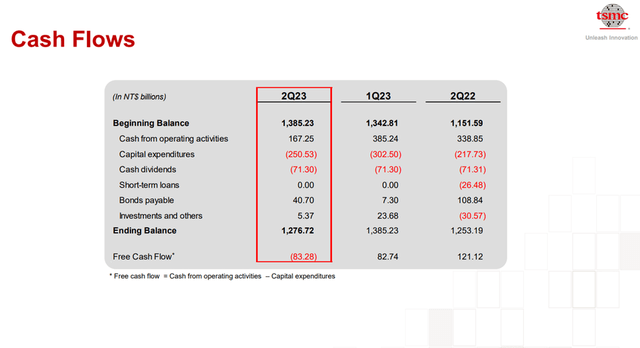

Q2-2023 Cash Flow Sheet Taiwan Semiconductor (Taiwan Semiconductor Investor)

Capex in this business is tremendous, so that cash isn’t just sitting there, it’s being rotated continuously into the running business and investments in new plants or maintenance of existing ones. However, small fluctuations YoY as seen in the cash flow statement above, doesn’t cause worry from my perspective.

This may perhaps be a situation of short-term pain at the expense of keeping the focus on long-term opportunities. At least that’s how I view it.

Risks & How To Mitigate

Taiwan Semiconductor finds itself in a situation where it must be a contortionist. It’s being pulled at from many different directions.

First, it finds itself in one of the most debated geographical areas of the world, as its native to Taiwan. Last time I wrote the following about that particular risk and my perspective on it.

“The company is located in Taiwan, one of the hot regions of the world, not only today but for the foreseeable future. Reason being, that China has a goal of unifying Taiwan with China. That can be done peacefully or aggressively, and this is a matter of hoping for the best but preparing for the worst. Before Xi Jinping’s rise to power, China had Hu Jintao as leader of the communist party, and at one time, he advocated for the use of soft power. What has been translated into ‘China’s peaceful rise’. This was official policy and a slogan in China back then, in order to assure the international community and regional neighbors of China’s intentions. The underlying reason was constructed around the idea of soft power, that strong and close relations do more for China, than the use of real power.

The ‘peaceful rise’ principle was constructed at a time where China wasn’t the same superpower it is today, and there was a different leader of the Chinese communist party. Furthermore, the principle was communicated prior to the later, and now official policy concerning Taiwan, labelled the Anti-Secession law, voted into effect back in 2005. This states, that China is authorized to use force if peaceful means are not able to unify the two, or if a situation should arise where Taiwan declares its independence. International response at the time was as could be expected, with the western countries in opposition.

So far, China has in fact managed to climb the ladder of economic development without having resorted to warfare, but the question is of course if the same shall be the outcome for this particular question.”

On the opposite side of that spectrum, we have the fact that semiconductor manufacturing has become national security policy in the US. We’ve seen export restrictions slapped onto ASML (ASML), who can’t sell their full array of offerings to Chinese companies as well as having restrictions on what type of equipment they may offer maintenance for. It’s complicated, and it puts companies operating in this space in an awkward position.

Taiwan Semiconductor is striving to finalize their new plan in Arizona, which has been delayed due to lack of skilled labor both in terms of finishing the plant and also ensuring its operations. That’s not how it was planned to play out, and it complicates the landscape as Taiwan Semiconductor and its peers must be scratching their heads as to the feasibility of betting on this region of the world. We’ll see more of these incentivization structures going forward, as semiconductors play a vital role not least in defense and space related equipment. Areas where the US (and others) will not allow themselves to not have access to the components needed to defend itself.

Companies in general have for a long while draped themselves in the flag in countries where it’s expected of them, such as China. However, that behavior is starting to move west, where companies are expected to be loyal and pick a side. Last year, when Intel (INTC) broke ground on its two new manufacturing sites in the US, Pat Gelsinger, CEO, said he could feel the national pride well up inside of him. Other companies strive to stay under the radar, but both strategies can result in political fallback. These are global companies who conduct operations throughout the world, perhaps Intel more so than Taiwan Semiconductor at this point, but their Arizona plant will mark a turning point. It’s difficult to stand behind patriotic cheerleading if you are at the same time operating with a global footprint either through your operations or the very least as a result of where your sales end up.

Then we end back up at the contortionist reference because companies in this particular space are being pulled at from multiple directions, and it’s immensely complex for them to navigate. Especially for companies who run CAPEX budgets in excess of $30 billion a year, such as Taiwan Semiconductor. Where do you place investments and how do you prioritise? That’s a risk, and it’s much broader than the lingering conflict between China and Taiwan or Beijing and Washington. There’s a real chance of political fallback here, as we’ve also seen CEOs being pulled in front of congress even to answer a barrage of questions, perhaps not always fair as political agendas have to be served as well. I would consider the whole situation inflamed, and perhaps we don’t fully understand the governance implications for these companies today. We just don’t know today if there is something hidden here.

Point being, that this company as well as its peers operate in difficult waters where the potential for conflicts is very real, perhaps more so than for many other companies.

You Need To Take Precautions

I’m of the opinion that Taiwan Semiconductor is a great company, but investors need to take precautions here. In my portfolio I don’t have other holdings with such a controversial risk exposure. Businesses can’t hide from geopolitics, but as investors we can limit our exposure to decrease the impact of downside, should it come knocking on our door. The answer? Diversification or a capped exposure to this individual company as part of one’s entire portfolio. At least that’s the principles I follow.

Valuation

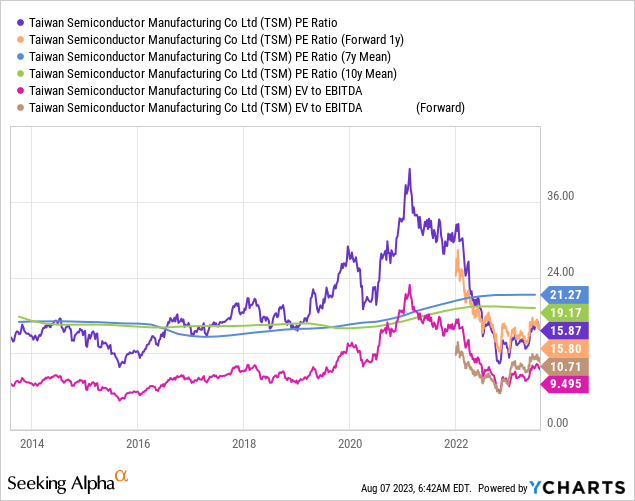

The company isn’t the same slam dunk purchase it was back in October, but if we look at the current valuation from a P/E or EV to EBITDA perspective compared to its historical norm, the stock still appears to be a fair buy. However, given the risk exposure for this company, I’d also stay firm on the need for a margin of safety.

Right now, semiconductors are the hot topic of this decade, but there’s also a scenario where these companies will receive a haircut associated to their risk profile. Same as with tobacco- or oil companies who are never allowed to trade at premiums which has been the norm rather than the exception for semiconductor companies. I’m not saying this is realistic right now, but as investors we must respect that what’s currently hot, might not be so in a couple of years. As such, this is not a company I’d be willing to pick up if I had to pay a premium.

It’s peer ETF, the iShares Semiconductor ETF (SOXX) is up 48% YTD compared to Taiwan Semiconductor which is up 30.3% from a total return perspective, so the company is trailing a bit.

I view the current valuation as a fair opportunity to invest in this company, not least because the company can weather implications from a potential recession due to its strong balance sheet.

Wrapping Up

Taiwan Semiconductor is in a unique position within its industry as an established leader, but it also carries a unique risk profile. On a relative basis, the valuation is still acceptable for a company expected to maintain double digit growth, keeping in mind it’s cyclical as also showcased in the FY expectations for 2023, where both top- and bottom-line is compressing.

Back in October, the stock traded at its lowest valuation since 2016, but the market also forecasted a recession at the time. That narrative has changed to some extent since then. Personally, I still believe we’ll have to go through a recession as central banks never succeed with what’s called a soft landing. With interest rates at their highest since the global financial crisis, history will tell us that it ends in an uncontrolled contraction, which would weigh heavily on a cyclical company such as Taiwan Semiconductor.

I also do conclude that the current valuation is fair with respect to the potential downsides both from an unforeseen macro scenario as well as the troubled waters within which it operates, creating a unique risk profile.

I think this company is worth being exposed to, as long as one takes the needed precautions to protect their portfolio. I’m perhaps not as bullish as many others due to the special risks, but I’m still of the opinion that this is a very strong company, operating in an industry with a very interesting outlook.

Read the full article here