A couple of days ago, Teekay Tankers (NYSE:TNK), one of the leading oil tanker companies, released its Q3-2023 earnings. Results were in line with analysts’ expectations, and the stock only marginally increased its value. In this article, I will provide an overview of Teekay Tankers’ Q3-2023 results, and I will explain why I believe the company is still worth a buy recommendation. Indeed, Teekay Tankers is a financially sound company and, by being a leader in the oil tanker market, will benefit from the prolonged high tanker rates that are supporting a strong FCF generation and profitability. The forces that are putting pressure on tanker rates are not going to fade in the near term, and this is good news for Teekay Tankers.

If you are interested in energy stocks, I have recently covered Range Resources.

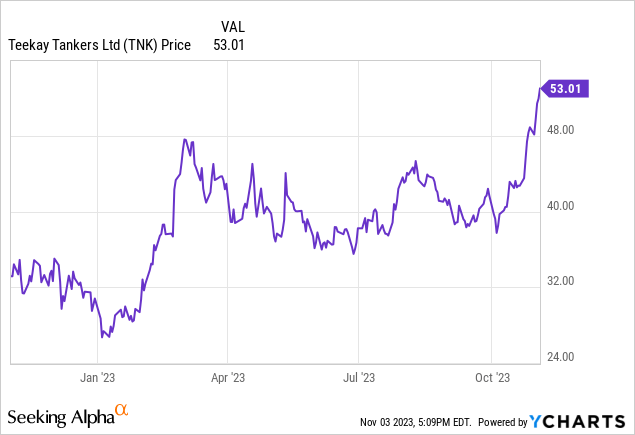

Stock performance

Teekay Tankers is currently trading at $53/share, equivalent to a market capitalization of $1.8 bn. The stock is up 60% year-on-year, while the performance is even more impressive on a yearly basis, with Teekay Tankers increasing by 72%. When I wrote my last article about Teekay Tankers, the stock was trading at $43.8/share and has gained 21% ever since. The 52-week minimum is $26.7/share, recorded in January 2023, while the 52-week maximum has just been reached at $53/share.

Q3-2023 Results

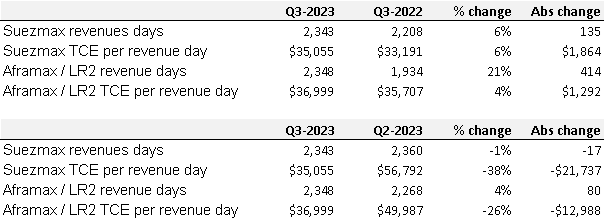

Revenues for Q3-2023 were $285 M, slightly up 2% year-over-year, from $279 M. Revenues were quite in line mostly because tanker day rates did not fluctuate too much if compared to Q3-2022: Suezmax day rates increased by 6% from $33.1k/day to $35.0k/day while Aframax/LR2 rates increased by 4% from $35.7k/day to $37.0k/day.

On the other hand, it is possible to notice that revenues significantly dropped quarter-over-quarter (-23%, from $370 M to $285 M) due to declining rates as can be seen in the table below. However, the Q3-2023 rates, despite being lower than the previous quarter, are still at extremely high levels and are more than enough to ensure profitability. Indeed, Teekay Tankers’ breakeven average rate is about $16k/day – almost half of the current market rates – and at the breakeven level, an FCF of about $2.6/share is generated.

Teekay Tankers

OpEx pre-write down decreased by 4% to $204 M with voyage expenses (bunker fuel cost and port tariffs) being the most relevant item at $113 M, down 16% year-over-year. Other relevant cost items were vessel operating expenses ($36.3 M, up 1% y-o-y) and depreciation ($24.5 M, up 1% y-o-y). It is worth mentioning that there was a $12 M increase in time-charter expenses (from $7.2 M in Q3-2022 to $19.3 M in Q3-2023) due to more vessels being chartered.

EBIT increased 8% to $81.5 M thanks to increasing revenues and decreasing OpEx. Net income increased more than proportionally vs EBIT, from $68 M to $81 M (+20%) due to some tax recovery.

Moving to the cash flow, cash flow from operations for the first nine months of the year was $493 M, driven by the high net income ($402 M in the nine months). Cash flow from financing was negative at -$451 M, mostly due to the prepayment of some obligations related to financial leases ($364 M) and to dividends paid ($50 M). Cash flow from investing activities was only -$2 M with no relevant movement to highlight.

Liquidity and debt

At the end of September, Teekay Tankers had $227 M of cash and a total financial debt of $145 M, resulting in a net cash position of $83 M. This represents a significant improvement versus the prior quarter when the company had a net debt of $28 M.

In addition to the $227 M in available cash, the company also has a credit line with an undrawn capacity of $284 M, bringing the total liquidity to $511 M. In terms of debt repayment, I do not see any relevant problem since Teekay Tankers will only have to repay $21 M per year from 2024 to 2027, an amount that can easily be covered by the FCF generation

Tanker market overview

Despite tanker rates having recently been declining, the values seen in Q3-2023 are still high if compared to the period pre-Covid and pre-Russian-Ukrainian conflict. I believe that rates will continue to remain at high levels, with Teekay Tankers so far having booked 42% of the Suezmax fleet at $26.5k/day and 37% of the Aframax/LR2 at $38.8k/day (higher than Q3-2023). It is also worth mentioning that, at the end of October, the spot rates jumped again at incredibly high levels (Suezmax at $73k/day and Aframax at $84k/day) mostly due to the general concern about the extension of the Israeli-Palestinian conflict. Considering that less than half of Teekay Tankers’s fleet has so far been booked, I expect that the average Q4-2023 Teekay rates will be significantly high, leading to strong FCFs.

As I mentioned at the beginning, the high rates are supported by some demand/supply dynamics that are likely to persist throughout 2024.

Indeed, according to IEA, oil demand is expected to increase by 0.9 million barrels per day in 2024 with demand from non-OECD Asia Pacific countries increasing by 1.3 Mbbl/day and demand from OECD countries decreasing by 0.4 Mbbl/day. IEA also forecasts that the majority of the oil supply increase in 2024 should come from countries such as the US, Canada, Guyana and Brazil. Therefore, I believe that these dynamics could benefit oil tanker companies since there could potentially be an increase in Atlantic-to-Pacific oil voyages, leading to fewer idle days and higher rates.

In addition, the Russian-Ukrainian conflict is still creating disruption in the European oil market with EU countries that are no more buying oil from Russia but from more distant countries.

On top of the oil demand phenomena, I believe that another fact that needs to be highlighted is the scarcity of available oil tankers with new order books that are at historical minimum levels. Low levels of new orders, together with an increasing average general fleet age, will ensure a low growth in tanker fleets worldwide, at least for the next 2 years.

Risks

One of the main risks to which Teekay Tankers are exposed is represented by the possibility of vessel hijacking or a marine disaster with a subsequent environmental issue. This risk is mitigated with the use of proper insurance policies that cover war risks – such as piracy and terrorism – and environmental risks. In particular, the maximum amount of coverage for pollution damages is $1 bn per incident per vessel.

Another risk I see is represented by an aging fleet: the current average age of Teekay Tankers’ vessels is 14 years and sooner or later, the company will have to replace the older vessels. However, as mentioned in the previous section, shipyards are full and placing an order for a new build either means waiting or paying a premium.

Conclusion

In conclusion, I believe that Teekay Tankers is a good opportunity for long-term-oriented investors. Despite the stock trading at its 52-week maximum, I believe that there is still room for growth since the oil tanker market dislocation will not go away for at least all of 2024. In addition, the company is financially robust with a net cash position and is led by top management, which is steering the company in the right direction.

Read the full article here